")

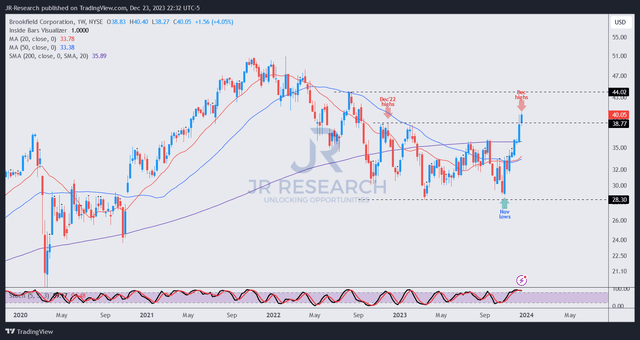

Investors in leading global wealth manager Brookfield Corporation (NYSE:BN) have experienced a surging recovery since BN bottomed out in early November 2023. Accordingly, BN rallied more than 40% from those levels, as it re-tested levels last seen in September 2022. As a result, it has also normalized its 5Y total return CAGR of 16.5%, ahead of its 10Y average of 13.5%.

Therefore, astute investors who positioned themselves well for the recovery ahead of the FOMC conference in mid-December have outperformed the S&P 500 (SPX) (SPY) substantially. Management had already provided sufficient clues to investors looking to partake in the BN opportunity at its third quarter or FQ3 earnings release. Accordingly, Brookfield underscored that it assessed “a significant disconnect between the intrinsic value of its shares and their trading price” in early November. In addition, it encouraged investors to add exposure by highlighting “that current entry points for investors could lead to favorable returns.”

Consequently, I believe management’s confidence in its robust and well-diversified business model has been vindicated, given the sharp relative outperformance since early November. Brookfield investors are likely well aware of the attractive investment thesis in BN. The corporation has significant exposure to Brookfield Asset Management’s (BAM) alternative asset management business, driving high-quality fee-related earnings. Accordingly, BAM contributed about 68% to BN’s asset management distributable earnings or DE in Q3. It also accounted for over 37% of Brookfield Corporation’s overall DE, suggesting it’s a critical growth driver.

Despite that, BN’s well-diversified business model provides investors exposure to its operating businesses, including infrastructure and renewable assets. As a result, investors can gain exposure directly to Brookfield’s solid cash-flow-generating assets portfolio. These assets are structured with non-recourse asset-level debt, enhancing its appeal. In addition, BN also received a credit rating upgrade in late November 2023. Notably, the upgrade was predicated on the “resilience and quality of earnings and cash flows generated by the company’s underlying operations.”

In addition, the company has also refinanced its near-term debt maturities for 2024/25. Accordingly, the company executed a $700M senior notes offering recently. Consequently, Brookfield anticipates the offering to “address upcoming maturities in 2024, leaving only modest maturities remaining through the end of 2025.” Accordingly, BN reported (in Q3) about $568M and $500M in term debt due in 2024 and 2025, respectively. As a result, the company capitalized on its recent credit rating upgrade to refinance its near-term debt maturity to improve the resilience of its balance sheet.

In addition, Brookfield investors also benefit from the growth in its insurance solutions business, which was instrumental in its Q3 performance. The segment delivered a portfolio yield of 5.5%, outperforming its average cost of capital by 200 basis points. DE attributed to the insurance solutions segment reached $182M, posting a 14.4% YoY growth. Management is confident of driving further upside from this segment, anticipating annualized earnings “reaching $800 million by the end of the year.”

BN investors have exposure to critical business segments and capitalize on the secular themes of “decarbonization, digitalization, and deglobalization.” Bolstered by Brookfield’s massive scale and operating expertise, investors can rely on the corporation’s competitive advantage and compound their wealth through these focused areas.

BN price chart (weekly) (TradingView)

As a result, I’m not surprised with the revival in BN since its November 2023 bottom. It recovered all the losses from its December 2022 highs in just eight weeks.

I believe the market has astutely pounced on a high-quality asset manager who is well-primed to leverage its scale and expertise across several secular themes moving ahead.

As a result, investors who missed buying into its highly attractive risk/reward opportunity will not likely see those levels revisited in the near term as the Fed moves toward a more dovish phase.

I gleaned that the recent surge has likely captured most of its near-term upside. Therefore, I welcome a healthy pullback to help improve subsequent entry levels for investors to potentially outperform the market.

I will watch the low- to mid-$30s level as possible zones for constructive consolidation, allowing investors who missed buying its recent lows another opportunity to get on board.

Rating: Initiate Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here