")

Public Storage (NYSE:PSA) is America’s largest publicly traded self-storage REIT. The company has been exceptionally successful over the decades; it has produced a total return of more than 5,000% over the past thirty years. Management realized early on the broad market opportunity in building and rolling up vast amounts of self-storage units and has continued to execute successfully on that business plan up to the present day.

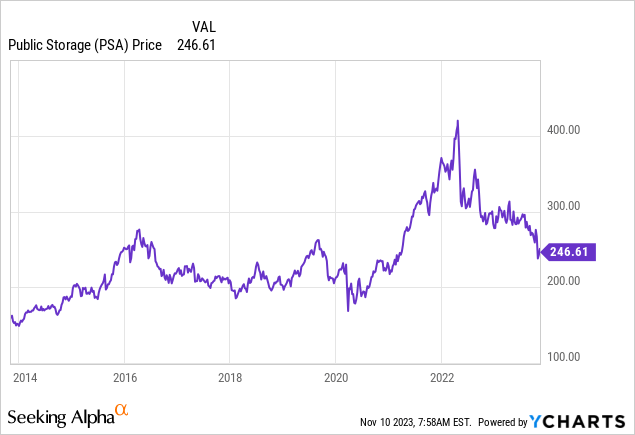

That said, Public Storage’s stock price performance has become more mixed over the past decade or so:

Shares traded roughly flat between 2015 and 2020 before doubling in recent years. However, Public Storage’s move up to $400 would be short-lived, and shares have now fallen back to prices seen in 2016. As Public Storage pays a healthy dividend, the company has still generated a positive total return, but it’s probably been far short of investor expectations over the past decade.

Public Storage: Acting Like A Bond Proxy

I covered Public Storage here on Seeking Alpha in March 2020, highlighting how shares would be a winner as interest rates plummeted with the onset of the COVID-19 pandemic. At the time, Public Storage was one of few stocks that rallied even as the market as a whole was dropping; that made sense as self-storage is a recession-resilient sector and REITs are often worth more in a falling interest rate environment.

I moved to neutral on Public Storage and the self-storage space more generally in 2022 as the interest rate dynamic reversed. Instead of low rates and lots of liquidity thanks to the government’s efforts to head off the negative effects of the pandemic, we flipped to a rising interest rates and inflation environment that was unfavorable to REITs. At the time, I suggested that I’d wait for an entry price below $300 to consider buying Public Storage shares once again.

As it would happen, interest rates ended up rising a lot farther than I would have expected, and we’ve seen a dramatic sell-off in REITs and other interest rate sensitive equities. PSA stock hasn’t just hit $300 again, it’s now fallen below $250.

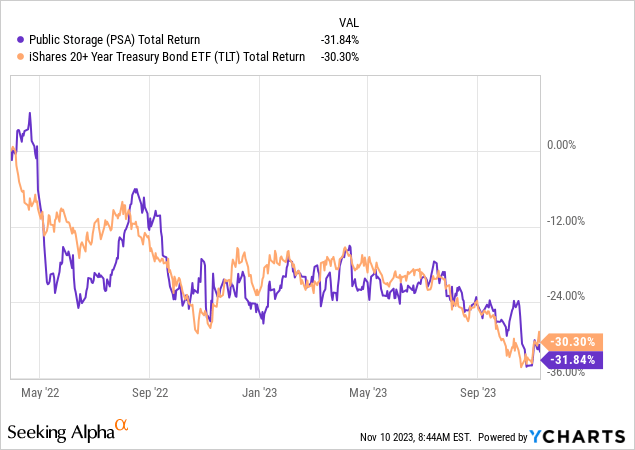

And, I’d argue, Public Storage is not trading on its own merits at the moment, but rather almost entirely based on the price of government bonds. Here is Public Storage’s total return over the past 18 months compared to the iShares 20+ Year Treasury Bond ETF (TLT):

As you can see, the correlation is quite strong, and particularly so in more recent months. A natural takeaway is that if government bonds start to rally, Public Storage should enjoy an upturn as well. It seems like Public Storage has been acting like a bond proxy in terms of its price movements since the onset of the pandemic. And yet, Public Storage’s actual underlying worth should be assessed based on the results of its storage operations, not the yield on a 30-year U.S. government bond.

Public Storage: The Business Is Fine

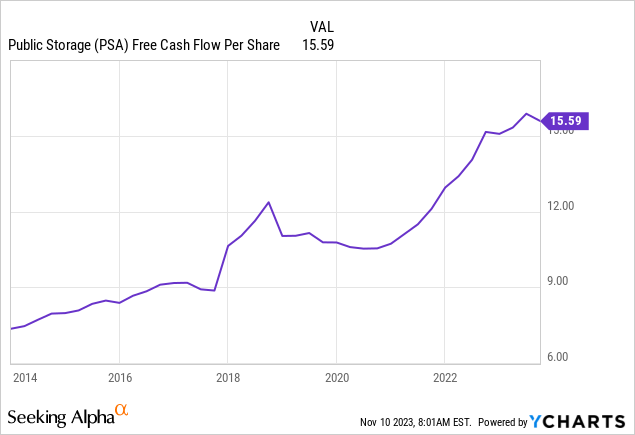

Above, we saw Public Storage’s stock chart, which has been largely flat since 2016, albeit with some volatility. Has Public Storage, the underlying business, shown similar ups and downs?

No, it hasn’t. In fact, Public Storage has created an admirable track record of strong and consistent free cash flow per share growth over the past decade:

Back in 2016, investors were receiving about $9/share in free cash flow annually when paying $250 for a share of Public Storage stock. Today, for the same $250, investors are getting more than $15/share in free cash flow. While the stock price hasn’t gone anywhere, the underlying business has dramatically improved its positioning.

Furthermore, Public Storage has increased its regular dividend from $8/share to $12/share since 2016. That’s a 50% dividend increase and results in a generous 4.9% dividend yield today. Compare that to the late 2010s, when PSA stock’s yield was usually in the 3% range. The difference is that while bond yields go up and down, Public Storage’s cash flow generation and yields have inflected higher and will keep giving investors more value regardless of where interest rates go next.

Adding to that, the company’s latest earnings report was upbeat. Q3 core FFO of $4.33 rose nicely from $4.13 last year and easily topped analyst expectations of $4.19. Same-store sales are up, and the company raised guidance. This is not the sort of earnings report you’d expect to see given the downward stock price action, and further backs up my idea that shares are simply trading as a derivate of the bond market at the moment rather than a reflection on Public Storage’s favorable fundamentals.

Before moving on, I’d also credit Public Storage’s balance sheet construction as it relates to the higher interest rate environment.

The firm funds a large portion of its capital needs by issuing preferred shares. Bears often criticized the company for paying slightly higher interest rates on preferred shares instead of issuing bonds or using bank lines of credit for funding needs. Now that interest rates have soared, however, Public Storage has locked-in preferred share funding in the low 4% range with no call date on that principal ever. This is an incredibly powerful tool in the event that interest rates remain elevated over a longer time horizon. Public Storage gave up a few basis points of interest in the 2010s but now has a durable competitive funding advantage. This is the sort of smart tactic that management teams focused on long-term value creation can obtain.

Public Storage Stock Verdict

Discerning readers may note that I do not currently have a position in PSA stock, even though I am bullish. What’s the explanation for that?

Simply put, I believe that the self-storage space as a whole is deeply oversold and set to spring back when interest rates reverse course. As such, I am bullish on pretty much all the major REITs in the sector. Given that view, I am looking for the most upside when the sector bounces back, and from my perspective, some of the smaller players like National Storage Affiliates Trust (NSA) have more upside when the tide turns — and pay a higher dividend yield today — than Public Storage.

For investors that want more certainty, however, Public Storage’s huge operating scale and strong balance sheet make it a great conservative pick within the self-storage space. While Public Storage’s all-time high stock price above $400 probably isn’t coming back anytime soon, it’s not hard to imagine PSA stock back above $300 in the near future as soon as interest rates turn and investors start bidding for dividend stocks again. Morningstar’s Suryansh Sharma agrees, with Sharma setting a $317 fair value target on Public Storage shares based on 19x funds from operations “FFO” multiple.

Given how much Public Storage continues to grow its underlying free cash flow, it should only be a matter of time until the stock price catches up with that value creation.

Read the full article here