")

In this article, we catch up on the Q3 results of Carlyle Secured Lending (NASDAQ:CGBD). CGBD trades at a dividend yield of 11.9% and a 13% discount to NAV. Its net investment income price yield is 14.5% – around 0.4% above the sector average.

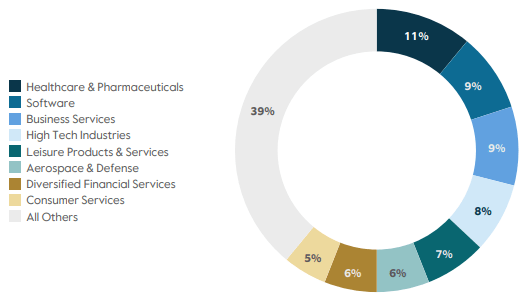

CGBD has a fairly typical BDC portfolio profile with an 80%+ first lien allocation. Its median company EBITDA of $80m is also in the sweet spot of the middle-market segment. Its sector exposure is tilted to Healthcare and Software – fairly common in the BDC space.

CGBD

Quarter Update

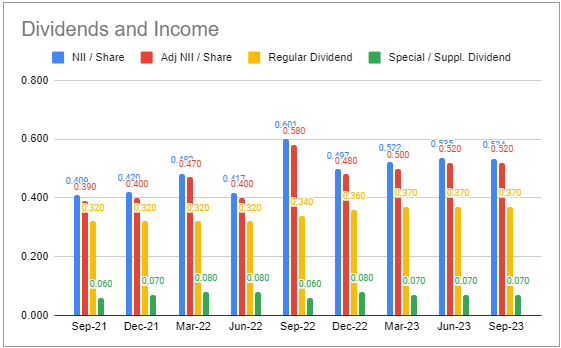

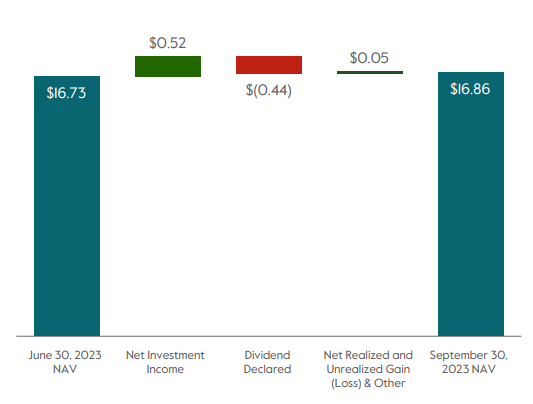

Adjusted net income came in at $0.52 – flat to the previous quarter. The increase in total investment income was roughly matched by the increase in interest expense and a larger tax accrual.

Systematic Income BDC Tool

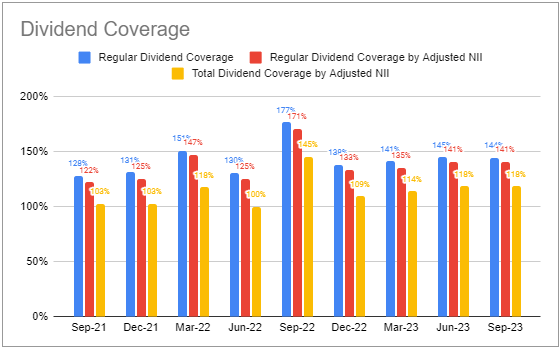

The company declared the same base dividend of $0.37 and supplemental of $0.07 as the previous quarter. Base dividend coverage remained at a very high 141% with total dividend coverage standing at 118%.

Systematic Income BDC Tool

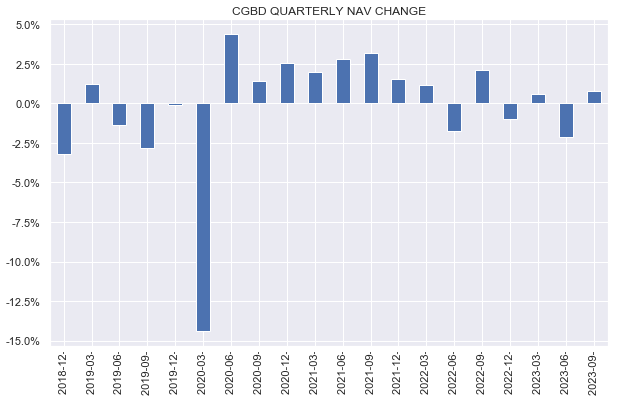

The NAV rose by 0.8%, offsetting some of the drop the previous quarter.

Systematic Income

This rise was primarily due to retained income as well as unrealized appreciation. Year-to-date, the company is still carrying $0.35 of net unrealized depreciation.

CGBD

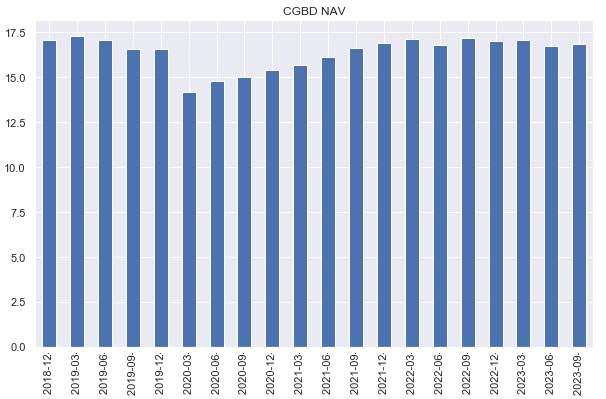

Overall, the NAV has been relatively stable over the last couple of years, particularly over the COVID period which is good to see.

Systematic Income

Income Dynamics

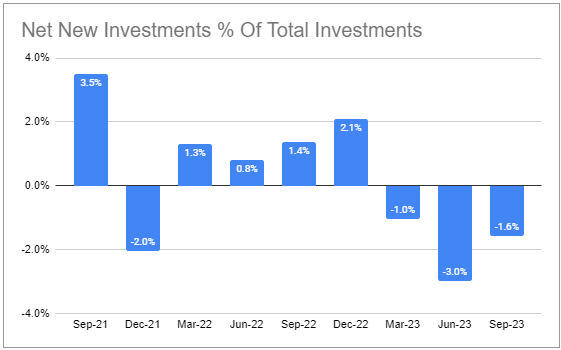

Net new investments were negative for the third quarter in a row as repayments and sales exceeded new fundings.

Systematic Income BDC Tool

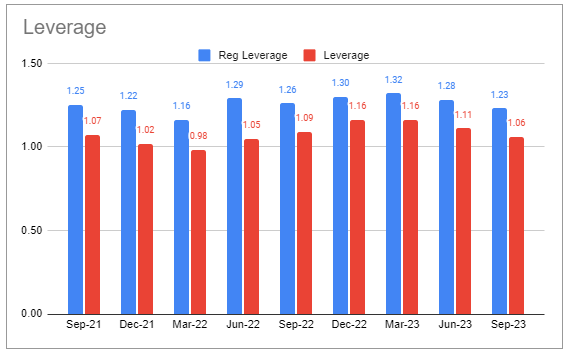

Combined with a rising NAV, leverage, therefore, ticked lower once again. According to management, they are intentionally running leverage at the lower end of its target range to take advantage of forthcoming lending opportunities. Given the tightening in credit spreads and the fact that marginal lending is financed with relatively expensive credit facilities (with interest expense around 7.3% and total expenses close to 9%) this makes a lot of sense.

Systematic Income BDC Tool

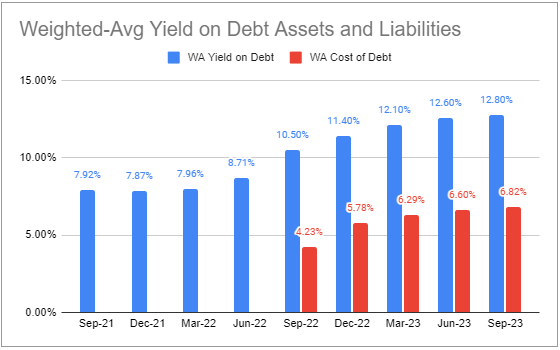

Both asset yield and interest expense rose by about the same amount. The company has a relatively high amount of floating-rate debt at 80% which is well above the sector average. This means its interest expense has increased more quickly relative to most other BDCs.

Systematic Income BDC Tool

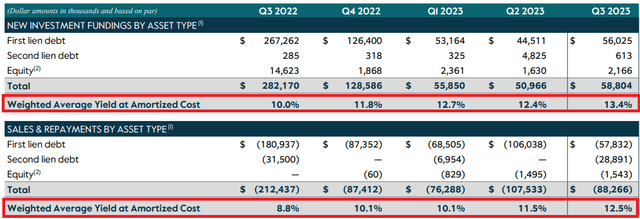

The yield on new fundings continues to run ahead of the yield on repayments which provides another marginal net income tailwind.

CGBD

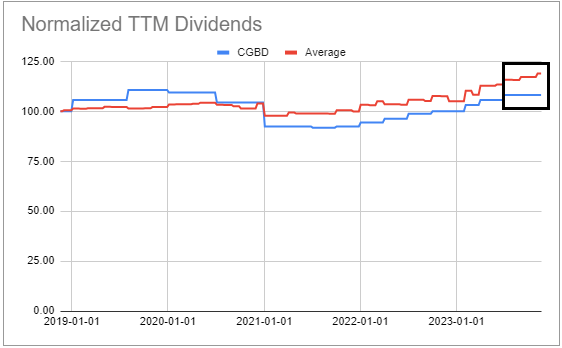

Overall, the company’s net income profile has not risen as much as the broader sector in the last several quarters. This is in large part due to a high level of floating-rate debt as well as the organic deleveraging of the portfolio. This is also largely why its dividend trajectory has lagged that of the broader sector in recent quarters. That said, if the Fed does take the policy rate substantially lower, CGBD could be a beneficiary as it will also enjoy an outsized drop in its interest expense.

Systematic Income BDC Tool

Portfolio Quality

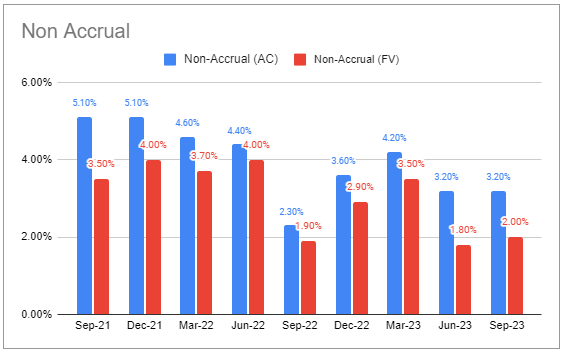

There were no new non-accruals in the last quarter and the uptick in fair-value was due to a write-up of two existing non-accrual positions.

Systematic Income BDC Tool

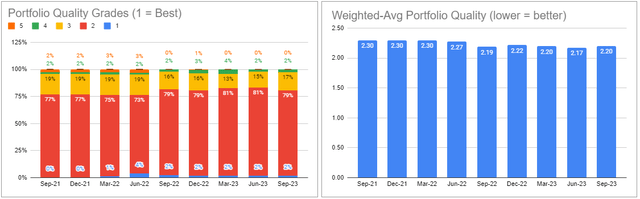

As far as internal portfolio quality metrics, the number of holdings in the worst two buckets stayed flat.

Systematic Income BDC Tool

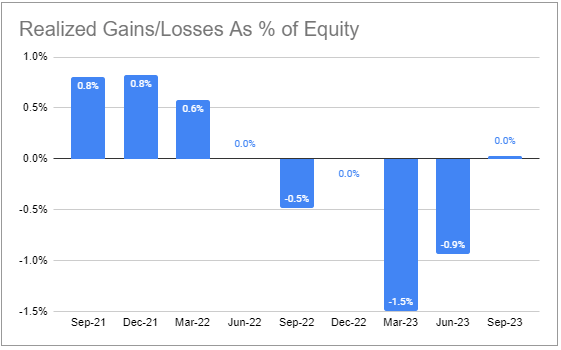

There was a small net realized gain which was a welcome respite from net realized losses in the last two quarters.

Systematic Income BDC Tool

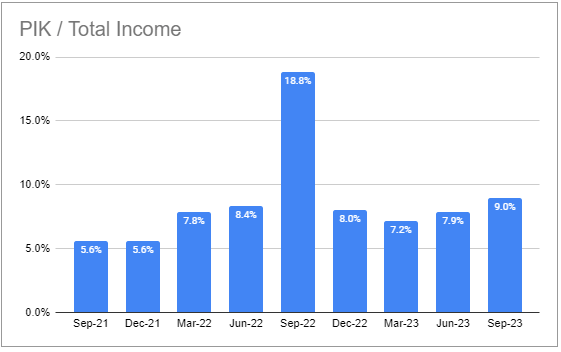

PIK remains a bit above the sector average.

Systematic Income BDC Tool

Valuation And Return Profile

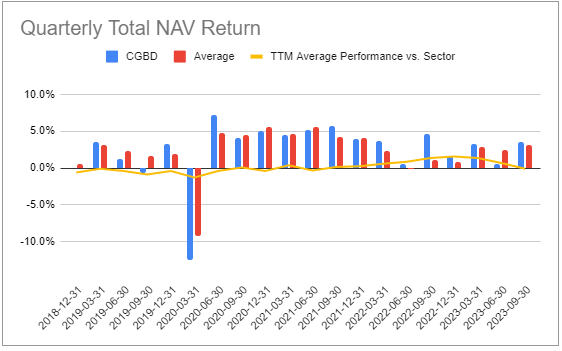

Apart from an underperforming Q2, CGBD has outperformed the sector since 2022.

Systematic Income BDC Tool

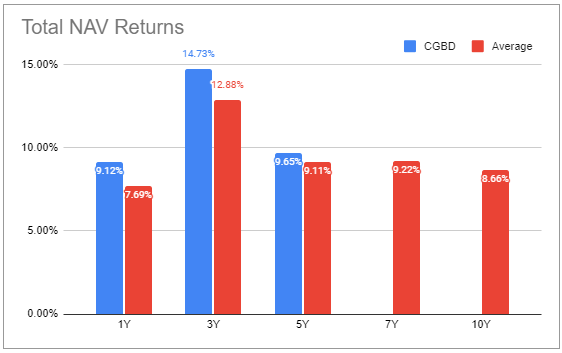

Over longer-time periods, its performance has exceeded the broader sector.

Systematic Income BDC Tool

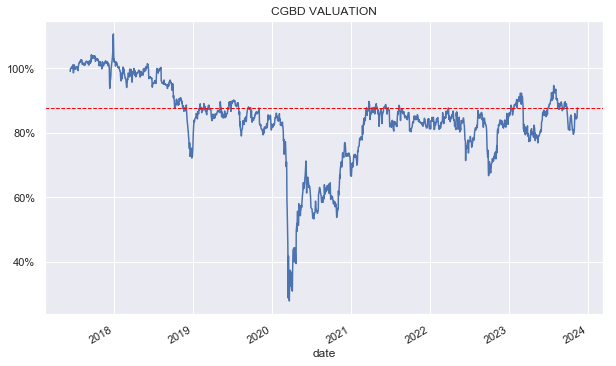

CGBD has traded fairly consistently at a discount over the last few years.

Systematic Income

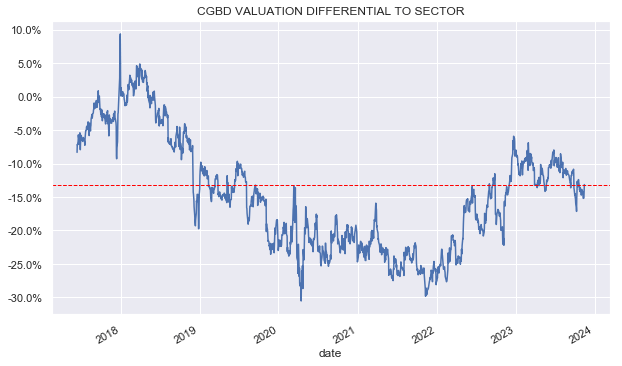

It also remains at a double-digit discount versus the sector average though that’s an improvement over the 20-30% lower valuation that we tended to see until this year.

Systematic Income

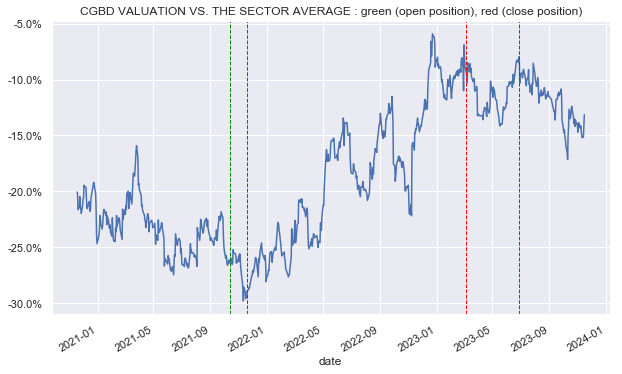

We added the bulk of our CGBD position at the end of 2021 when it was trading at a huge discount to the sector (green lines). More recently we pared back the allocation when its relative valuation discount moved into the single-digits (red lines). We continue to carry a moderate position to the stock and would look to top it up if its relative discount widens from here.

Systematic Income

Read the full article here