")

Dear readers/followers,

I cover many Italian companies – and while Tenaris (NYSE:TS) (OTCPK:TNRSF) headquarters are in Luxembourg City, but is a majority-owned subsidiary business of the Techint Group, which is a major company initially from Italy, but currently headquartered in Argentina with interest in everything from steel to energy, to engineering, to construction and industrial equipment.

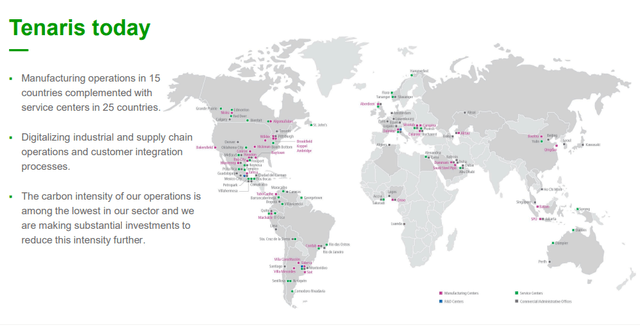

Tenaris S.A. is a Luxembourg-headquartered supplier of welded steel pipes for gas pipelines. Its manufacturing facilities are found across multiple continents and the company has representation across 30 countries. Tenaris has the capacity to manufacture over 5M tons per year of seamless and welded pipes.

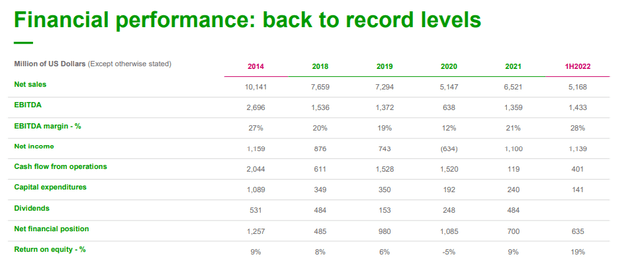

The company is one of the leading players in this, and related services for the energy industry but also other industrial applications. The company has now been on the NYSE for 20 years as of 2022, and in those 20 years, the company has become a leading supplier of energy and reached record sales and financial results for the 2022 fiscal.

In this article, I’m going to present Tenaris to you – and why you may invest in the business at a good valuation, and what sort of upside you can expect if you do invest.

Tenaris – A driver of energy

So, first off – to give you a picture of the scale of Tenaris, here is Tenaris as the company’s operations are today.

Tenaris IR (Tenaris IR)

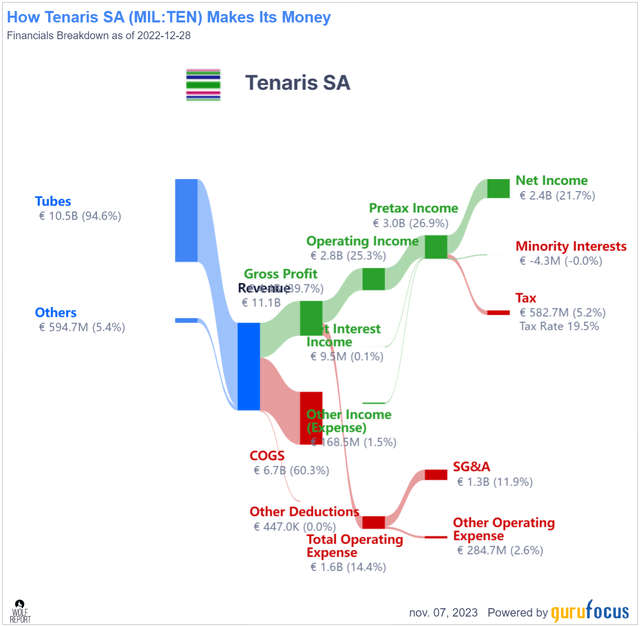

We begin, as we always do, with hard data. The company estimates 2023E revenue of just north of €13.6B. On that sales revenue, the company expects an EBIT margin of 30%, and a net margin of almost 24% if we look at 2022A numbers, the latest set of annual results we have for the business. That set of margins means, when adding the company’s 42%+ Gross margins, that the company has above-average margins to the sector, in this case, margins in the oil/gas industry.

When looking at the business model, you’ll see that for 2022, the company had truly excellent results and trends. We’re talking about nearly 60% COGS, despite it being a manufacturer and less than 15% OpEx with less than 12% SG&A.

Tenaris business model (GuruFocus)

The company also has very solid fundamentals in terms of leverage. We have a cash-to-debt of 4.53x and a debt/EBITDA of 0.14x with an interest coverage of 42.2x. This is a well-run company in terms of its balance sheet, and this moves to return metrics like RoE, ROA, and ROIC, all significantly above average.

You can’t view Tenaris how it was 10 years ago compared to Tenaris how it is today. The company has significantly evolved its demand and sales mix over the past 20 years. Currently, close to half of the company’s sales go to the US and the Canadian market, and over 60% of the worldwide OCTG sales are made through the company’s Rig Direct Service. Tenaris is now developing products for low-carbon energy applications, and is working to become a leading player in things like geothermal energy, CCS, and hydrogen.

The oil market recovered from its lows last year, moving to pre-pandemic levels with more drilling and higher consumption of OCTG per rig, which has a strong correlation to the company’s revenues and profit – given its position as a leading domestic OCTG producer (Source: Tenaris).

The US and Canada are not the only areas where Tenaris is growing. The Middle East segment is experiencing growth and evolution here, with Tenaris seeing increases in Qatar, while Saudi Arabia, UAE, and Kuwait are all set to increase oil and gas production. Tenaris has already established long-term agreements with these players, is supported by local industrial development, and has advantages through its technologies and services, like Rig Direct, Dopeless, and others.

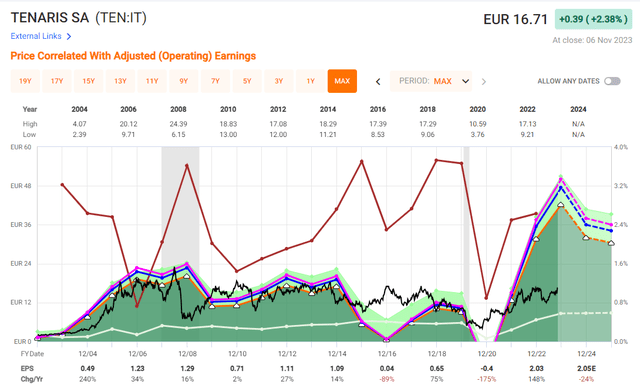

Tenaris is a very cyclical company, following the crude/energy cycle. The last upswing we had was in 2014 – with 2022 being the “next” sort of upcycle. What you see here is how low the company usually goes, and how far up it goes – with the associated return metrics.

Tenaris IR (Tenaris IR)

The company is without a doubt a leading player that’s consolidating an already-excellent market position. It’s also doing more to support the ongoing global transition in energy, and like any company, is actively investing in its production and supply chain efficiencies. Looking at the most recent results, which are the company’s 3Q23, we see a lower net income, lower operating income, and sales – as trends are slowly normalizing from the 2022A high. Due to a difficult comp, we’re seeing a significant decline – 21% on sales, and 52% on net income, as well as on the ADS EPS.

These 3Q23 trends reflect declining activity and price declines, which honestly you should have been able to expect early this year given the inflationary trends and overall macro. Tenaris has still managed over $3B in cumulative FCF this year and still has over $3B in cash. So while the trends are certainly down YoY, the company is in no way in a troubled situation.

This article is poorly timed – I’ll admit that. Tenaris was at a very attractive valuation not that long ago. In September, the business traded below €13/share – but even at the current valuation of just north of €16.7, the company is still decently attractive. The company has a current yield of 3%, which is well below the current risk-free rate, but still offers us an upside.

The company recently approved a share buyback program, currently representing over 75.4M shares, or almost 6.5% of the current SO, to be done within a year. Given the company’s new profit potential on a forward, forecasted basis, I don’t believe this to be a bad choice, but I would have preferred extraordinary dividends to shareholders instead – but that is not what Tenaris does with excess cash.

Overall, the Energy industry will continue to be volatile. In the past few months, we’ve seen oil prices remain above $80/barrel, and this is despite ongoing concerns about interest rates on the global economy. NG prices are rising along with LNG and European Natgas prices, showing high volatility despite positive demand and potential supply interruptions (Source: Tenaris).

The company has also been investing in new ventures. In October of 2023, the company put into operation its new wind farm, at 103.2 MW of power implying a reduction of Co2 of 152,000 tonnes each year. The company has also put an investment into a new wind farm in Argentina at just over $210M, which together would mean that 80% of the company’s Campana energy demand would be filled by wind power, significantly reducing Co2.

So while the company’s results are going down – both Seamless and Welded tube sales are down, and it’s down across every single geography (least in Asia, Middle East, most in NA), Tenaris is continuing to invest its cash into ventures that either improve its profile or improves its appeal (buybacks).

I have not yet invested in Tenaris – but I believe the company has an appealing enough upside for you to “BUY”.

Let me show you what the valuation implies and what the upside for Tenaris could be.

Tenaris – An upside worth considering, even if we see a 2024-2025E decline.

In order to effectively invest in Tenaris, you need to accept the through-cyclical trends of this business and the associated sector. You can see that earnings go up and down, as does the company’s share price. You can see where you need to “BUY”, and where you’d need to “Trim” if you wanted to be efficient, at least generally. The company typically doesn’t rise far above 15x normalized, not unless you look at special situations, like the period between 2015 and 2018.

Tenaris 20-year share price (F.A.S.T graphs)

You can also clearly see the impact of the materially improved earnings trends over the past few years – and how this is currently expected to go. This year is expected to be an adjusted EPS apex, after which it will decline.

This is why, despite the company being a solid business, I do not consider the company at a very high price target. Because you’re investing in a cyclical business with a less than risk-free rate yield in a declining market. I’m not sure about the amount of decline, but I would say that the decline is actually likely here, given current macro and market trends.

The 5-year average here is just below 14.3x P/E. This sort of multiple upside would imply almost 30% annualized here, based on this much higher level of earnings we’ve seen for the past years, and a 2025E of €1.95/share for the native listing of TEN, currently trading at €16.7.

However, I don’t consider this a likely outcome given the EPS trajectory of negative 12.6% per year until 2025E, on average. This implies a share price of almost €28/share, which I consider completely unlikely.

And this is a conservative P/E estimate. The company, over a 20-year average, trades closer to 17.5x P/E, which would imply almost €35/share.

I consider Tenaris likely trading range between €11-€21, going by projected FCF and historical averages. Current S&P Global analyst averages for the company are around €20/share, from 11 analysts going between €14 to a high of €24. Only 4 analysts out of 11 are at a “BUY” though, with most of them either being at “HOLD” or “Underperform”. A year ago, Tenaris was not only cheaper, but the average was at €16.25.

Most conservative valuation metrics and methods point to Tenaris being worth at least €17-€19/share or above. A Peter Lynch valuation points it to €60/share, and an average in the sector of the tangible BV points to around €11/share. The averages, if we look at projected free cash flow, sales, Graham analysis, and other methods really point to above €20/share being possible (Source: GuruFocus). This makes a €17-€18 implication a conservative valuation, and one I believe represents an excellent entry point.

I may “BUY” Tenaris in the near term – but there are many great companies currently on sale, where valuation implies significant underperformance without exposure to cyclical sectors like this one. Every investment needs to not only be justified by its own merits and to its own valuations, but to other available investments as well.

While Tenaris does this, it does so barely – and it’s an easy argument to make, that other investments are of equal value and upside, or better, at a lower risk.

So, for the current situation, I’ll go “BUY” here, but with the addition that you should be careful investing here.

Thesis

- Tenaris is a leading company in the attractive segment of energy services. The company has a leading position in several markets, and has one of the better balance sheets in the segment and industry, with extremely low leverage and high overall interest coverage.

- Tenaris may not have the highest yield, or even a high yield for this sort of company, but it has a history of outperforming the market over time. Investors who bought 20 years ago, have done very well for themselves with over 12% annualized return inclusive of dividends – this is despite the downcycle lows we saw in 2016.

- I consider the company to be a “BUY” below a share price of €17/share, making it attractive here, if barely.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

The company is a “BUY” here, but barely. It fails on the “cheap” portion of my criteria, and there are so many good alternatives today – but I would not call it wrong to buy Tenaris here.

Thank you for reading.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here