")

Investors who ignored the market pessimism in ASML Holding N.V. (NASDAQ:ASML) at the previous steep pullback leading to a bottom in September/October 2023 have been rewarded. Accordingly, ASML bottomed out at the $560 level in early October after falling into a bear market, as it fell almost 27% from its July 2023 highs. It also coincided with geopolitical uncertainties relating to more intense US export controls. The uncertainties were worsened by Canon’s (OTCPK:CAJPY) challenge to gain market share in the advanced semiconductor equipment market, as the Japanese semiconductor company threatened to thwart ASML’s EUV monopoly.

I explained in my previous update in mid-October (pre-Q3 earnings) why investors “shouldn’t be spooked by the recent fears hurting ASML’s market dominance.” As a result, astute investors who gleaned a bottoming opportunity in ASML capitalized on these fears and rode the recovery as ASML nearly re-tested its July highs. As a result, it should be clear why choosing your entry points makes sense for high-multiple stocks like ASML, helping investors markedly improve their risk/reward and outperform the market. If you added ASML aggressively at its July highs, you are likely still sitting on losses, barely even breaking even. However, if you added ASML at its October lows, you would have gained up to 35% on a price-performance basis in just over two months.

ASML reported its third-quarter earnings release in October (over two months old). I’ve always believed that investors shouldn’t rely on past earnings releases (backward-looking information) to make investing decisions in a forward-looking market. If you closely followed ASML’s initial Q3 post-earnings reaction, you would have realized that the market astutely shook out weak holders at its October lows before setting up the surging rally to form its December highs.

Management updated in its earnings call that while the company’s outlook suggests a relatively flat 2024, there could be a growth inflection in 2025. As a result, ASML remains confident in reaching a target revenue range of between €30B and €40B for a midpoint guidance of €35B by FY25. Wall Street analysts are still relatively pessimistic, projecting revenue estimates of about €33.2B in FY25, lowering the bar for ASML to potentially outperform.

I can understand why analysts are cautious about ASML’s growth inflection, as the execution risks leading to a flat growth guidance for 2024 need to be accounted for. ASML has a solid backlog, reaching €35B in Q3, including €19B for EUV lithography systems. The EUV backlog includes high-NA orders, which could lift its gross margins higher at scale. Despite the clarity of its backlog, Wall Street analysts are likely concerned about whether it could translate into revenue recognition, as ASML highlighted the uncertainty of the underlying demand recovery in 2024.

However, ASML’s significant rally since bottoming out in October demonstrates the market’s conviction that ASML’s leadership isn’t expected to be impacted. Advanced Micro Devices’ (AMD) recent AI chips launch highlighted that the company underestimated the scale of the AI chips market initially. Accordingly, AMD revised the total addressable market to be worth $400B by 2027, up from a TAM of just $150B at its previous update.

Furthermore, even Canon highlighted that the company doesn’t expect its machines to “replace ASML’s EUV machines,” corroborating ASML’s dominance. While Canon’s machines could be more “cost-effective” than ASML’s machines, it remains to be seen whether leading foundries like TSMC (TSM) would be willing to take significant risks with Canon’s technology. Accordingly, nano-imprint technology has reportedly faced technical issues, “including issues related to particles in the air, alignment problems affecting yields, and concerns about throughput.” As a result, I believe the market has astutely shrugged off these undue concerns, as investors remain confident about ASML’s leadership.

Notwithstanding the recent market optimism, I believe it makes sense to be cautious now, as its valuation and price action suggest much of its near- and medium-term upside seems reflected.

ASML last traded at a forward EBITDA multiple of 29.2x, well above its 10Y average of 22.3x. It’s also way ahead of its peers’ median of 18.7x. Seeking Alpha’s “F” valuation grade adds another layer of caution, urging investors to carefully assess their decisions to add exposure to ASML at the current levels.

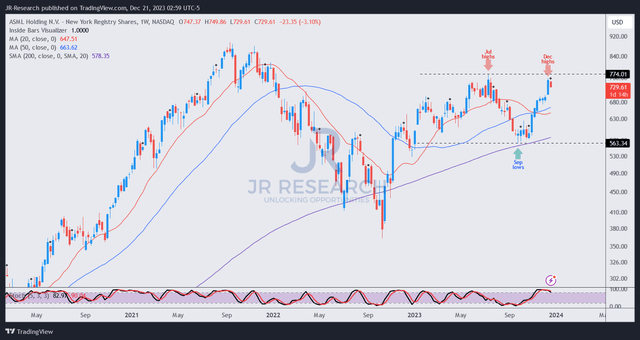

ASML price chart (weekly) (TradingView)

ASML’s recent surge looks to have faced resistance just below the $775 level that marked its July 2023 high. I didn’t assess sell signals suggesting investors should consider cutting exposure significantly.

Despite that, the remarkable rally isn’t expected to be sustained without a welcomed pullback, corroborated by its relatively expensive valuation that could deter dip buyers from adding further.

As a result, I encourage investors to wait patiently for much-needed downside volatility to shake out some recent fervor on semi-equipment stocks before considering a return to add more shares.

Rating: Downgraded to Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here