")

Shares of First Horizon Corporation (NYSE:FHN) have been a particularly poor performer over the past year. Like essentially all regional banks, FHN has been negatively impacted by higher funding costs in the wake of Silicon Valley Bank’s failure. Further, in May, TD Bank (TD) ended its efforts to acquire First Horizon after failing to receive a timeline for regulatory approval; as a result, it paid FHN $225 million. It is important to emphasize this was due to a slow regulatory process and not problems with FHN’s business. Shares have recovered somewhat from their lows, but they remain down 45% from last year.

However, FHN is now a well-capitalized bank, which should enable it to consider meaningful share repurchases over the next year. Additionally, the headwinds on its net interest margin should begin to ease. This combination can lift shares at least another 10% past $15, creating a 15% total return opportunity. At a December conference, management guided to 1-4% growth in net interest income, 4-6% growth in fee revenue and 4-6% growth in expenses, as it invests in technology. I view these targets as credible, given recent trends, providing over $1.50-$1.60 in 2024 EPS potential

Seeking Alpha

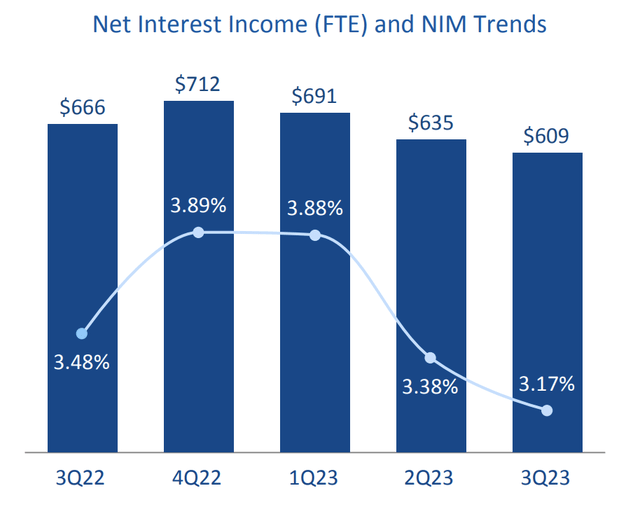

In the company’s third quarter, First Horizon earned $0.27 in adjusted EPS. These results beat the consensus by $0.03. FHN has seen a meaningful squeeze in its net interest margin (NIM) as funding costs have risen more quickly than asset yields, alongside a decline in fixed income underwriting fees. Last quarter, its 3.17% net interest margin (NIM) fell 21bp sequentially and 72bp so far this year. This is about a $57 million headwind from last year, or about $0.08 of EPS all by itself. While this sequential drop was quite large, it did moderate from the 50bp drop seen in the prior quarter after SVB failed.

First Horizon

Deposit rates and mix were a 42bp drag sequentially, twice the benefit from higher loan rate, making them the primary driver of the NIM decline. On the more positive side, FHN was able to repay all FHLB borrowings as liquidity has improved—this funding is over 5%, making it more costly than deposits. We also are seeing some evidence that the pressures from deposits have peaked. FHN is paying an average deposit rate of 3.36% on interest-bearing accounts. However, it reduced base rates in the latter part of the quarter by 10bp.

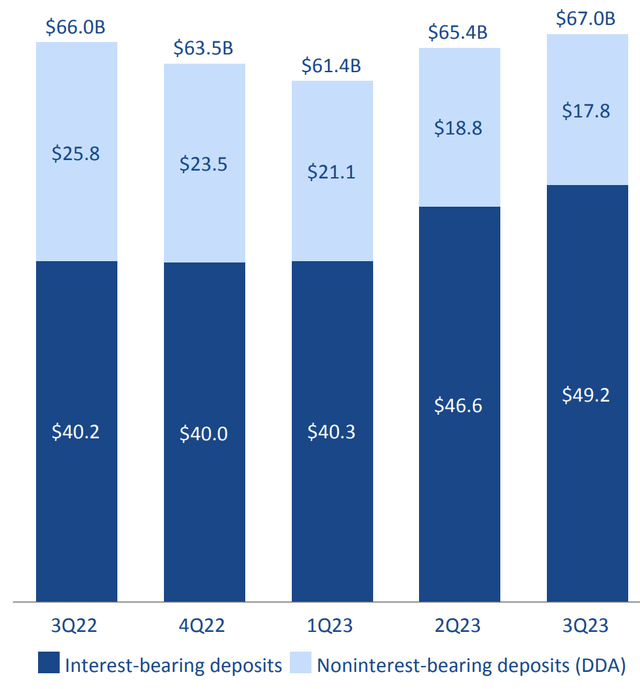

As the deposit turmoil occurred in Q1 and Q2, FHN materially stepped up the rate it offered on deposits to stem the outflows. This proved effective. As you can see below, deposits fell by $4.6 billion from Q3 2022 through Q1 2023, but they have since recovered by $5.6 billion. This growth has been entirely from interest-bearing accounts with non-interest-bearing deposits continuing to fall, though the $1 billion drop in Q3 was the slowest in over a year, suggest a bottom could be approaching. 68% of its deposits are insured or collateralized, roughly average for the industry.

First Horizon

Deposits rose by $1.6 billion in Q3 to $67 billion even as the company began to pull-back on pricing, suggesting it has some further room to reduce rates, having overshot peers. Moreover, it has $6 billion of high-cost time deposits acquired after Silicon Valley’s bank failure that roll-off over the coming months. As these are replaced at lower rates, we should see some improvement in NIM.

Critically, with deposits having recovered, the strains on First Horizon’s liquidity have eased. This is why it repaid FHLB borrowings. The bank’s loan-to-deposit ratio improved from 94% to 92% as well. This is still above the 87% registered last year. This is because loan balances are up 8% from last year to $61.8 billion, whereas deposits are up 1.7%. Loan growth has slowed, though, rising just $0.5 billion last quarter. I would expect loan growth to be slower than deposit growth over the next year, at least until loan-to-deposits fall back under 90%.

FHN has historically been a conservative lender with solid underwriting results. However, last quarter, provisions rose from $50 million to $110 million. This was as net charge-offs rose to 0.61% last quarter due to a $72 million idiosyncratic item. Otherwise, charge-offs would have been a solid 0.15%. Based on a third-party valuation, management expected a large recovery on this credit during the Chapter 11 process, instead of losing its entire $72 million loan. As such, it has retained outside counsel to attempt a recovery after the surprise liquidation. The timing or magnitude of such a recovery is unknowable.

Sometimes, idiosyncratic losses due occur, and this is not a condemnation of the bank’s entire underwriting process. At the least, annualizing the charge-off impact is overly punitive, as there are unlikely to be similar one-time charge-offs every quarter, with this charge-off having just a ~12bp impact for the full year. So long as items like this do not recur, pro forma baseline quarterly EPS is closer to $0.37 than the reported $0.27.

Aside from this loan, First Horizon has $394 million of nonperforming loans, down $8 million from Q2, pointing to a relatively stable credit environment. It added $15 million to provisions, or $842 million, covering 1.36% of loans. This provides 214% of coverage for its nonperforming loans; I view 250%+ as a strong level of reserves, and so I would expect to see modest reserve builds over the next year, consistent with this year’s results.

While 23% of its loans are in commercial real estate, only 2% are in office, the sector which I view as most challenged. These buildings on average also have a relatively high occupancy rate of 89% relative to the Southeast region’s 83% average. This speaks to the higher quality of the buildings to which FHN lends. While we may see some incremental losses here, given its small share of loans, I view this challenge as manageable.

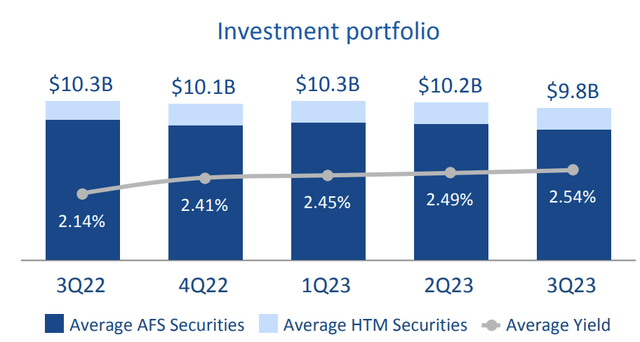

Like other banks, FHN has a securities portfolio of fixed income securities, purchased when rates were lower, leaving it with a substantial unrealized loss. As you can see below, FHN has strategically allowed this portfolio to shrink by not reinvesting all principal payments, another way in which it has built liquidity. As lower yielding debt matures, the yield on this portfolio is gradually rising. This portfolio has a 5-year duration with about $1 billion in annual cash flows. While it has a $1.8 billion unrealized loss, which sits in accumulated other comprehensive income, maturities and the pull to par as bonds near maturity will gradually reduce this loss.

First Horizon

FHN has a strong common equity tier 1 (CET1) capital ratio of 11.1%. Management targets a long-term capital ratio of 9.5-10.5%, leaving it with an excess capital position. Because FHN has less than $100 billion in assets, it will not need to factor AOCI into its capital calculations. If we did, though, capital is about 9.3%. Management is cognizant of this true economic capital position, which is why it is running at a higher reported capital level. The company aims to stay around 11% in 2024, rather than build further capital, since even pro forma capital is approaching targeted levels. This means it can return generated capital to investors via the dividend and a resumed buyback program.

As noted earlier, FHN has $6 billion of high-cost deposits rolling off. Additionally, it has $4 billion in loans at 4.2% and $1 billion of securities at 2.3% As these funds are re-deployed, they can drive the net interest income growth FHN is forecasting. Assuming a similar pace of credit reserves and these benefits to NIM, earnings should be $0.37-$0.42 a quarter next year, or about $1.50-$1.60.

FHN pays a $0.60 annualized dividend, and we are likely to see it retain some capital as assets growth, but that leaves about $250-300 million in buyback capacity to keep capital ratios flat, enough to buy back up 3.5-4% of shares, for an all-in capital return yield of 8%. That is an attractive return level, and thanks to its higher capital ratios, FHN should begin repurchasing shares more quickly than most banks. I believe this can push its multiple towards 9-10x earnings, or $15-16 a share. While shares may not recover all losses, they do have room for substantial further recovery.

Read the full article here