")

Elevator engineering company Kone (OTCPK:KNYJF) recently released its Q3 2023 interim financial report. The results were solid, but there are large differences between the performance of the different business segments of Kone. Sluggish market conditions led to significantly lower sales in its new building solutions business, while the service and modernization activities are growing at a healthy rate.

Kone’s outlook implies an aggravation of these disparities, which could lead to slower mid- to long-term growth if these conditions continue. Also, its dependency on China (about a third of its sales) makes the company vulnerable.

Kone Q3 2023 results

Kone’s Q3 2023 results, which can be found here, look ok. Most of its metrics seem a continuation of developments which already were apparent in the second quarter of this year: orders received declined, while its cash flow from operations grew. What was different is that sales declined in the third quarter, albeit slightly correcting for comparable exchange rates (1.4%).

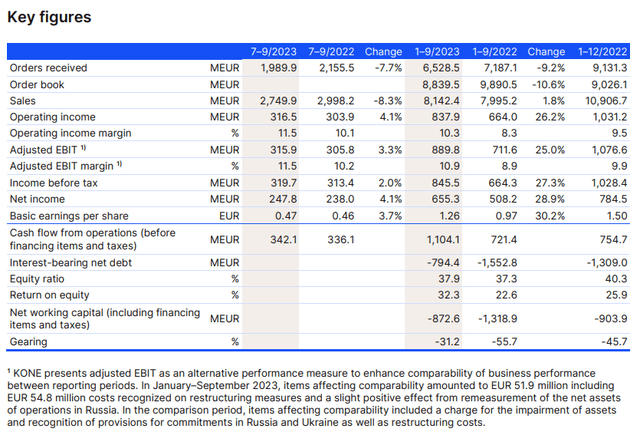

Kone’s margins and net income look especially nice in the key figures table, pasted below. The basic earnings per share increasing by 30% for the first nine months of this year is a real achievements and reflects this decent performance. This margin improvement has likely been positively influenced by the reorganization which Kone commenced, introducing a new operating model for the company.

Kone key figures Q3 2023 (Kone Q3 2023 Interim Report)

A company moving at two different speeds

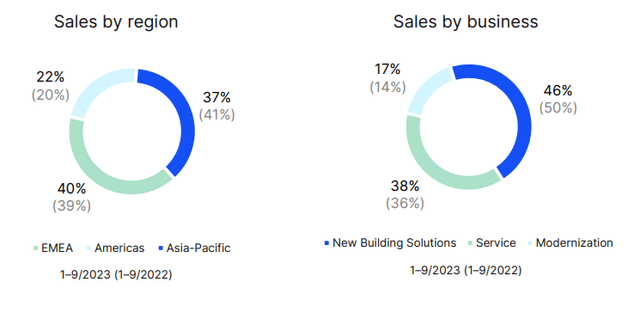

Looking at the different businesses of Kone however reveals a company with great internal differences between segments. Kone splits up its sales in three regions and three different businesses. The names of the regions and the businesses speak for themselves. In the picture below we can observe that the company is well-diversified geographically and business-wise, but also which regions and business areas showed a relative growth or decline during the past 9 months compared with the same period in 2022.

Kone sales per region and per business (Kone Q3 2023 Interim Report)

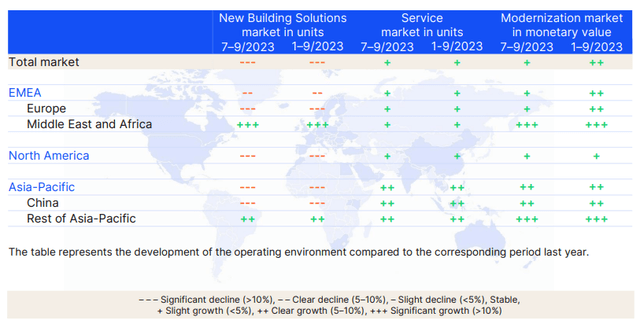

Zooming in more, even larger differences become apparent. New building solutions are declining in most geographical areas, except for Middle East and Africa and non-China Asia Pacific. Also, service and modernization markets are growing everywhere compared with the previous year, but growth is quickest where new building solutions are also still growing. This seems intuitive: for regions where market and societal conditions are beneficial for new building solutions, there will also likely be more demand for modernization of existing equipment. Service contracts are often started after completion of new building solutions or modernization projects, and as such it is logical that growth here is highest in locations which show strong current growth or have shown strong growth until relatively recently (such as China).

Kone operating environment development current year (Kone Q3 2023 Interim Report)

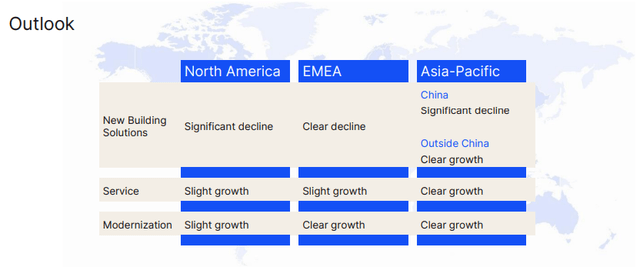

Kone’s outlook for the rest of 2023 looks more or less the same: decline for the new building solutions business, except for some smaller markets such as non-China Asia Pacific, and modest growth for modernization and service.

It is important to consider that China is a very large part of the global market of the elevator and escalator business: more than 65% of the global number of units are built in China. Kone expects the new business solutions market in China to decline by 10-15% in 2023, but judged by the remarks of the company, it could be that the worst is over. In its Q3 presentation, Kone mentions that the company regained momentum in China, with new building solutions business orders growing significantly in Q3 2023 (without mentioning the exact numbers). It is unlikely that this will already have much influence on the last three months of 2023 though, but with China currently dominating the global landscape, this is bound to be important for the next couple of years.

Kone Business Outlook 2023 (Kone Q3 2023 Interim Report)

Kone does not report individual profitability metrics for its different business segments or regions.

Bottom line

Kone’s business is seemingly moving at two different velocities at the moment: the new building solutions business is currently declining, while the modernization and service businesses are doing well with decent growth. China is still a problem for the company due to its weak consumer sentiment, but improved orders for new building solutions seem to indicate that the worst has passed. Still, the drag will continue for a while, and since China is Kone’s biggest market, this will continue to have a large impact.

The business concept of Kone is to support its customers during the entire life cycle of the equipment they are selling: installation, service and equipment. Because this cycle starts with new building solutions, a slump in this segment will eventually also have effects on service and modernization. The company has been quite successful lately in improving its margins, but for the longer term orders received will need to pick up again for continuous growth. The business of Kone seems to be less volatile than other construction business due to its long-term service and follow-up modernization commitments, but that doesn’t mean that the company is insulated from economic conditions.

Kone’s shares currently trade for a forward P/E of 22.5, and this seems expensive, especially considering the recent margin improvements of the company. But measured by TTM revenue, Kone is one of four companies dominating the elevator and escalator industry with a TTM revenue of $11.7B and as such I believe a premium is warranted. The other three peers of Kone are Otis (OTIS) with $14B, Schindler (OTC:SHLRF) with $12.6B and TK elevator (private after it was sold from parent company Thyssenkrupp (OTCPK:TYEKF) to private equity firms in 2020) with $9B. In 2019, these four companies were responsible for almost 70% of elevator sales worldwide.

If Kone can accelerate its growth and continue to increase its margins at the same time, it could prove to be a very good investment for the long term. For growth acceleration, more beneficial economic conditions are likely necessary, especially in China. I consider Kone to be a hold at this moment, that could change to a buy if the company is able to improve its margins even more or if new construction business picks up again.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here