Co-authored with “Hidden Opportunities.”

Value investing involves buying underappreciated businesses when others are selling them at a discount and then holding them for the long term. This approach led to some of Warren Buffett’s most significant and profitable investments, acquired when others panicked.

During the 2008 financial crisis, when everyone was running away from the stock market, the legendary investor bought Bank of America (BAC) and Goldman Sachs (GS) shares, which became excellent passive income sources for years.

“In the 58 years we’ve been running Berkshire, I would say there’s been a great increase in the number of people doing dumb things, and they do big dumb things,” he said. The reason they do it is because, to some extent, they can get money from people so much easier than when we started.” – Warren Buffett.

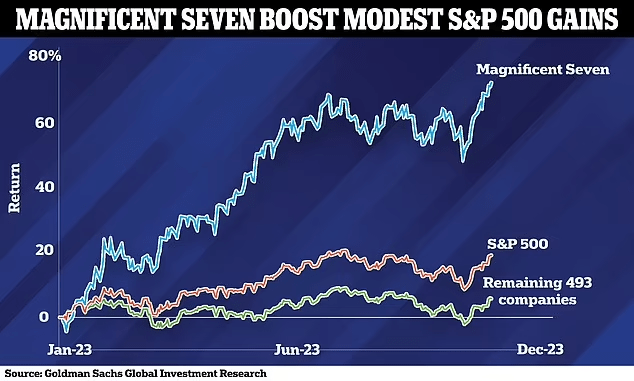

The markets may have recovered, but it is the tale of two markets with a handful of companies swelling up in valuation. The rest of the index without The Magnificent Seven continues to present undervalued bargains to scoop up. Source.

DailyMail

We discuss two such beaten-down and ignored picks that we buy as the Magnificent Seven distract the markets. Let’s dive in!

Pick #1: BTI – Yield 9.7%

In 2011, Google (GOOG)(GOOGL) paid $12.5 billion to acquire Motorola Mobility. Three years later, the company sold much of it to Lenovo for $2.9 billion, realizing a $9.5 billion loss. It is likely that Google overpaid for the assets, but the company retained a plethora of mobile patents that it licensed to Lenovo and continued generating cash flows. Moreover, several of those acquired patents were instrumental for the company in launching its Pixel brand of smartphones.

In the same vein of discussion, in 2005, Google acquired the rather unknown Android for $50 million. Today, this platform has 72% of the market share and generates hundreds of billions in revenue from licensing and sales on the Google Play Store. But all that success will not be reflected on the conglomerate’s book value, since accounting principles generally require the acquiring company to account for the acquisition using the purchase method, where the assets and liabilities are recorded at their fair values at the acquisition date.

In the above examples, Google’s write-down of the Motorola asset acquisition or the lack of adjustment of the book value of its Android acquisition didn’t impair the monetization potential of these businesses.

Let us now talk about British American Tobacco p.l.c. (BTI, BTAFF), popularly known as BAT, which is currently in the news for the announcement of a £25 billion impairment charge relating to its U.S. brands, which it acquired via RJ Reynolds in 2017.

Brands don’t carry indefinite value, and the write-down of the book value of the acquisition is a realistic alignment of value that BAT would get if it were to sell these assets (not that they are planning at this time). In fact, the Oracle of Omaha has repeatedly mentioned that book value isn’t a meaningful measure of a company’s value.

The really wonderful businesses require no book value. It’s a factor we ignore. We do look at what a company is able to earn on invested assets and what it can earn on incremental invested assets. But the book value, we do not give a thought to. – Warren Buffett in 2000.

The economic value of an income-generating asset like a brand can sometimes be more closely tied to its ability to generate cash flow rather than its market value, and book value adjustments may not always align perfectly with the ongoing operational performance of the asset.

Combustible tobacco is a business that requires no new investment. The global customer base is massive, and the demand remains strong, although on a mild declining trend due to health concerns and social stigma. BAT subsidiary Reynolds American is the second-biggest U.S. cigarette maker by sales and has continued to demonstrate stubborn demand despite massive price hikes and taxation. We expect this profitability and cash flow potential to continue for the foreseeable future until BAT has a dominant non-combustible business.

There is a significant benefit from this impairment

As discussed before, the impairment is largely on paper and does not mean BAT is disposing of these assets at pennies on the dollar. These brands will continue churning FCF (Free Cash Flow) for the foreseeable future.

There is one notable benefit from the impairment in that it is often tax deductible. In its financial reports from FY 2022, BAT reported a 29% stake in ITC, which had a book value of £1.9 billion but was worth more than £12 billion from a fair value perspective. Through 2023, this stake has appreciated to over £16 billion. If BAT were to realize the capital gains from this investment, it could offset all those gains through the impairment.

And if BAT pursues the disposition of its ITC stake, the proceeds will be substantial enough to extinguish ~50% of the company’s net debt. Source.

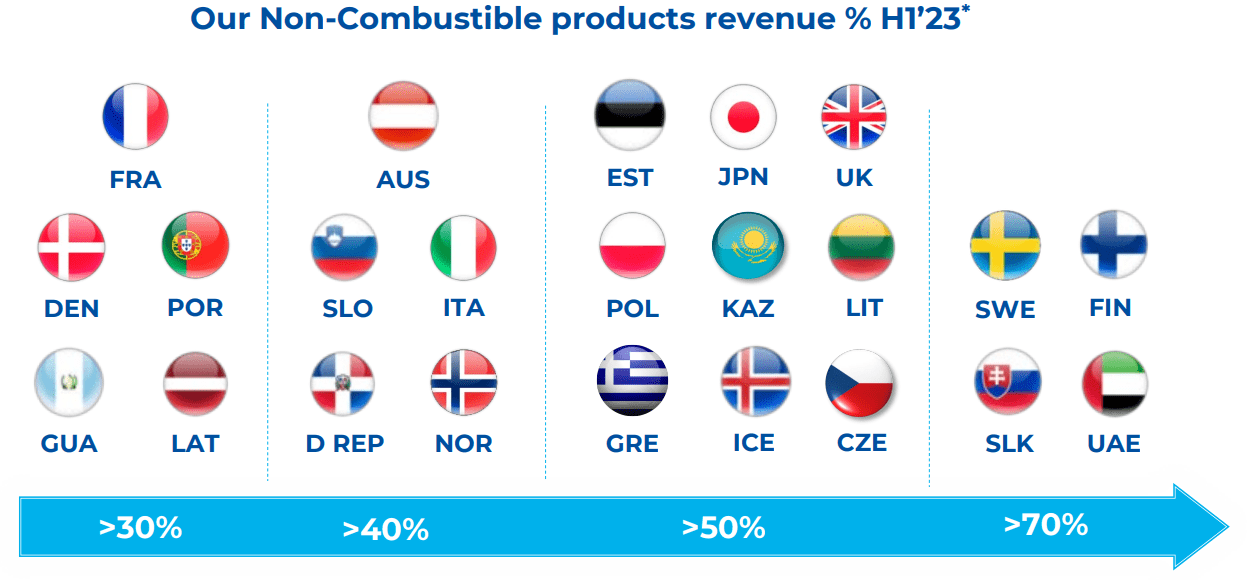

FY 2023 guidance remains intact

1H 2023 Investor Presentation

Non-combustibles represent a rapidly growing portion of BAT’s business globally, and the company’s exposure to emerging economies like Bangladesh, Pakistan, and Indonesia, will ensure modest growth even in its combustible segment. Mr. Market is being irrational, looking at BAT solely through the U.S. market. In fact, the U.S. government recently announced its decision to delay the menthol ban in fear of the political consequences of the decision ahead of the federal elections.

In this recent press release, management reaffirmed their FY 2023 guidance, expecting revenues to be at the low end of the 3-5% growth projection, a mid-single-digit adjusted EPS growth, and strong new category top-line growth, and expects this to contribute to 50% of the top line by 2035.

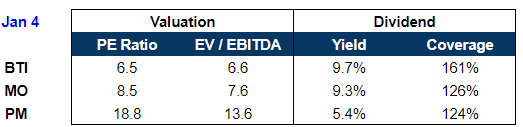

BAT currently trades at an extremely low valuation on forward earnings while sporting a large 9.7% yield. Among tobacco peers, BAT maintains the lowest 62% dividend payout ratio, indicating adequate safety to the income stream and strong prospects for continued dividend growth in the coming years.

Author’s Calculations

Accounting regulations require companies to carry out regular impairment tests, and BAT’s current announcement presents significant tax offsets without any change to the cash flow generation from its legacy brands or affecting the dividend safety. We know the combustible business will slowly fade away in developed nations, but that remains several decades away and adequate to fund the growth and expansion of non-combustibles. The steep irrational sell-off presents an attractive opportunity to load up on this 9.7% yield.

Pick #2: RVT – Yield 7.5%*

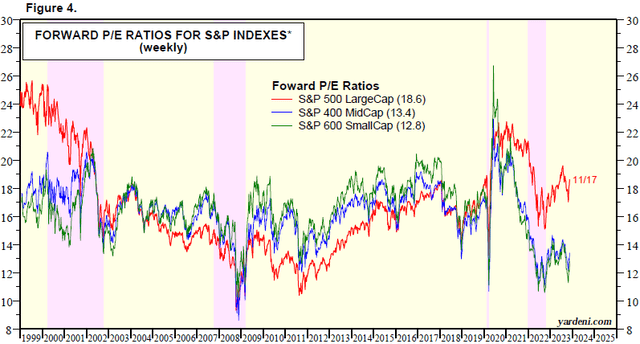

Due to the record pace of rate hikes by the Federal Reserve, and persistent recession forecasts by Wall Street, we see the widest disconnect between the valuations of Small Cap vs. Large Cap. Source.

Yardeni Research

Small caps are currently trading at valuations well below their historic levels, appearing to be priced as though the recession were already here.

Bargain buyers see a lot of value in the SmallCap sector, but as income investors, we want to collect waiting fees for that valuation improvement, whether it is from rate cuts or better earnings announcements from SmallCap firms.

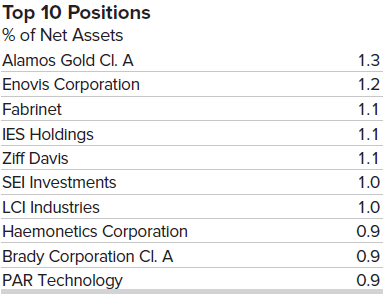

Royce Value Trust (RVT) is a time-tested closed-end fund, or CEF, run by managers who pay scrupulous attention to small-company balance sheets. As such, there is better protection against individual company blowups. 60% of the fund’s assets are invested across industrials, financials, and information technology, with an actively managed portfolio of 488 holdings from the small-cap segment of the market. Notably, the CEF’s weighted average P/E ratio sits at 14.4x, below that of its benchmark, the Russell 2000 index. Source.

RVT Fact Sheet

RVT was born in 1986, an era with high inflation, unemployment, and a weak economic outlook, making it one of the few funds that have demonstrated long-term portfolio reliance and shareholder returns through a wide range of economic challenges.

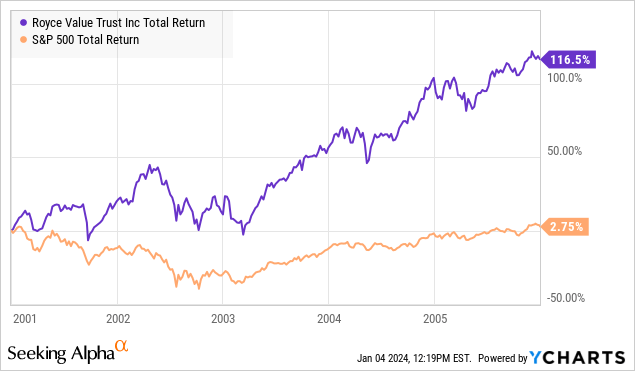

The parameters surrounding the economy today, namely unemployment, inflation, and interest rates, are highly comparable to those of the Dot-com bubble era. Comparing the performance of RVT and the S&P 500 since January 2001, we can clearly see what the CEF is made of, and the fund is well-positioned to repeat this in the coming years.

*RVT has a variable distribution policy whereby its quarterly payment is adjusted based on the NAV at the end of the trailing four quarters. Variable dividends scare a lot of investors, but the variability is a defense mechanism to protect the fund from having to liquidate valuable assets at unfavorable market prices. RVT does not utilize leverage in its investment strategy, which further protects the fund from further downside from a weakening economy.

In the nine months of FY 2023, RVT’s distributions were composed of 0.5% income, 15.3% short-term gains, 84.2% long-term gains, and 0% ROC.

Not only is RVT composed of undervalued companies from an undervalued sector, but the fund itself trades at a large 12% discount to NAV. This makes every invested dollar automatically work harder to secure returns.

RVT’s time-tested strategy makes it an excellent addition to your income portfolio, and the generational disconnect in SmallCap valuations makes it very appealing to lock in the 7.5% yield.

Conclusion

We all love a bargain in almost every purchase, be it goods or services. But when it comes to investing, people find it surprisingly comfortable to buy at 52-week high price points. It is like going to a bar during happy hour and waiting for it to end before you order your drink at regular prices. It doesn’t make any sense, but this is how the markets operate, and those who understand it repeatedly benefit.

“Some people should not own stocks at all because they just get too upset with price fluctuations. If you’re gonna do dumb things because your stock goes down, you shouldn’t own a stock at all.” – Warren Buffett.

The markets clearly show a disconnected recovery where the bulk of it remains undervalued with respect to its underlying earnings. BTI and RVT present two such deeply discounted picks that we are buying to collect steady dividends through the market’s irrational phase.

At High Dividend Opportunities, we have been steady buyers of passive income, and our “model portfolio” of +45 picks currently yields ~9.7%. They provide a reliable income stream as we patiently await market normalization during this unbalanced recovery. Our strategy involves seizing opportunities when others are fearfully selling, and with the impending shift in the rate cycle, the stock market’s “happy hour” is drawing to a close. Take swift action and capitalize on these bargains before they vanish!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here