")

The Kraft Heinz Company (NASDAQ:KHC), a significant player in the global food and beverage industry, showcased modest growth in Q3 2023 earnings. The company witnessed a slight increase in net sales, despite facing headwinds from foreign currency fluctuations and divestitures. There was an increase in organic net sales compared to the previous year, primarily driven by a significant price increase across both reportable segments to mitigate higher input costs. However, this price increase also led to a noticeable decline in volume/mix, reflecting the elasticity impacts of the pricing actions. This article delves into the technical analysis of Kraft Heinz’s stock price, mainly focusing on the recent trends following the announcement of Q3 earnings. The analysis highlights a robust recovery in the stock price, underpinned by a solid support level.

An Overview of Kraft Heinz’s Q3 2023 Earnings

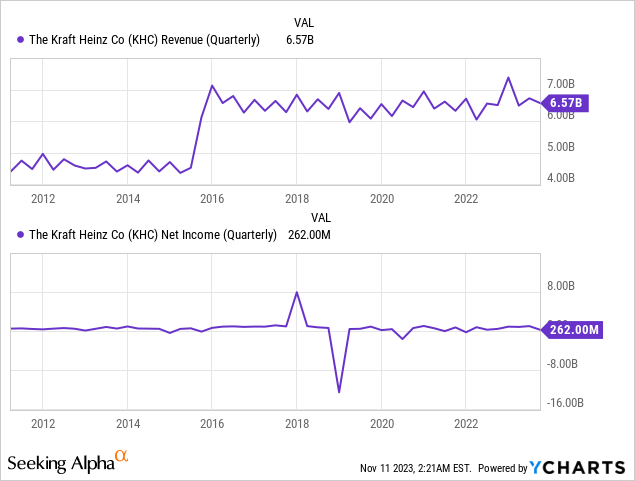

Kraft Heinz recently announced financial results for Q3 2023, reflecting growth and challenges. The company reported a 1.0% increase in net sales, reaching $6.57 billion, a modest rise influenced by several factors. A negative impact from foreign currency fluctuations and divestitures partly offset the growth in net sales. Despite these headwinds, the company achieved an organic net sales increase of 1.7% compared to the previous year. A significant driver of this revenue growth was a 7.1% increase in prices across both reportable segments, aimed at mitigating higher input costs. However, this pricing strategy led to a 5.4% decline in volume/mix, reflecting the elasticity impacts of these pricing actions. In other words, the price increases led to a decrease in the quantity of products sold.

However, the company’s net income presented a less favorable picture, decreasing by 41.7% to $262 million, as shown in the chart below. This decline was primarily attributed to higher non-cash impairment losses and increased tax expenses. Despite these challenges, Kraft Heinz saw an 11.9% increase in Adjusted EBITDA, reaching $1.6 billion. This increase was mainly driven by the higher pricing and efficiency gains, which helped offset rising supply chain costs, unfavorable volume/mix, and investments in marketing, technology, and research and development.

Moreover, EPS declined, with diluted EPS down by 40.0% at $0.21. However, Adjusted EPS, which can offer a clearer view of a company’s operating performance, was up by 14.3%, at $0.72. This increase was primarily due to the higher Adjusted EBITDA and favorable changes in other expenses/income, despite higher taxes on adjusted earnings.

From a cash flow perspective, the company showed a strong performance. Net cash provided by operating activities was $2.6 billion, a significant increase of 72.8% compared to the previous year. This improvement was driven by lower cash outflows for inventories, higher Adjusted EBITDA, and lower cash outflows for tax payments. The year-to-date Free Cash Flow stood at $1.8 billion, marking a remarkable 108.2% increase, benefiting from the same factors that boosted operating cash flow, despite increased capital expenditures.

In addition to financial metrics, Kraft Heinz announced key leadership and organizational changes in Q3 2023. The company named a new President for its North America Zone. It restructured its International Zone into three distinct regions to optimize growth potential and leverage global expertise and resources. These changes are part of Kraft Heinz’s strategy to drive profitable growth and innovation in the food industry.

Overall, Kraft Heinz’s Q3 2023 results indicate a company navigating a complex market environment, balancing pricing strategies with volume impacts, and making strategic decisions to strengthen its financial and operational footing for future growth. These financials, marked by strategic adaptability and robust cash flow amidst market challenges, highlight its potential as a resilient and forward-looking investment.

Kraft Heinz Price Action Through Historical Context

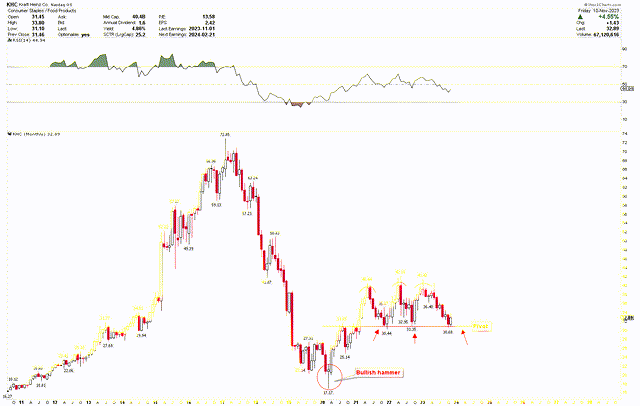

The monthly chart below presents a robustly bullish technical perspective for Kraft Heinz. In 2020, the stock established a solid base at $17.17 before embarking on an upward trajectory characterized by a bullish price pattern. Historically, Kraft Heinz demonstrated notable resilience and strength from 2011 to 2016. This significant rise was primarily attributed to strategic moves and market conditions that favorably impacted investor perceptions and the company’s financial performance. In 2015, the merger between Kraft Foods and H.J. Heinz, orchestrated by Berkshire Hathaway and 3G Capital, created a food industry giant with a vast portfolio of iconic brands, leading to synergies and cost-cutting measures that boosted profitability. The merger was a positive step towards consolidating the fragmented food industry, promising greater market dominance and efficiency.

KHC Monthly Chart (stockcharts.com)

During this period, Kraft Heinz benefited from a consumer trend towards familiar and comfort food brands, which many of its products represent. Moreover, the company’s focus on reducing overhead costs and improving operational efficiency appealed to investors, as reflected in its stock price. This significant rally peaked at $72.85 in February 2017, followed by a considerable decline.

This price drop was largely due to operational challenges and changing market dynamics. One of the critical factors was the company’s struggle to adapt to rapidly evolving consumer preferences towards healthier and more natural foods, which led to a decline in sales for many of its traditional, processed food products. This shift in consumer behavior caught Kraft Heinz off-guard, showcasing a disconnect between its product portfolio and emerging market trends. Additionally, the aggressive cost-cutting measures that initially drove profitability post-merger began to backfire, as they resulted in underinvestment in brand innovation and marketing, hindering the company’s ability to compete effectively in a highly competitive market.

Furthermore, in early 2019, Kraft Heinz reported a $15.4 billion write-down on its Kraft and Oscar Mayer brands, significantly eroding investor confidence and raising concerns about the company’s long-term growth prospects. This financial setback, with a dividend cut and ongoing concerns about high levels of debt, further fuelled the negative sentiment among investors, leading to a steep decline in the stock price.

However, the stock price showed signs of recovery and appeared to bottom out due to strategic shifts and external factors. The company’s renewed focus on streamlining its product portfolio and increased consumer demand for packaged foods amid the COVID-19 pandemic helped improve its financial performance and investor confidence. The price momentum has faced significant resistance in the $40 range, as indicated by the triple top formation at $40.44, $42.10, and $41.42 in the monthly chart. This pattern led to a decline in price, pushing it back towards the robust support level near $30.68 in October 2023. Given its repeated testing following the notable price recovery post-Covid-19 pandemic, this support level has become pivotal. In November, there’s been a notable upward movement following the announcement of Q3 earnings, underscoring the strength in price. This bullish trend is further supported by historical upward movements, particularly highlighted by the bullish hammer pattern seen in March 2020 at $17.17.

Understanding Price Strength at Pivotal Regions and Investor Consideration

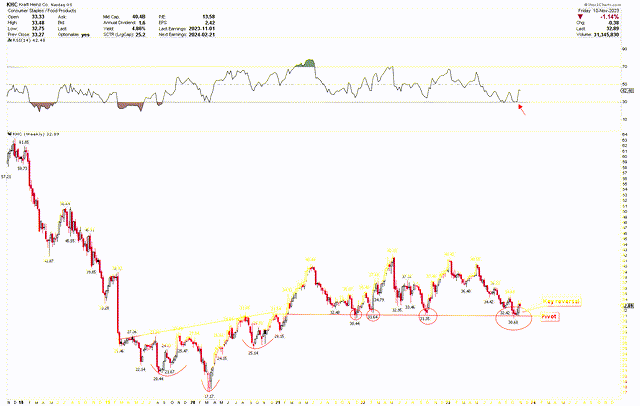

To gain a deeper insight into the optimistic outlook, let’s examine the weekly chart, which sheds light on the price movements following the Covid-19 pandemic. Notably, the post-2020 recovery was underpinned by an inverted head and shoulders pattern, with the head at $17.17 and shoulders at $20.44 and $25.14. This pattern was decisively breached in 2021, leading to consolidation above the breakout level, now deemed the pivotal point of this bullish surge.

The red circles along this critical line highlight significant price reversals following contact with this support level. The first week of November’s weekly essential reversal candle underscores robust price momentum, suggesting a potential further climb in price. Additionally, the RSI’s bounce back from oversold conditions signals strong bullish momentum.

KHC Weekly Chart (stockcharts.com)

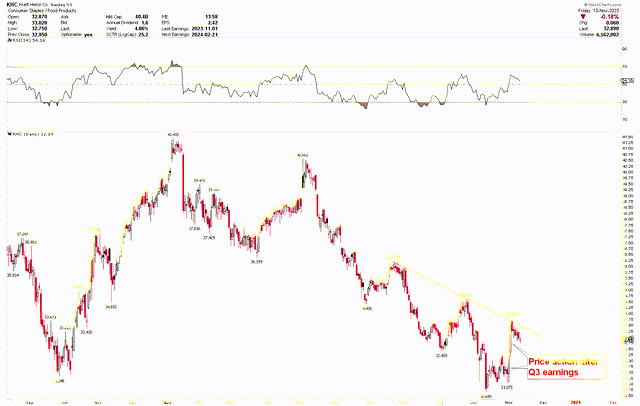

Moreover, the daily chart presents the price trajectory post-earnings announcement, which illustrates a marked upward movement, reinforcing the bullish narrative. This chart also indicates that breaching the $34 level could trigger a substantial short-term uptrend.

KHC Daily Chart (stockcharts.com)

This analysis shows that the price has demonstrated resilience around the pivotal zone of $30, backed by a bullish key reversal on the weekly chart and robust movements on the daily chart. The historical inverted head and shoulders pattern further confirms the market’s strength, making it a viable option for investors to consider entering at the current price. The stock is poised for a rally, provided it continues to close above $30.

Market Risk

Kraft Heinz faces several market risks, particularly in pricing strategy and consumer demand. The company’s decision to increase prices to offset higher input costs led to a 5.4% decline in volume/mix, highlighting significant price elasticity. This suggests that consumers are sensitive to price changes, and further price hikes could exacerbate this decline, negatively impacting revenues. Additionally, operational and strategic risks loom, evidenced by the company’s recent leadership and organizational changes. While these changes aim to enhance performance, they carry inherent risks of execution and transitional disruptions.

The competitive landscape and internal operational challenges also pose significant risks to Kraft Heinz. Intense competition in the food and beverage industry threatens its market share, especially given past brand innovation and marketing investment issues. Moreover, global economic and political factors, such as inflation and supply chain disruptions, could impact the company’s cost structure and efficiency, indirectly affecting consumer demand.

The stock’s technical analysis reveals risks; despite showing signs of recovery, there is noticeable resistance around the $40 mark and crucial support at approximately $30.68. If the monthly closing falls below $30, it will counter the positive outlook and trigger the activation of a triple-top pattern on the monthly chart. This emergence of the triple top suggests a potential further downturn in the market.

Bottom Line

In conclusion, the Q3 2023 earnings for Kraft Heinz have measured growth amidst a challenging market environment. The modest increase in net sales and a decline in net income illustrate the company’s delicate balance between pricing strategies and volume impacts. This balance is critical as the company navigates through market headwinds such as foreign currency fluctuations, divestitures, and shifting consumer preferences.

The technical analysis of Kraft Heinz’s stock reveals a cautiously optimistic outlook. The recovery in the stock price, particularly following the Q3 earnings announcement, reflects investor confidence in the company’s strategic direction and resilience. The stock’s historical performance and current technical indicators suggest a potential for upward momentum, especially with the stock showing strength around the pivotal $30 zone. The appearance of a bullish hammer in the 2020 monthly chart establishes a historically positive trend, and a significant reversal candle following the Q3 earnings, notably from the crucial $30 mark on the weekly chart, underscores the stock’s robust outlook. This suggests that investors might consider buying the stock at its present value in anticipation of additional upward movement. Nevertheless, a monthly closing under $30 would signal increasing downward momentum in the market.

Read the full article here