")

Summary

Readers may find my previous coverage via this link. My previous rating was a hold as I believed FIGS (NYSE:FIGS) operating metrics would improve as its current momentum was sustainable. I am reiterating my hold rating for FIGS as its third quarter result showed continued growth and strength in its business, where its revenue and net income margin all grew double digits.

Valuation

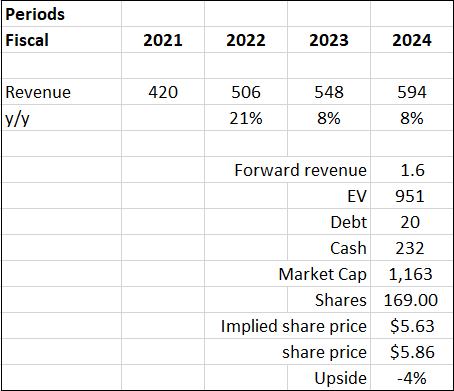

Based on my view of the business, I anticipate 8% growth in FIGS’s revenue for FY23 and FY24. This projection is based on Management’s revenue guidance of single-digit growth. The driver and factors behind this guidance are due to the continued macroeconomic uncertainty such as inflation and the central bank’s interest rate direction. In addition, the third quarter’s performance might be a result of pull-forward demand. It refers to a situation where consumers make purchases earlier than they normally would. This can happen due to anticipated price increases due to current uncertainty regarding inflation and the direction of inflation in the near future.

Currently, inflation hovers around 3.7%, still way above the targeted and healthy rate of 2%. Although inflation has come down significantly since the start of 2023, it started to take a turn around July and inflected. As a result, the pull-forward demand might worsen for the upcoming quarters and extend into 2024, given the fact that no one can predict the movement of inflation.

Based on author’s own math

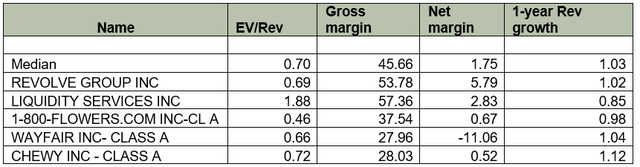

Peers overview:

FactSet

FIGS now trade at 1.6x forward revenue, which is higher than peers’ medians of 0.70x. The drivers for the higher forward revenue are FIG’s far superior margins and 1-year revenue growth outlook. In terms of gross margins, FIGS is at ~69%, whereas peers’ median is 45.66%. In terms of net margins, FIGS net margin is ~2.9%, while peers are 1.75%. The last but most significant is FIGS’s revenue growth outlook. In 2023, FIGS is expected to grow at 8%, while peers are at 3%. That is more than double of them. With a better growth outlook and margins, I think it’s fair for FIGS to be trading at a higher P/E.

With my target price nearing its current traded price, the upside potential is not attractive enough. This means that the market has already priced the strength of FIGS into its share price. On the back of these analyses, I maintain my hold rating for FIGS.

Comments

FIGS reported strong third quarter 2023 results. Compared to $128.6 million in the 2022 third quarter, net revenues increased 10.7% to $142.4 million for the third quarter of 2023. This increase was mostly attributable to a higher average order value [AOV] and an increase in orders from both new and existing customers. In that quarter, active customers increased by 19.6%, which was made possible by FIG’s persistent efforts to raise brand awareness globally and high rates of lapsed customer reactivation.

Moving onto AOV, it grew by ~2% in the third quarter year-over-year. This increase was mostly driven by higher units per transaction [UPT] and, to a lesser extent, by an increase in average unit retail [AUR]. AOV is still benefiting from the change in the product mix, which is mostly due to the popularity of outerwear and shoes. Non-scrub wear categories, such as shoes and limited-edition styles, are growing robustly. Non-scrub wear increased 26.4% to 19.3% of net revenues in the third quarter of 2023, compared to 16.9% for the third quarter of 2022.

On the surface, it might seem like FIGS is facing pressure on its margins, as it reported contractions in gross margins. The third-quarter gross margin was 68.4%, as opposed to 70.6% in 2022. The primary cause of the decline was a shift in the product mix. However, when we dive deeper into the call, FIGS demonstrated excellent cost management. In the third quarter, selling expenses reported were $32.2 million, or 22.6% of net revenues, as opposed to 24.8% in 2022. Lower fulfilment costs and leverage within shipping expenses were the drivers of the decline. Due to improved digital marketing efficiency, the third quarter’s marketing expenses were $19 million, or 13.4% of net revenues, down from 15.6% in 2022. Although gross margin contracted, FIGS effective cost management drives its third quarter net income margin to expand to 4.2% compared to 3.1% for last year.

Moving to my outlook for FIGS, I anticipate that FIGS will be under pressure from the current uncertain and tough macro environment. My perspective aligns with that of management. Starting with the top line, FIGS projects single-digit net revenue growth in the fourth quarter, reflecting continued macroeconomic uncertainty and acknowledging that, given the third quarter’s outperformance, there may have been some pull forward in demand. They anticipate that, until at least the first half of 2024, the macroenvironment will continue to have an impact on consumers. Regarding gross margin for the fourth quarter, FIGS anticipates that a change in the mix of products and promotions will balance out improved freight costs. Therefore, I do not foresee any strengthening or weakening of its gross margins. Lastly, FIGS anticipate that the initial start-up costs for its fulfilment enhancement project will come to about $2 million. It is anticipated that these high expenses will persist through the first three quarters of 2024. From these, I can infer that margins will be facing pressure when FIGS report its 2024 numbers, as they have already warned us.

Risk & conclusion

One upside risk to my hold rating would be the possibility that FIGS’s growth and margin beat the optimistic expectations that are guided by management. In the current challenging environment, FIGS continue to grow its revenue in the third quarter of 2023. On top of that, it also manages to reduce its operating expenses and expand its net margins, even though inflation is high. This speaks volumes about FIGS’s business model as well as its cost management effectiveness. In this scenario, FIGS P/E might expand, which leads to share price appreciation.

In conclusion, FIGS’s third quarter result is robust and impressive. Its revenue grew by double digits despite a challenging macroeconomic landscape plagued by high inflation and interest rate hikes. Although the gross margin compressed slightly, this did not negatively impact its bottom line. Due to its excellent and efficient cost management, FIGS instead managed to expand its net income by 1.1% to 4.2% for the third quarter of 2023. In my opinion, this is very impressive given the fact that high inflation has generally increased most companies costs and contracted their margins. Lastly, when compared to peers, FIGS surpass and outshines all of them in terms of margins and growth outlook. However, the lack of an attractive share price gains leads me to maintain my hold rating for FIGS.

Read the full article here