")

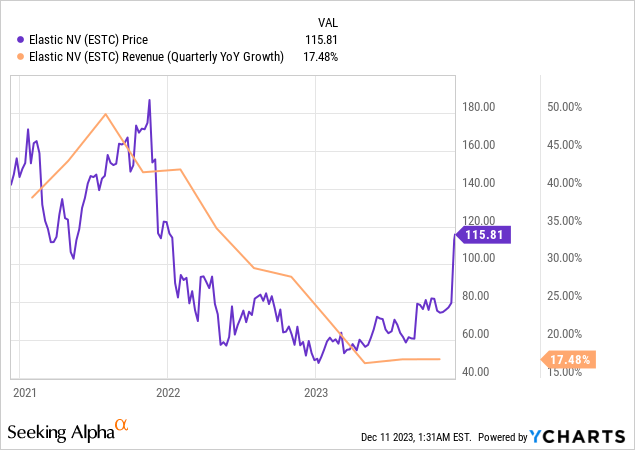

The last several years have been difficult for an emerging cloud company like Elastic (NYSE:ESTC). Like most rapidly growing, unprofitable companies, high inflation, war, supply chain disruptions, and other problems that ravaged a post-pandemic economy hurt the company’s fundamentals. Things only got worse when cloud customers of all sizes decided to optimize cloud spending in reaction to a slowing economy in the third quarter of 2022. Cloud optimization is when companies look for ways to use cloud resources more efficiently, often leading to companies shelling out less for various cloud services, thereby reducing revenue growth for cloud providers. The one-two punch of a worsening economy and a rising cloud optimization trend was at least part of why quarterly revenue dropped from around 50% year-over-year at the end of 2021 to approximately 17% as of its second quarter fiscal 2024 earnings report. Until the start of 2023, the stock price decreased in line with the fall in revenue, as seen in the chart below.

When the company beat analysts’ Q2 revenue and earnings guidance for its recently reported quarter and bumped up guidance for Fiscal Year 2024 revenue, non-GAAP operating margin, and non-GAAP earnings-per-share (“EPS”), investors may have started believing that the worst of the downturn is over, and the stock may have bottomed out. Additionally, Elastic performs a service that can help make generative artificial intelligence(“AI”) responses more accurate. The company promotes that it “powers the generative AI era.” Since investors’ use of AI as an investment theme has increased in popularity, the stock has recently gained traction.

This article will discuss Elastic’s services, its long-term opportunity, some risks of investing in the company, the stock’s valuation, and why I believe it is a Hold.

What the company does

Elastic describes itself in its latest 10-K as “a data analytics company built on the power of search.” The company was a pioneer in providing an open-source solution for developers to build custom search engines. Its main product, Elasticsearch, is one of the most heavily used open-source search engines; the company estimates that users have downloaded the tool more than 3.6 billion times! People have used ElasticSearch to conduct all types of inquiries, including searches for movies, music, books on media platforms, personal product recommendations on e-commerce platforms, government public records inquiries, medical records searches in healthcare, internal company database searches, and more. Some of its more prominent customers are Shopify (SHOP), Tinder, Goldman Sachs (GS), Uber (UBER), and Ticketmaster.

It also has “out-of-the-box solutions” for Observability and Security. DevOps teams use Elastic’s Observability tools to monitor and troubleshoot applications and Information Technology (“IT”) infrastructure like servers and networks. Elastic Security is a solution that helps security professionals collect, analyze, and respond to malware and other security threats on a company’s network, mobile devices, computers, servers, Internet of Things (“IoT”) devices, and cloud instances. Although Observability and Security offer distinct solutions, both rely on the Elastic platform’s core search functionality.

Elastic Second Quarter FY 2024 Investor Presentation.

Customers can access the products on the Elastic platform in two ways: through a self-managed on-premises version and a managed service on major cloud providers, including Amazon’s (AMZN) AWS (Amazon Web Service), Alphabet’s (GOOGL) (GOOG) Google Cloud Platform (“GCP”), and Microsoft’s (MSFT) cloud platform, Azure. As of the end of the second quarter of FY 2024, Elastic’s managed cloud service made up 43% of total revenue, up from 39% in the first quarter of FY 2023. Although the company has not publicly stated that it desires to become a 100% cloud company, Elastic Cloud is growing more rapidly than the self-managed on-prem version and drives most of its revenue growth. Since the overall trend with companies in all industries is biased towards cloud adoption, it’s vital to see Elastic produce strong growth in its cloud computing products.

The company uses a “land and expand” sales model. In the following chart, number one signifies a customer landing in either Elastic’s Enterprise Search, Observability, or Security product segments. The number two point represents expansion within each segment, which each contains at least three products. The third point signifies customers expanding across Elastic’s three product segments. For instance, an example of a third-point sale is an existing Search customer buying Elastic Security or Observability services.

Elastic Financial Analyst Day 2022 Investor Presentation

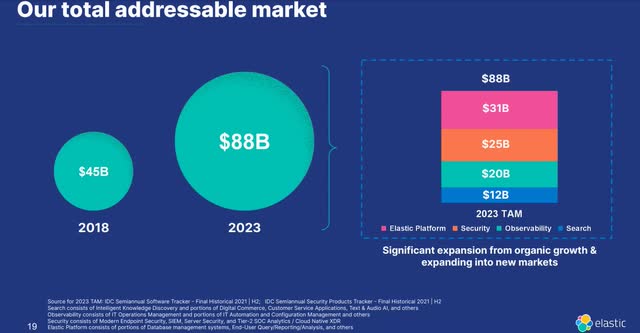

During Elastic’s 2022 Investor Day, the company cited International Data Corporation’s (“IDC”) statistics that show its Total Addressable Market (“TAM”) across the above three opportunities almost doubled from $45 billion in 2018, the year of its Initial Public Offering, to $88 billion in 2023.

Elastic Financial Analyst Day 2022 Investor Presentation

The best part is that IDC estimated $88 billion TAM before generative AI became the latest “next big thing.” Elastic’s TAM opportunity could grow faster and larger than expected if generative AI becomes as large as some prognosticators believe it could become. However, although some investors may hype up the opportunity in generative AI, it is essential to understand that generative AI is a long-term opportunity. The market will likely value the stock more in the near and medium term based on its performance in the Security and Observability opportunity, which currently make up $45 billion or slightly over half of its estimated 2023 TAM.

Its generative AI opportunity

One of the deficiencies that users of generative AI have found early on is its propensity to generate wrong answers or hallucinate. One of the better ways to reduce AI hallucinations is by using semantic, vector, and hybrid search techniques, which considerably improve the accuracy of generative AI responses. The reason that some investors are increasingly looking upon Elastic as an AI opportunity is that semantic, vector, and hybrid search techniques are right in its wheelhouse through its ESRE (Elasticsearch Relevance Engine), a collection of tools Elastic designed to allow AI-based applications to understand natural language data. Chief Executing Officer (“CEO”) Ashutosh Kulkarni said on the company’s recent second-quarter earnings call:

Generative AI is driving a resurgence of interest in search as customers use semantic search, vector search and hybrid search to ground large language models with their private business context and ESRE provides the most comprehensive and enterprise-ready platform for these use cases. While it will take some time for generative AI spend to become a significant driver of our revenue, we are very excited about the long-term opportunity.

Source: Elastic Second Quarter FY 2024 Earnings Call

What he means by “ground large language models (LLMs)” is making it more likely that an AI application bases its responses on facts and that the AI model’s training or inherent biases don’t produce false answers.

When he mentions a vector search, it refers to a technique for turning words into numbers and measuring the similarity between these mathematical data representations. This search method works excellently on unstructured data, which is data like pictures, videos, music, social media posts, email, or any other data that fails to fit into the neat columns and rows of a traditional database. The standard keyword searches that work well in conventional databases don’t work very well with unstructured data.

A semantic search is much different from a vector search. Instead of turning words into numbers, this technique uses Natural Language Processing to glean the meaning of various words and phrases. This type of search extends beyond the old-fashioned keyword search and attempts to understand the context and intent behind a user’s search. A hybrid search can use a combined vector, semantic, keyword, and other search methods to find an answer.

Without digging too far into the weeds explaining this technology, management believes it has the broadest capabilities to help generative AI models produce more correct responses than without its usage. CEO Kulkarni said the following about Elastic’s Search prospects to improve generative AI responses:

When search powers AI, customers are able to quickly build generative AI applications while reducing hallucinations at the lowest possible cost. Elastic’s prospects as a key component of the modern IT stack for generative AI remain extremely strong.

Source: Elastic Second Quarter FY 2024 Earnings Call.

Last, what the CEO says about generative AI taking time to drive Elastic’s revenue significantly will likely turn out to be true. Despite the hype surrounding the technology, market research company Gartner (IT) predicts that generative AI won’t have a material impact on IT revenue until 2025.

Suppose you are a patient long-term investor who believes that generative AI can become a disruptive technology and that Elastic’s search tools have considerable potential upside in AI. In that case, you might value the company differently than those who value it only on the near-term results they see and want to avoid speculating on the AI opportunity several years down the road.

The near-term results

Before OpenAI released ChatGPT and started the generative AI era, Elastic identified six growth drivers during its Financial Analyst’s Investor Day in 2022. The following image presentation shows those factors:

Elastic Financial Analyst Day 2022 Investor Presentation

What investors should look for in the company’s earnings releases, earnings calls, or investor conferences is data or language from management indicating Elastic’s “growth vectors” are healthy, as it augurs well for Elastic’s near and medium-term revenue growth momentum. And its second quarter FY 2024 earnings report gave investors in this company reasons to feel optimistic about its near-term growth.

Elastic Second Quarter FY 2024 Earnings Presentation

First, although the company only grew overall revenue by 17% over the previous year’s comparable quarter, investors were pleased to hear CEO Kulkarni talk about continued improvement in cloud consumption. One of the most significant issues cloud companies have faced from late 2022 into 2023 is a slowdown in customers consuming cloud resources. Even the big boys AWS, GCP, and Azure have seen slowing consumption trends and revenue growth decline. This time last year, Elastic management talked about customers doing a “belt-tightening” and decreasing cloud consumption among small and medium-sized businesses, which proved terrible for the company’s results. However, in the latest quarter, the commentary is much more positive. CEO Kulkarni said on the earnings call:

[A] trend in the quarter was around cloud consumption, where continued improvements helped drive cloud revenue growth. Customers remain focused on costs, but they have generally optimized their Elastic deployments and are now focused on driving new workloads to Elastic.

Source: Second Quarter FY 2024 Earnings Call

Growing cloud consumption and “driving new workloads” suggest increased usage of Elastic’s search and analytics tools, adoption of new solutions, and customers moving to higher subscription tiers. Elastic Cloud’s total revenue grew 31% year-on-year in the second quarter of FY2024, down from the previous year’s rise of 52% and 84% in the same quarter two years ago. Considering that a few other cloud companies’ commentaries in the third quarter have suggested that cloud optimization is not getting worse and some customers are starting to add new workloads, Elastic Cloud may be at or near the end of its steep quarterly year-over-year revenue growth decline since the end of 2021.

Another favorable trend for the company that the CEO highlighted was evidence that its go-to-market strategy of creating sales across its three product segments achieved some success in the second quarter, especially wins in the Observability and Security segments, which bodes well for the company in the near and medium term. The CEO said during the earnings call:

The second trend we saw in Q2 was customers continuing to consolidate onto the Elastic platform for multiple use cases. We had many key wins where we displaced incumbent solutions for observability and security and helped customers save on their overall IT spend while gaining even greater value through our many innovations.

Source: Elastic Second Quarter FY 2024 Earnings Call

Despite an uncertain economy and fierce competition in the observability and security market, Elastic managed to maintain solid customer growth. It ended its latest quarter with over 1,220 customers with an annual contract value (“ACV”) above $100,000 and over 4,230 customers above $10,000 in ACV. Total subscription customers were approximately 20,700, up from 20,500 in the first quarter. Most of its new customers use Elastic Cloud.

Elastic Second Quarter FY 2024 Earnings Presentation

Elastic Second Quarter FY 2024 Earnings Presentation.

Elastic recorded a 110% Net expansion rate (“NER”) by the end of October 2023 — a solid number. NER measures the year-over-year growth in ACV from its existing customers, including upsells and renewals. A 110% NER means existing customers are spending 10% more than they did in the previous year. The higher the NER, the better. In the company’s latest 10-Q, management states how critical this metric is for the company:

Our future [revenue] growth and profitability depend on our ability to drive additional sales to existing customers. Customers often expand the use of our software within their organizations by increasing the number of developers using our products, increasing the utilization of our products for a particular use case, and expanding use of our products to additional use cases. We focus some of our direct sales efforts on encouraging these types of expansion within our customer base. We believe that a useful indication of how our customer relationships have expanded over time is through our Net Expansion Rate, which is based upon trends in the rate at which customers increase their spend with us.

Source: Elastic December 01, 2023 10-Q

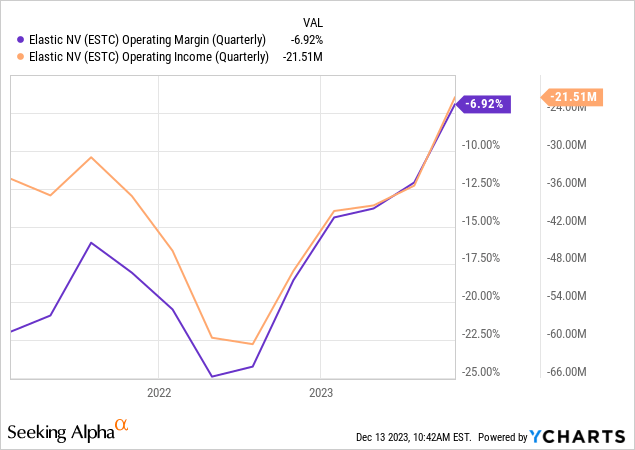

Next, let’s look at profitability trends. Like many other companies unprepared for the sharp reduction in global economic growth in the post-pandemic era, Elastic’s cost structure needed to be lowered compared to its potential revenue growth. On November 30, 2022, management announced during its second quarter FY 2023 earnings call that they would restructure the company to gain operating efficiency and reduce costs. Unfortunately, some of the costs were human, as the company announced it would also lay off 13% of its workforce — a blow to employee morale. However, around a year later, the company’s moves paid off in improved operating margins and reduced operating loss, as seen in the chart below.

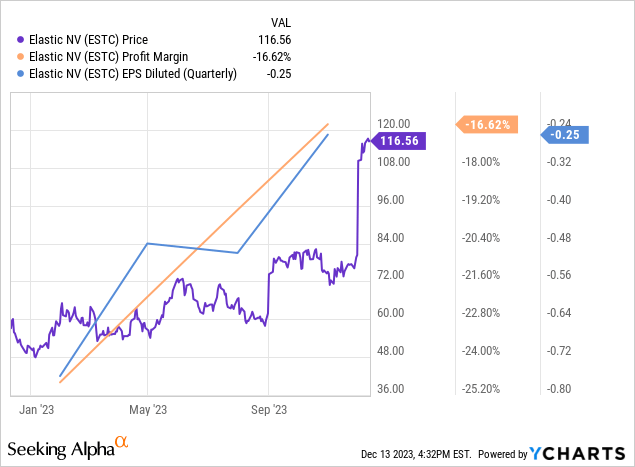

The global economic picture could remain muddled for the next year or two. Investors will likely continue emphasizing profitability over top-line growth in that case. So, monitoring Elastic’s bottom line for earnings growth is essential. Elastic produced a GAAP diluted earnings per share (“EPS”) loss of $0.25 in the second quarter and an adjusted free cash flow (“FCF”) of negative $3 million in the quarter with a negative 1% adjusted FCF margin.

The company maintains a strong balance sheet. At the end of the second quarter, the balance sheet showed cash and short-term investments of $966 million against $568 in long-term debt. Elastic has a debt-to-equity (D/E) ratio of 1.3. A D/E ratio between 1.0 and 2.0 typically signals a moderate risk balance sheet. It has a quick ratio of 1.89, indicating that the company can pay its short-term debt.

Risks

Inflation, rising interest rates, wars, the pandemic, and other macroeconomic issues have slowed worldwide economic activity over the last several years and have led to an uncertain economic environment. If economic conditions worsen, it may be more challenging for the company to close subscription sales, and cloud consumption could continue to slow, resulting in reduced revenue growth and the stock price underperforming.

Throughout its history, Elastic has not produced Generally Accepted Accounting Principles (GAAP) profitability. If the economy worsens, it may lose some of this year’s progress toward a breakeven point.

Last, Elastic faces tough competition in the Observability and Security market from companies like Splunk (SPLK), Datadog (DDOG), Sumo Logic (SUMO), Microsoft, and Amazon, to name a few. Heavy competition could force the company to spend more to maintain or gain market share, making it more difficult to achieve profitability.

Should you buy, sell, or hold?

The following shows a reverse discounted cash flow model with a trailing 12-month FCF of $67, a terminal growth rate of 3%, and a discount rate of 10%. On December 12, 2023, the closing price of $116.35 implies FCF growing at a rate of 37% over the next ten years to reach $1.6 billion, which is a highly aggressive assumption when Elastic has yet to generate profits. The market potentially overvalues the stock.

Elastic Reverse DCF

|

Third quarter FY 2024 reported Free Cash Flow TTM (Trailing 12 months in millions) |

$67 |

| Terminal growth rate | 3% |

| Discount Rate | 10% |

| Years 1 -10 growth rate | 37% |

| Current Stock Price (December 12, 2023, closing price) | $ 116.35 |

| Terminal FCF value | $1.607 billion |

Analysts estimate that non-GAAP EPS will grow from $1.13 in fiscal 2024 to $12.99, a compound annual growth rate of 31.17%. If I use the non-GAAP EPS growth rate of 31% as a proxy for FCF growth, I calculate an intrinsic stock value of $76.66.

MongoDB DCF

|

Third quarter FY 2024 reported Free Cash Flow TTM (Trailing 12 months in millions) |

$88.67 |

| Terminal growth rate | 3% |

| Discount Rate | 10% |

| Years 1 -10 growth rate | 31% |

| Current Stock price | $116.35 |

| Terminal FCF value | $1.027 billion |

| Intrinsic Value | $76.66 |

According to the above calculations, at $116.35, Elastic is 52% overvalued. Elastic might prove its current valuation over the long term because people underestimate its opportunity in generative AI. In the near term, however, the picture is not as rosy. Some economists and big banks expect global growth to slow in 2024. Additionally, while companies like Amazon and Microsoft have reported “cloud optimization” trends winding down, they have yet to predict an upturn in cloud spending. Cloud spending could bounce along a bottom for more than a few quarters.

Consequently, Elastic’s results in the near term might be disappointing, especially if the global economy tanks. If you have yet to buy the stock, avoid this name, as there may be better opportunities to buy. If you are a patient investor who already owns shares, the long-term potential upside in generative AI is reason enough to stick around. I recommend a Hold.

Read the full article here