")

Shares of Ovintiv (NYSE:OVV) have lagged the broader market significantly this year, losing about 15% of their value as commodity prices have come off their highs. Still, shares have rebounded significantly from their lows several months ago, given the company’s ongoing free cash flow generation. Last year, I argued shares were a strong buy, but they have fallen 10% since then. Having just reported quarterly earnings, now is an opportune time to re-evaluate Ovintiv’s prospects. While the company’s results are improving, debt reduction reduces upside, making shares just a hold in my view.

Seeking Alpha

In the company’s third quarter, it earned $1.47, which was $0.27 below consensus. However, this included $292 million in unrealized losses on its hedge portfolio, and adjusting for these mark-to market movements, earnings were in-line with expectations at $1.74. Investors in the oil & gas sector have been focused over the past two years on capital returns via either buybacks or enhanced dividends. Having spent years fixing its balance sheet, this was supposed to be the year Ovintiv could focus entirely on rewarding its shareholders.

That thesis changed earlier this year, Ovintiv acquired Permian acreage for $4.3 billion, paying about $3.1 billion in cash and the remainder in stock. Now in hindsight, OVV was ahead of the curve in terms of M&A and deepening its Permian exposure with Exxon Mobil (XOM) and Chevron (CVX) recently making much splashier acquisitions. Because of the cash portion of the deal, OVV has had a $2.6 billion increase in debt this year while also needing to spend more on cap-ex to ramp up its Permian assets.

This has meant lower shareholder returns with just $127 million last quarter. OVV pays out a base dividend, which gives shares a 2.5% yield. Beyond that, it targets 50% of remaining free cash flow in buybacks and/or special dividends and up to 50% in debt reduction. Over time, Ovintiv seeks to bring debt to EBITDA down from 1.4x currently to 1x, or about $4 billion. The need to de-lever alongside increased cap-ex spending to ramp up these new assets have greatly reduced what stock investors have received relative to initial hopes for the year.

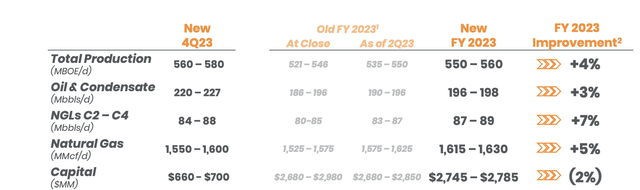

It seems to me this quarter may prove to be something of a turning point, though it will be several years before debt reduction is done. The integration of this new Permian acreage is complete, and we are now seeing strong operating results that came in ahead of guidance. In the third quarter, production was 572mboe/d (thousands of barrels of oil equivalents), above the 540-560mboe/d guidance, led by oil production of 214mbo/d (vs a 202-208 guidance). This beat on production came even as cap-ex spending was below guidance at $834 million vs $840-$890 million. Ovintiv is seeing record efficiency and strong well performance in the Permian where it allocates about half of its capital budget. Base production is also holding in better than expected as older wells decline less.

This is particularly true in its legacy assets in the Anadarko basin, which generate 119mbo/d in production. This portfolio is benefitting from shallowing base declines of just 20% from 38% in 2021. This reduces the cap-ex needed to sustain production, supporting a better free cash flow profile. While it accounts for 20% of production, less than 8% of the capital spending occurs here. Based on these strong operating results, management has upgraded guidance, increasing production while decreasing capital spending. Since closing on the Permian assets, its capital productivity has risen by 6%.

Ovintiv

Having spent aggressively to develop Permian acreage, with five working rig crews, the company is expecting moderation next year when cap-ex should be $2.1-$2.5 billion with oil production holding above 200mbo/d. As capital needs go down, we should begin to see free cash flow benefits from this purchase. Additionally, every $5 oil move has a $100 million cash flow impact, and every $0.25 move in NYMEX natural gas is worth $20 million. During Q3, oil realizations fell to $82.26 from $91.55. Natural gas realizations of $2.51 were close to the $2.55 NYMEX level as transportation costs have improved.

In Q3, OVV generated $278 million in free cash flow. Through nine months, OVV has generated $720 million in free cash flow. Thanks to lower capital spending, we should see a significant increase in Q4 with free cash flow likely to be at least $440 million for full year free cash flow of about $1.165 billion or higher.

If we hold prices commodity prices flat as we think about next year, given its lower cap-ex spend and higher average crude oil production, free cash flow should rise to at least $1.6-1.8 billion. That gives shares a 13% free cash flow yield at their current share price. Now, part of this elevated free cash flow yield is due to the fact that the company has to redirect some of its free cash flow to debt reduction.

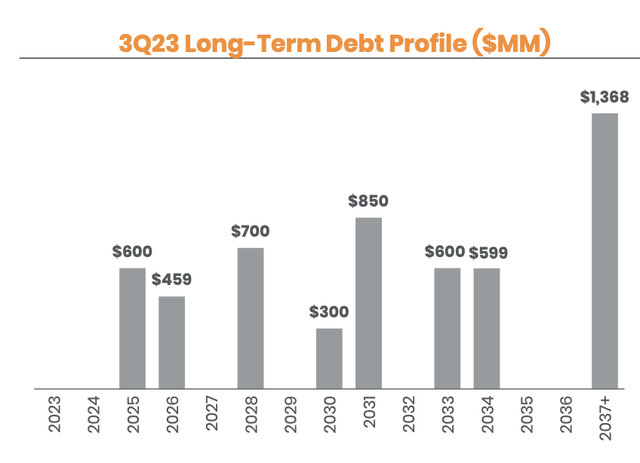

On the positive side, OVV does not have meaningful near-term maturities. As you can see below, its debt is well laddered out with the first maturity in 2025. This means OVV is not refinancing low-cost debt at today’s high interest rates. Indeed, I do not expect OVV to have to refinance any debt until 2028 at the soonest as it will be using excess cash flow to retire debt early.

Ovintiv

At the low end of my free cash flow estimates for 2024, OVV will generate $1.6 billion in free cash flow. From this, it will first pay out the base dividend. That costs the company about $325 million a year, leaving it with $1.3 billion for other capital return actions. As noted above, it seeks to use these funds 50/50 for shareholders and debt reduction. That $650 million in debt reduction will cover the company’s 2025 maturity. The remaining $650 million provides capacity to repurchase about 5% of the company’s shares at their current level.

Given Ovintiv’s $4 billion debt target, it will take about 3 years, depending on commodity prices to bring debt to target. Given its maturity profile, this is not problematic, but this delay in focusing entirely on shareholder returns has been a contributor to the stock’s underperformance, though having more oil-centric assets in one of the best basins has greatly enhanced OVV’s asset quality.

Even with debt reduction, at the current share price, investors are getting a roughly 7.5% capital return yield, with a 2.5% dividend and 5% buyback. I would note that if the stock were to rise materially, OVV may reallocate buyback funds to special dividends, but at the current share price, buybacks are likely to be the use of its excess free cash flow. A 7.5% all-in yield while the company is also paying down debt is not an unattractive place for investors to be, though it may not be sufficiently cheap to merit the long wait for an end to debt reduction.

While shares trade at a discount on a free cash flow yield, its capital return yield is not dissimilar from other oil companies, like Diamondback Energy (FANG), which return 75+% of free cash flow to investors. Now in the long-term as OVV completes its debt paydown, it is positioned to return more cash to shareholders, but three years is a lifetime in financial markets.

Still, shares should be aided by the fact that capital returns will increase next year relative to this year as cap-ex declines. Moreover, steady share count reduction will support moderate per-share cash flow growth. I view a 6-7% capital return yield as appropriate, which provides about 10% upside to shares. Having already recovered meaningful lost ground over the past three months, there is still some remaining upside, but I see other oil companies like FANG as having clearer upside, and so would rotate out of OVV. With some upside, but not as much as peers, I view shares as just a hold.

Read the full article here