")

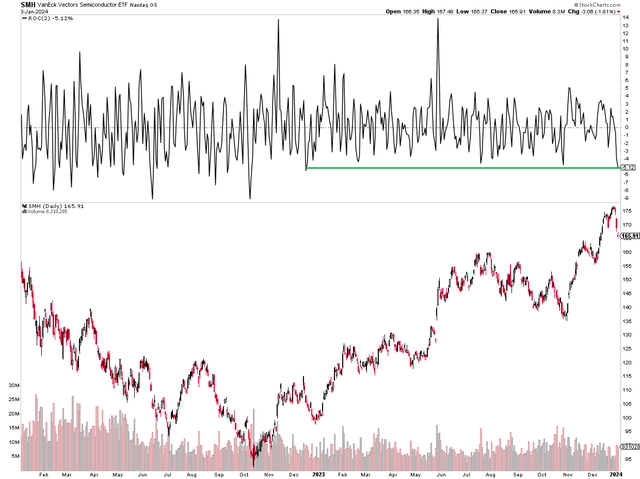

It has been a rough start for some of 2023’s winners. Specifically, semiconductor stocks have struggled to kick-start the year. I noticed that the first two sessions of January were the worst back-to-back trading days since December 2022 for the VanEck Semiconductor ETF (SMH). After a stellar last 12 months, a pullback might make sense, but I continue to see fundamental upside in one global chip player.

I reiterate my buy rating on Qualcomm (NASDAQ:QCOM). Following another quarterly EPS beat with robust earnings growth ahead, I see the stock as undervalued with technical strength.

SMH Chips ETF Suffers A Significant Dip To Begin 2024: worst back-to-back sessions since December 2022 -5.1%

Stockcharts.com

According to Bank of America Global Research, Qualcomm designs, develops, and supplies semiconductors and collects royalties on wireless handheld devices and infrastructure based on its dominant position in code-division multiple access (CDMA) and other related technology patents. In addition, Qualcomm provides systems software and components to wireless handset vendors and promotes applications and services that run on high-speed wireless networks. The company operates primarily through two segments: CDMA Technologies and Technology Licensing.

The San Diego-based $153 billion market cap Semiconductors industry company within the Information Technology sector trades at a low 14.9 forward 12-month non-GAAP price-to-earnings ratio and pays an above-market 2.3% dividend yield. Ahead of its Q1 2024 earnings report due out later this month, the stock features a moderate 29% implied volatility percentage and has a low 1.4% short interest as of January 3, 2024.

Back in November, Qualcomm reported a strong set of Q4 results. Non-GAAP EPS of $2.02 topped the Wall Street consensus outlook of $1.91 while $8.7 billion of revenue, down 24% from year-ago levels, was a small beat. Rapid growth in Android handset demand helped the chip stock along with costs that were generally in check during the quarter. That combination led to a healthy 31% operating margin. The management team also expects Q1 shipments from major Chinese handset manufacturers to verify at a 35% sequential growth rate. Another potential driver of future earnings is its chips being used in the next Samsung phone edition.

With full-year 2024 growth in handset shipments around 10% and perhaps strong bottom-line growth in the outer year, I continue to like the fundamental backdrop for QCOM. Don’t discount the strength in the auto market either – its Q4 revealed a high 23% sequential growth rate in that segment, though its IoT segment was lackluster. In terms of Q1 2024 guidance, revenues are seen in the $9.1 billion to $9.9 billion range with non-GAAP diluted EPS from $2.25 to $2.45. That’s an upbeat outlook amid a backdrop of a new iPhone launch and expected demand from China.

Key risks emerging for QCOM right now include macro weakness in China and the possibility of ongoing tensions between Apple and Huawei. Weaker global smartphone adoption amid a slowing economy could also hurt the firm, while margin pressure in that scenario would be likely. Also, QCOM’s penetration into the 5G competitive market has been impressive, but it may create a lofty expectations bar going forward, so say analysts at Morgan Stanley.

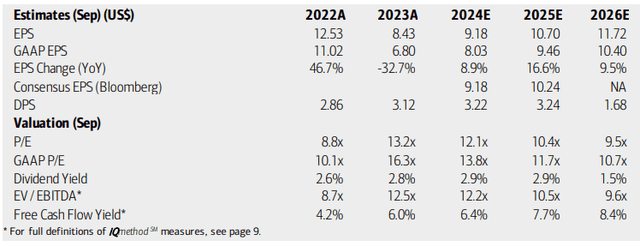

On valuation, analysts at BofA see earnings rising at a solid 9% clip this year, with an acceleration in per-share profits in 2025. A continued double-digit bottom-line growth rate is seen in 2026. The current consensus, per Seeking Alpha, shows operating EPS topping $10 next year and climbing above $11 in 2026, all while revenue growth is in the 5% to 9% range.

Dividends, meanwhile, are expected to rise at a steady pace over the coming quarters. QCOM continues to be a strong free cash flow generator – the current TTM FCF yield is 6.4%. The company also features an EV/EBITDA ratio that is below that of the S&P 500.

Qualcomm: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

If we assume $9.50 of forward non-GAAP EPS and apply a 17 forward operating earnings multiple, then the stock should trade near $162. That is up from my previous valuation estimate, given lower interest rates today and a natural rise in expected EPS over the coming 12 months. I continue to like Qualcomm’s cash flow metrics, though shares are not as attractive when assessing sales multiples.

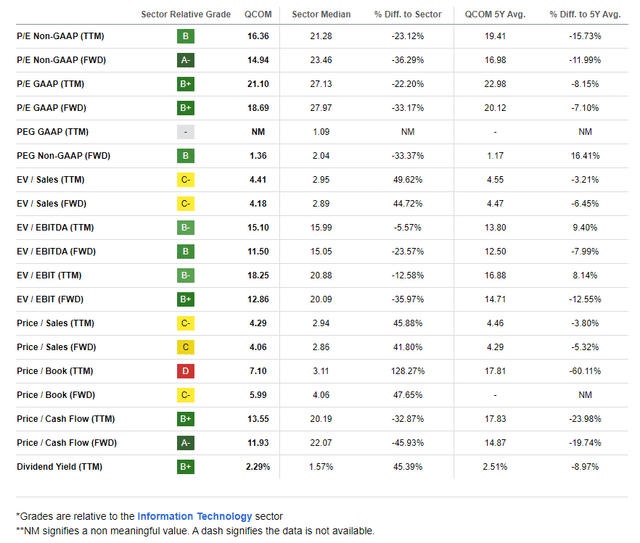

QCOM: Generally Favorable Valuation Metrics

Seeking Alpha

Compared to its peers, QCOM features a near-average valuation as the entire space experiences generally healthy chip demand. Historical growth has been weak, leading to the poor grade (non-GAAP EPS fell 33% in 2023), but I assert that the growth trajectory is much more sanguine. Qualcomm is among the most profitable and strongest firms from a free cash flow perspective, while share-price momentum has been strong – I will detail key price points to watch on the chart later in the article. Finally, EPS revisions have been mixed lately, though QCOM has topped earnings estimates in each of the last 12 reports.

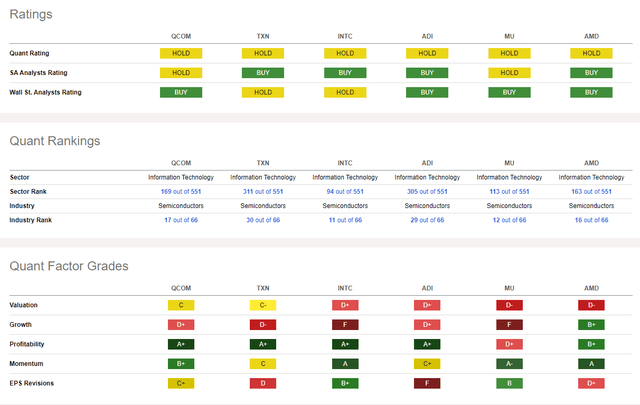

Competitor Analysis

Seeking Alpha

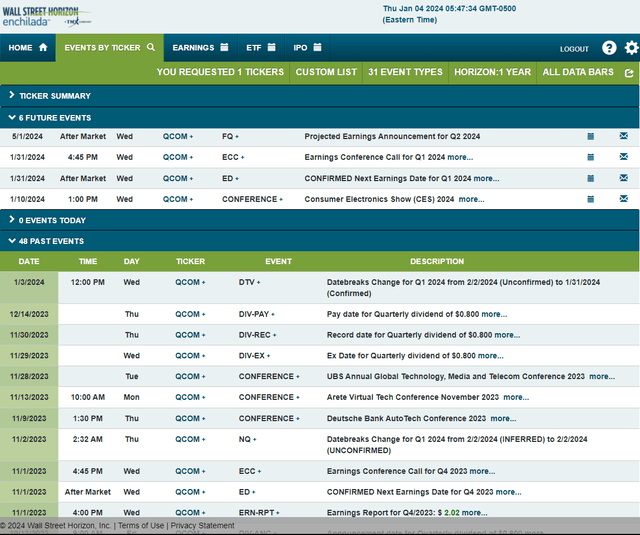

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q1 2024 earnings date of Wednesday, January 31 AMC with an earnings call immediately after results cross the wires. You can listen live here. Before that, Qualcomm is slated to participate at the

Consumer Electronics Show (CES) 2024 from January 9 through 12 in Las Vegas.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

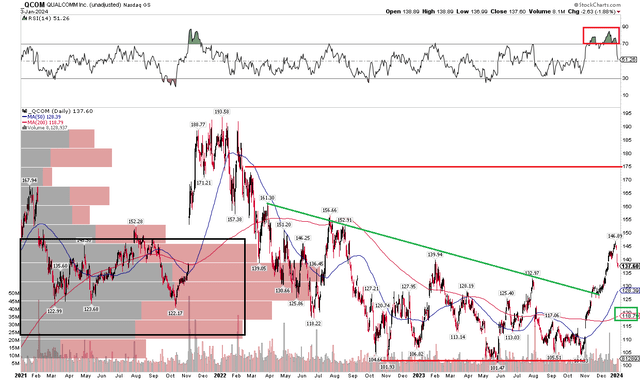

I took a long-term view of QCOM in my previous analysis in Q3 last year. Zooming in, I see that the stock has broken out from a consolidation that featured a key downtrend resistance line. Notice in the chart below that shares rallied above the $130 mark during Q4 last year. The stock has retreated amid the early-year selloff in the tech sector, falling from $147 to $138, but with a long-term 200-day moving average that is now upward-sloping, the trend appears to favor the bulls.

I continue to see broad support near the $101 mark, and the descending triangle breakout leads to an upside measured move price objective to near $175 based on the height of the triangle at its onset and then adding that height to the $130 breakout point. $175 also has confluence with the range lows from the late 2021 to early 2022 highs. For now, QCOM is working off technical overbought conditions, so buying on a pullback to the $130 breakout point could be a favorable risk/reward play.

Overall, I see QCOM’s chart as constructive after holding important support near $101 and then rallying through resistance.

QCOM: Bullish Upside Breakout, $175 Technical Target

Stockcharts.com

The Bottom Line

I reiterate my buy rating on QCOM. I see shares as a solid GARP play with impressive EPS growth ahead and a solid technical backdrop.

Read the full article here