This article was coproduced with Cappuccino Finance.

The net lease REIT sector is getting a lot of attention these days.

However, back when I began writing on Seeking Alpha (in 2010), the property sector was mysterious to many.

Most institutional investors were not interested. There were just a handful of analysts interested in covering REITs like Realty Income (O) and NNN REIT (NNN).

Over the years the sector grew, largely because of the increasing number of investors who were seeking steady “sleep well at night” income.

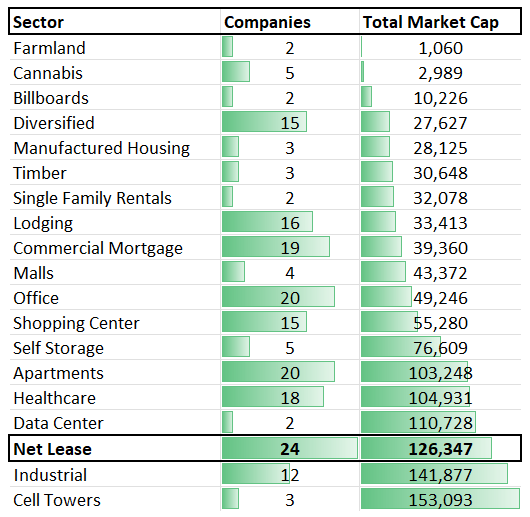

As shown below, the net lease REIT sector is now the third-largest category with a total of 24 companies with a combined market capitalization of more than $126 billion:

iREIT®

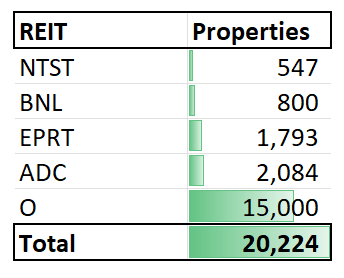

Today we would like to provide you with a list of five of our favorite net lease REITs that collect more than 20,000 monthly rent checks from tenants.

iREIT®

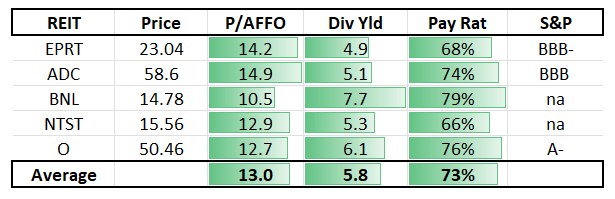

Essential Properties Realty Trust (EPRT)

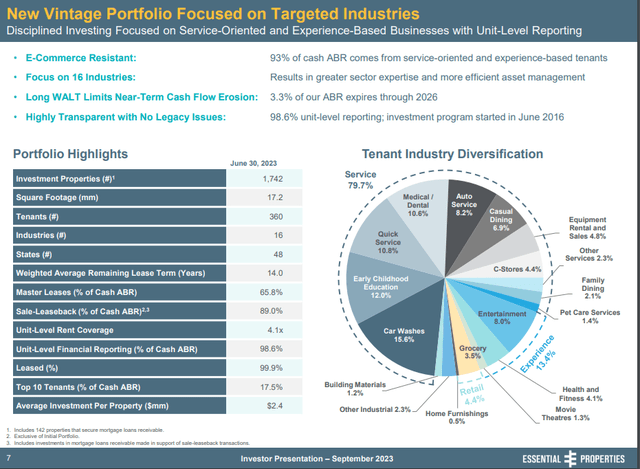

Essential Properties Realty Trust has a portfolio focusing on 16 different industries that are e-commerce resistant with limited near-term cash flow erosion.

They have more than 1,790 properties and 99.9% of the properties are leased.

Also, they enforce unit-level financial reporting with disciplined underwriting, and the current unit-level rent coverage is at 4.1x.

Investor Relations

Essential Properties also has a very conservative and flexible debt structure. They have a well-laddered debt maturity schedule with a weighted average debt maturity of 5.2 years. The cost of debt is fairly low, and the weighted average interest rate is 3.4%.

Essential Properties reported strong results during a recent earnings call.

Their same-store rent growth was favorable at 1.2%, and they acquired 65 properties (30 separate transactions).

3Q investment reflected an improving pricing environment with a cash cap rate of 7.6%, an average annual rent escalation of 2%, and a weighted average lease term of 17.6 years.

Management expects the favorable cap rate environment to persist in the near term.

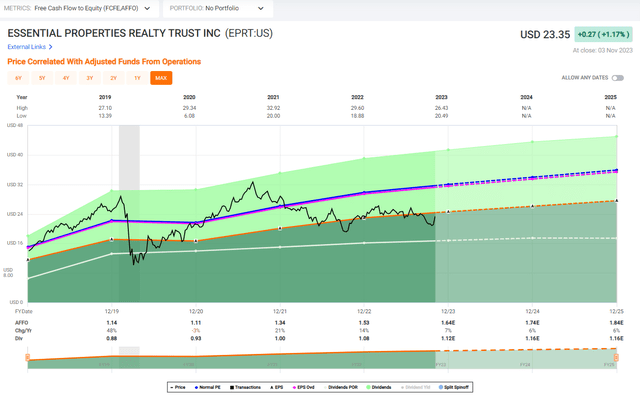

The current valuation of Essential Properties suggests that they’re undervalued.

The current P/AFFO of 14.24x and P/FFO of 13.50x are about 30% less than their historical average.

Our tracker shows the margin of safety at 15% with a “Buy” rating.

FAST Graphs

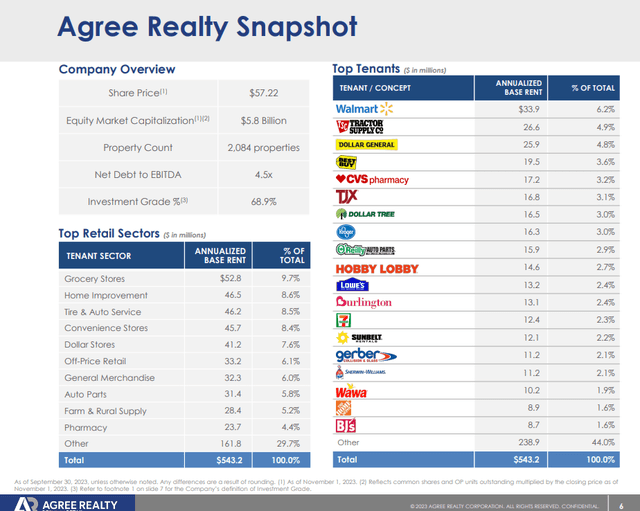

Agree Realty (ADC)

Agree Realty has the country’s leading retail portfolio. They have more than 2,000 properties in their portfolio, and their top tenants include Walmart, Tractor Supply Company, Dollar General, and Best Buy.

Their portfolio will be even stronger in the future as they incorporate their newly acquired 74 high-quality retail net lease assets (worth $398 M) in Q3 2023.

Agree Realty focuses on four core principles: Omni-channel critical (E-commerce Resistance), recession resistance, avoidance of private equity sponsorship, and strong real estate fundamentals.

Investor Relations

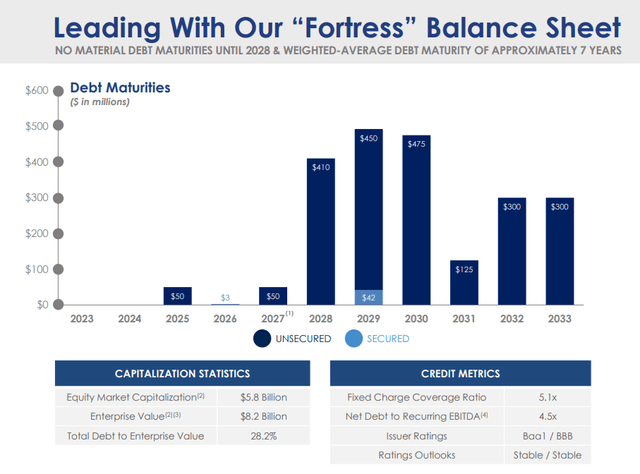

Agree Realty has a strong balance sheet that gives peace of mind to investors. The debt maturity schedule is very well spread out over the next couple of decades, and the net debt to recurring EBITDA ratio is at 4.5x.

The fixed charge coverage ratio stands at 5.1x. It’s not surprising to see the credit ratings of Baa1 (Moody’s) and BBB (S&P) with stable outlooks for Agree Realty.

Investor Relations

Agree Realty had a strong 3Q 2023 performance with a 4.2% YoY increase in AFFO per share and a 3.8% YoY increase in dividends. During 3Q 2023, Agree Realty invested approximately $411 M in 98 high-quality retail net lease properties.

The properties acquired during the quarters are leased to the leading operators in the sectors. I expect this strong performance and increasing dividend trend to continue in the future.

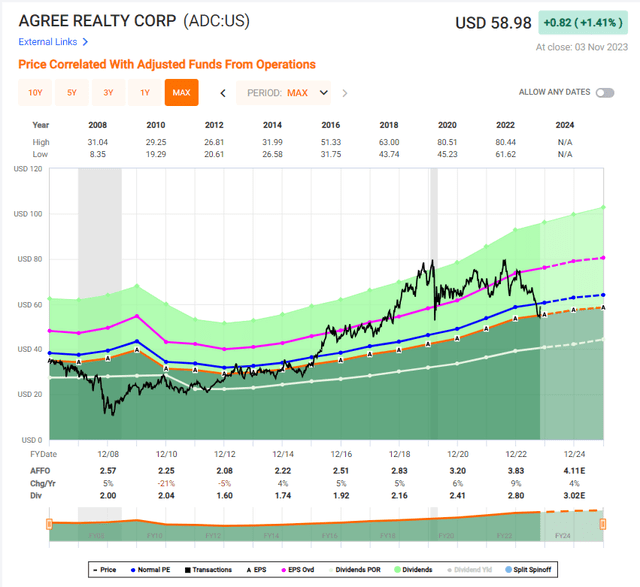

Looking at the valuation, Agree Realty is undervalued at this point.

The current P/AFFO of 14.93x and P/FFO of 14.93x are about 27% lower than their historical average. Our equity rating tracker shows the margin of safety of 20% for Agree Realty with a “Buy” rating.

FAST Graphs

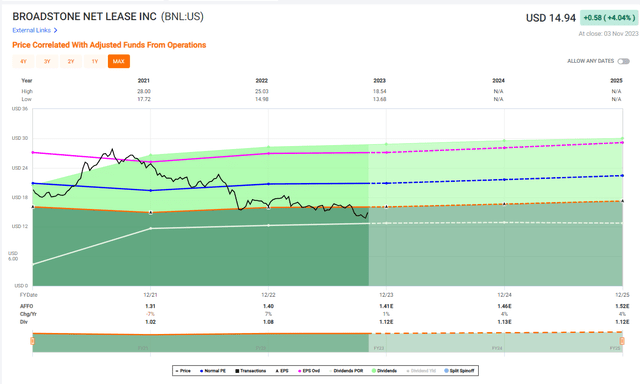

Broadstone Net Lease (BNL)

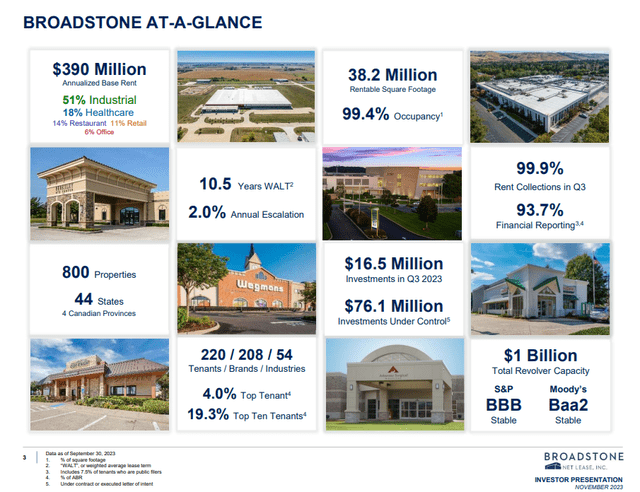

Broadstone Net Lease is a REIT that focuses on industrial real estate. They acquire, own, and manage primarily single-tenant commercial properties that are net leased.

The portfolio consists of 800 properties in 40 different states and four Canadian provinces, and their weighted average lease term is 10.5 years. The tenant base of Broadstone is very well diversified with more than 200 tenants in 54 different industries.

Investor Relations

Broadstone has a strong balance sheet with plenty of liquidity. The debt maturity is well spread out over the next several years, and there’s no significant maturity until 2026.

The net debt to annualized adjusted EBITDA ratio is 4.9x, and the fixed charge coverage ratio is 4.3x. Broadstone has a $1 billion revolver capacity. The credit agencies rated Broadstone as an investment grade (BBB from S&P and Baa2 from Moody’s).

During the recent quarter, Broadstone successfully disposed of select assets that possessed a credit risk or residual risk (two properties for gross proceeds of $62.3 M). Year-to-date, they have sold 11 properties for gross proceeds of $189.1 M at a weighted average cash cap rate of 6%.

Utilizing these proceeds, the management team will continue to evaluate potential new acquisitions (more than $10 billion of pipeline opportunities) and execute the acquisition to increase the profitability of the portfolio.

Looking at valuation, Broadstone is clearly undervalued at this point. Our tracker shows a 37% margin of safety with a “Spec Buy” rating. The current P/AFFO of 10.6x and P/FFO of 10.3x are about 30% lower than their historical average.

The dividend yield is a juicy 7.63%.

Given their strong balance sheet and solid growth prospects, investors should grab some shares of Broadstone and collect dividends while waiting for the stock price to rise.

FAST Graphs

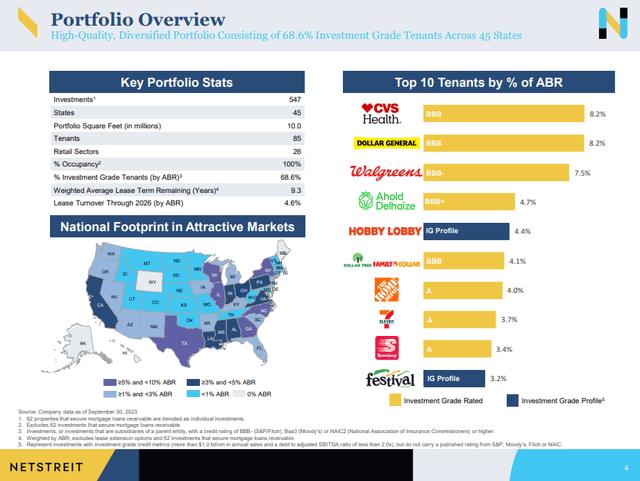

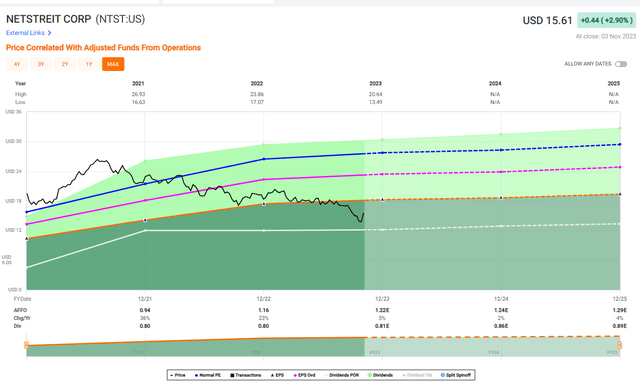

NETSTREIT (NTST)

NETSTREIT focuses on maintaining a portfolio that’s nationally diversified and primarily comprised of recession-resilient retail tenants.

The majority of their tenants are necessity retail stores like Walmart, Home Depot, CVS, and Kroger, and the other big portion includes discount retail stores like Family Dollar, Dollar Tree, or Burlington.

The weighted average lease term is 9.3 years, and 83.3% of their tenants have investment grade credit or investment grade profile.

Additionally, NETSTREIT makes sure each unit performs well to ensure strong rent coverage. They gather financial information to clarify location-specific performance and perform financial analysis to assess store demand dynamics, cost structure, and liquidity profile. These procedures ensure the quality of the portfolio and the steady growth of it.

Investor Relations

NETSTREIT has abundant liquidity (more than $500 million) to support an acquisition and growth plan, and they have a well-staggered debt maturity profile (no term loan maturities until 2027). 99% of the asset base is unencumbered.

During the latest quarter, they closed on $117.5 million of investment at a blended cash yield of 7%. The weighted average lease term remaining on these investments was 10 years, and most of them (97.2%) were leased to investment grade/investment grade profile tenants.

I expect these investments to further strengthen the portfolio and bring higher dividends in the future.

The current valuation metrics indicate that NETSTREIT is severely undervalued at this point. The current P/AFFO of 12.90 and P/FFO of 13.46 is less than half of their historical average. Our ratings tracker table shows the “Strong Buy” rating with a margin of safety of 36%.

FAST Graphs

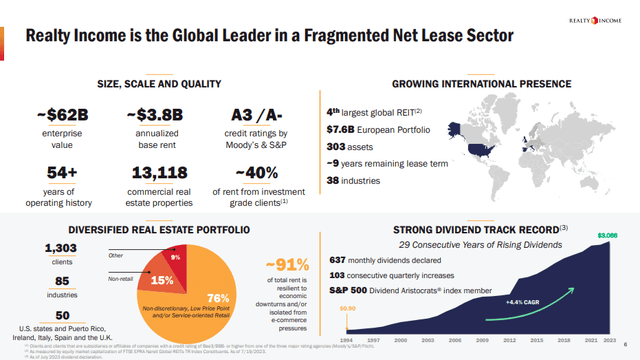

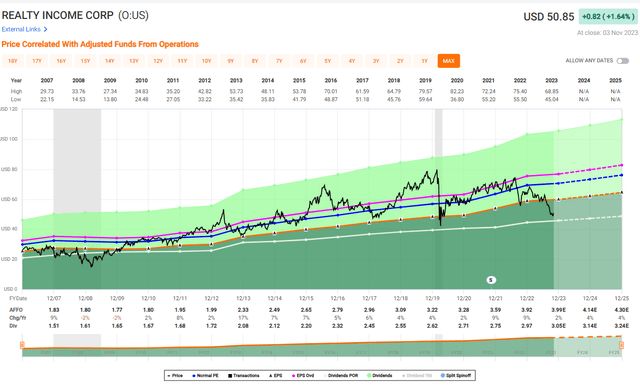

Realty Income (O)

Realty Income is a monthly dividend company, and it’s a net lease REIT that has been increasing its dividend for more than 29 consecutive years.

This impressive dividend track record will likely continue based on the strong diversified portfolio, solid balance sheet, and great operation team.

On top of that, Realty Income recently acquired Spirit Realty Capital in an all-stock transaction. The value of the transaction is approximately $9.3 billion.

This acquisition will deliver over 2.5% accretion to Realty Income’s annualized AFFO per share, and Realty Income’s already well-diversified portfolio will strengthen even further in the future.

Investor Relations

In Q3-23 Realty Income increased its 2023 FFO per share guidance by $.01, from $4.08 to $4.15, and increased acquisition guidance from $7 billion to $9 billion.

In Q3 the company invested $2 billion at a cash cap rate of 6.9% and generated same-store rental revenue growth of 2.2%.

The current valuation shows that Realty Income is significantly undervalued at this point.

The current P/AFFO of 12.71x and P/FFO of 12.40x are more than 35% discount to the five-year history. Our ratings tracker shows a Strong Buy rating with a margin of safety of 28%.

FAST Graphs

More Than 20,000 Rent Checks and Counting

We are entering another phase of uncertainty.

Or should I say that we continue to deal with uncertainty as we’ve witnessed over the last three years?

The pandemic impacted the stock market, and then quantitative easing brought the market to the highest level in a very short amount of time.

Unfortunately, the large money influx resulted in high inflation, and the very hawkish quantitative tightening was implemented by the Federal Reserve to tame inflation.

Also, several geopolitical uncertainties and high energy costs added complications.

Now, inflation seems to be calming down, but we have to worry about a recession.

It appears that we can never catch a break.

In times like this, I believe investing in real assets is a great idea, and net lease REITs are a terrific option for investors.

I don’t know if we will soon enter into a bad recession, but I certainly expect the economy to slow down substantially.

The lagging effects from high-interest rates and resumed student loans will start showing their impact on the economy soon.

I believe this will force the Federal Reserve to start to ease its monetary policy, and the net lease REIT’s stock price will take off.

In the meantime, shareholders can keep collecting their juicy dividends.

iREIT®

Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Read the full article here