")

After the bell on Wednesday, we received fiscal third quarter results from BlackBerry (NYSE:BB) for the company’s November ending period. Over the past decade, shares have been one of the worst performers in the market as a revenue turnaround has completely failed to materialize, and now more major changes are in the works. The latest set of results were less than impressive yet again, clouding the overall future here a bit more.

For fiscal Q3, BlackBerry reported revenues of $175 million. This number was up $6 million year-over-year and soared dramatically on a sequential basis from the more than a decade low of $132 million that was reported in Q2. Unfortunately, the total top line number missed street estimates by nearly $6 million. For once, the Cybersecurity segment showed a nice number, with revenues rising by $8 million over the prior year period to $114 million. The IoT business continued its longer term growth trend by adding $4 million to $55 million. Some of these gains were offset by the Licensing segment, which can be very volatile quarter to quarter, and this time showed a 50% year-over-year drop to $6 million in revenue.

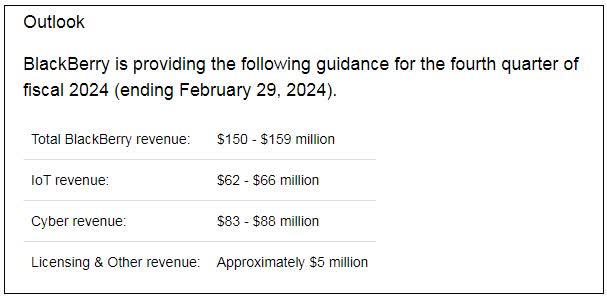

In the press release, BlackBerry management talked about the Cybersecurity division securing large strategic deals with leading government agencies. However, the company also reported that the annual recurring revenue (“ARR”) figure of this segment dipped by another $6 million sequentially to $273 million. The total ARR here is down $61 million in the past 18 months, and yet again management is saying it should bottom soon, with growth not too far away. The dollar-based net retention rate here at 82% remains well below what’s needed for sustainable growth. Worse yet was the company’s revenue guidance for the current period, its fiscal Q4, which concludes at the end of February 2024. Analysts were looking for nearly $190 million, which would have been a nice sequential jump to finish out the fiscal year, but BlackBerry is now calling for a large sequential decline:

Q4 Guidance (BlackBerry Q3 Earnings Release)

On the margin side, the nice increase in both Cybersecurity and IoT revenues helped gross margin dollars rise to their highest point in a couple of years (excluding the patent sale quarter). However, it’s not yet enough to cover all of the company’s major operating expenses, so there are still GAAP losses being reported here. The company’s adjusted profit of a penny beat the street by 3 cents. However, BlackBerry basically never misses here, as it always reports a number of adjustments to make the bottom line look much better – in this quarter those alterations were about a nickel per share in total.

A major worry of investors is that the company doesn’t have the financial flexibility to execute a true turnaround plan. Total cash and investments were $271 million at the end of Q3, down from $519 million at the end of Q2. During the period, the company’s convertible debentures hit their maturity date, but the stock’s low price meant they couldn’t be swapped for equity. Management ended up paying the $365 million back, but at the same time issued new extension debentures in the amount of $150 million. These will mature in February 2024, but could be extended for an additional three months. BlackBerry needs to get its cash burn down, which in Q3 was significantly hampered by a surge in accounts receivable that put that balance sheet category figure at a value higher than the quarter’s revenue total.

Since I last reported on the company in October, there have been two other major developments. First, John Chen retired from his CEO position after a very turbulent decade at the helm. While Chen was hired to help BlackBerry avoid bankruptcy, he failed to get the long term revenue picture back on track. So while markets have soared to new all-time highs in the past ten years, BlackBerry shares lost a good chunk of their value. Ironically, John Giamatteo, President of BlackBerry’s Cybersecurity division, was appointed as the new CEO, despite that segment being the company’s worst revenue performer in recent years.

The second major news item is that the plan to IPO the IoT segment has been scrapped. On the conference call, management explained its new plans, whereas it will have two separate business segments basically under a holding company. There will be some additional restructurings over the next calendar year, which will cut the operating expense base down a bit. This could be a decent catalyst if the company can get to GAAP profitability and positive free cash flow, but we all know that BlackBerry has had plenty of trouble meeting its goals over the past decade.

As of Wednesday’s close, shares were trading at about 3.25 times their expected revenue for the February 2025 fiscal year. That’s significantly below most comparable software companies that go for high single digit or low double digits on a price to sales basis. However, many of those names have very strong revenue growth profiles, and some even have sizable GAAP profits and or significant free cash flow generation. While I’m not thrilled about BlackBerry’s revenue situation currently, that negativity is offset by the potential for profitability improvement coming in the next year along with the depressed valuation. For that reason, I’m keeping a hold rating on the stock, but I will examine that more in about three months as management has said to wait until the next earnings call for more concrete numbers and plans for the separation and restructuring efforts.

In the end, it was another disappointing quarterly report from BlackBerry. While the company announced its usual bottom line beat for adjusted Q3 earnings, revenues again missed estimates by a decent margin and Q4 revenue guidance was well below street expectations. The company still has a sales problem, but a new CEO is in place so I’ll give him some time to get his near term plans finalized before I can determine if this stock should get a buy or sell recommendation again. One thing is certain, and that is that BlackBerry has been one of the most disappointing names in recent years, with shares very close to multi-year lows at a time when the overall market has been racing to new highs.

Read the full article here