")

Bureau of Labor Statistics

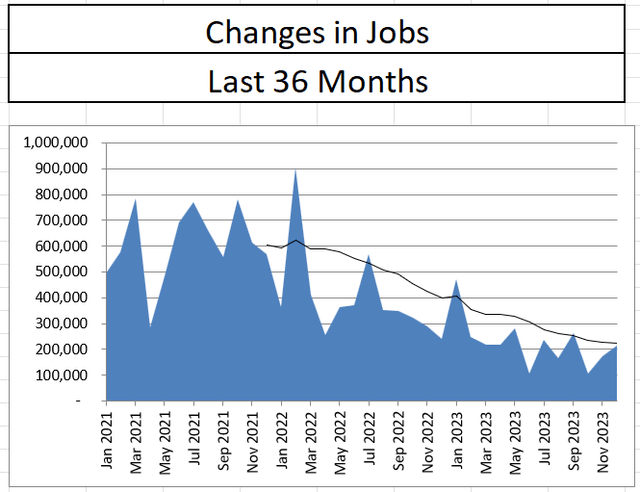

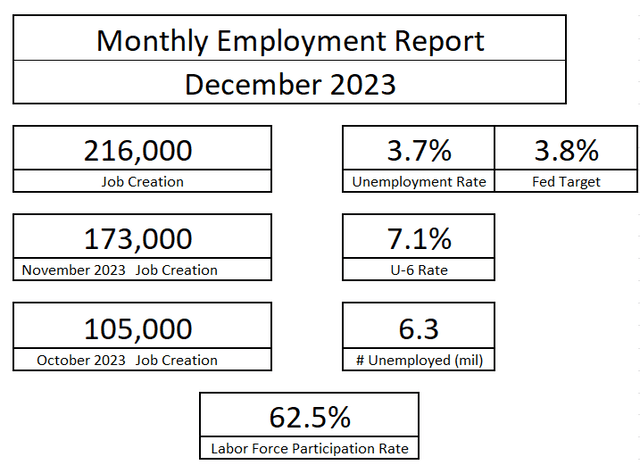

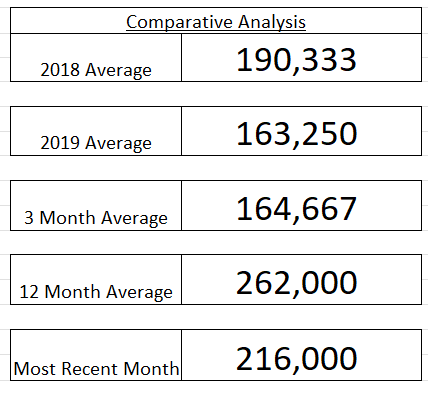

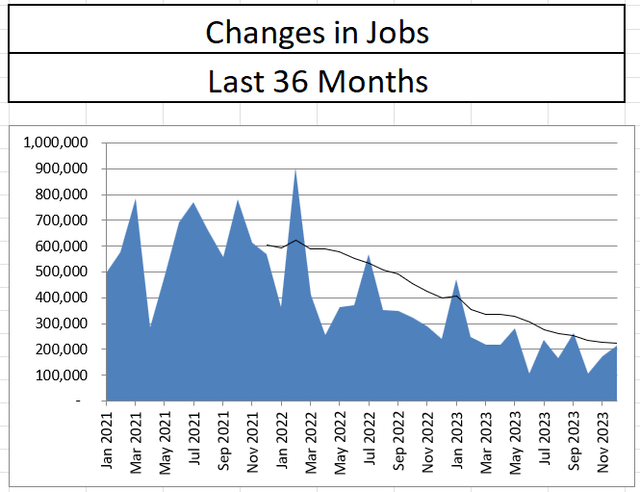

The Bureau of Labor Statistics released the December 2023 jobs report on Friday. While the report delivered on softness by revising October and November’s jobs numbers downward, the BLS estimated that the economy created 216,000 jobs in December, which was above expectations and pre-pandemic levels. Additionally, the unemployment rate remained at 3.7%, one-tenth below the Federal Reserve’s last projection for the year. While the Fed has projected easing rates, the status of the labor market raises serious questions about whether such an action may create new constraints.

Bureau of Labor Statistics Bureau of Labor Statistics

Bureau of Labor Statistics

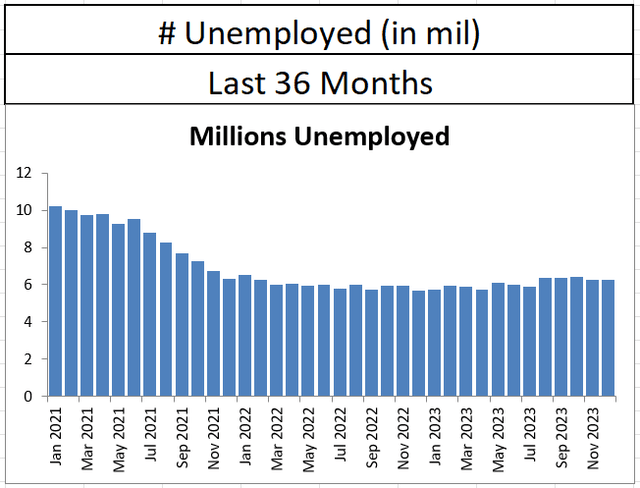

In dissecting the report, there continues to be a string of mixed messages in the data suggesting more of a normalization into a traditional strong labor market versus one that was overheating. The total number of unemployed people in December came in at 6.27 million, a slight uptick from the prior month and exactly at the six-month average.

Bureau of Labor Statistics

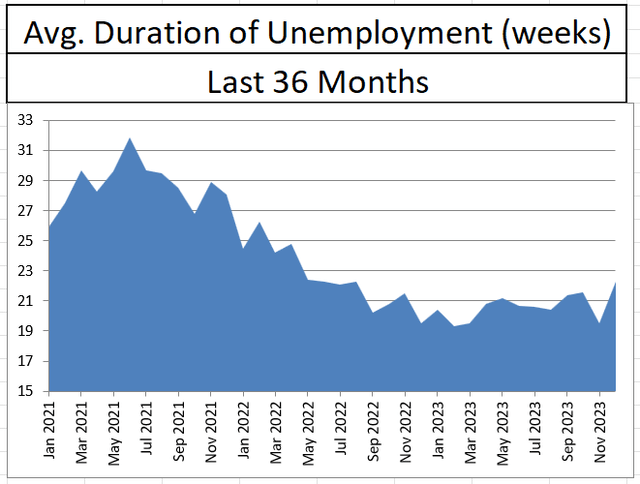

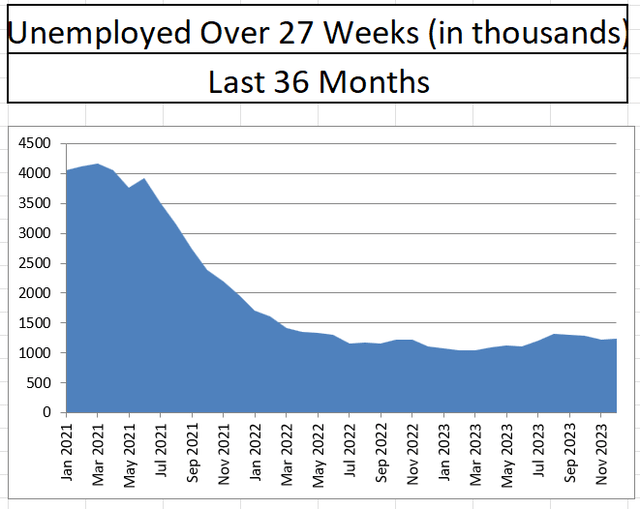

While the number of unemployed remained the same, the average duration of those unemployed popped back up after having a steep decline in November. The average duration of unemployment rose from 19.5 to 22.3 weeks. In fact, that level of duration has not been seen since August 2022. Additionally, the number of unemployed over 27 weeks rose from 1.22 to 1.245 million, which sits at the six-month average.

Bureau of Labor Statistics Bureau of Labor Statistics

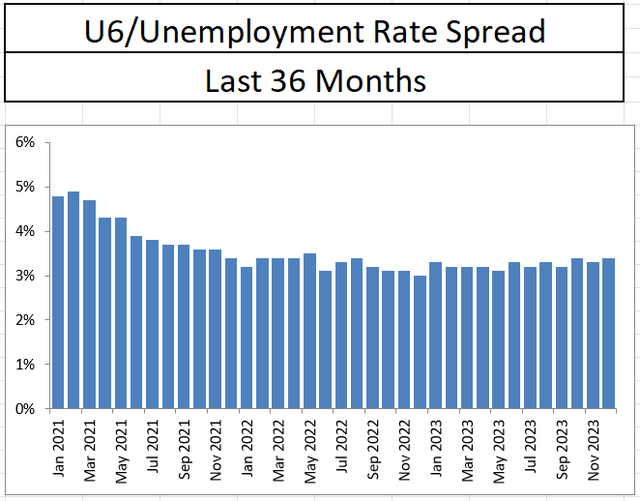

One metric that has ticked up slightly in recent months is the U6/U3 spread. The U6 rate is the broadest measure of unemployment which includes workers who wish for full-time work but are not getting full-time hours. The gap between U6 and U3 signifies the number of underutilized workers in the labor force. After running between 3.1 and 3.3% for over a year, December’s reading was at 3.4% for the second time in three months. This number matches pre-pandemic levels signaling a return to normalcy in the number of underutilized workers.

Bureau of Labor Statistics

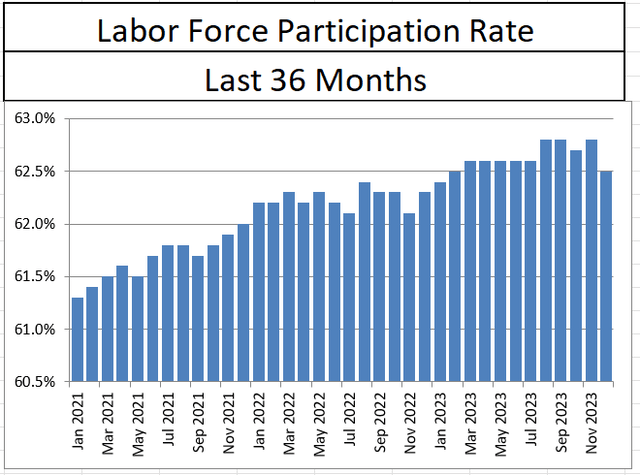

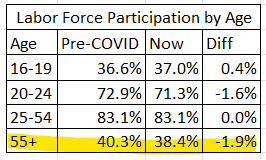

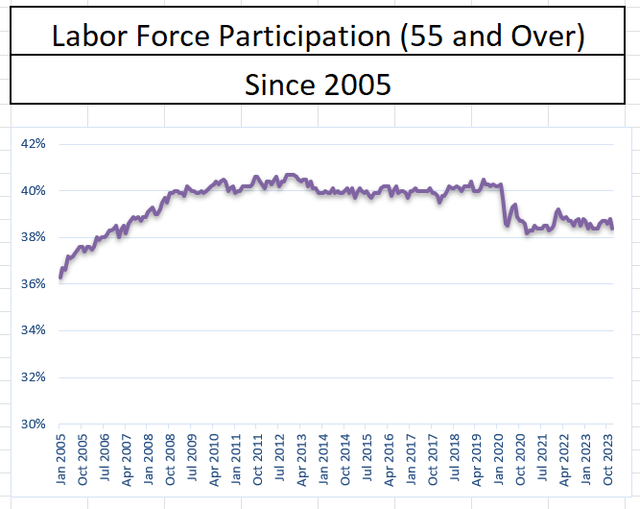

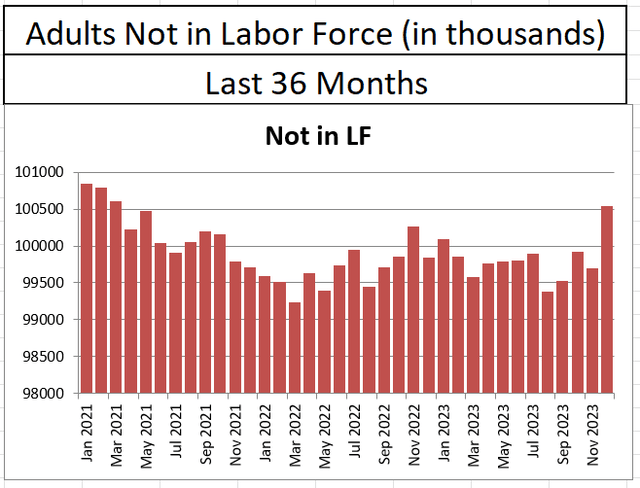

One big disappointment in the December jobs report was the drop in the labor force participation rate. After rising to 62.8% during the second half of this year, labor force participation fell to 62.5% in December, the lowest level since February. While the prevailing opinion is that young people are leaving the workforce, December’s drop in labor force participation came from the cohort aged 55 and over. In fact, labor force participation for workers over the age of 55 has remained impaired since the start of the pandemic. The number of adults not in the labor force jumped to over 100.5 million in December, the highest level since March of 2021.

Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics Bureau of Labor Statistics

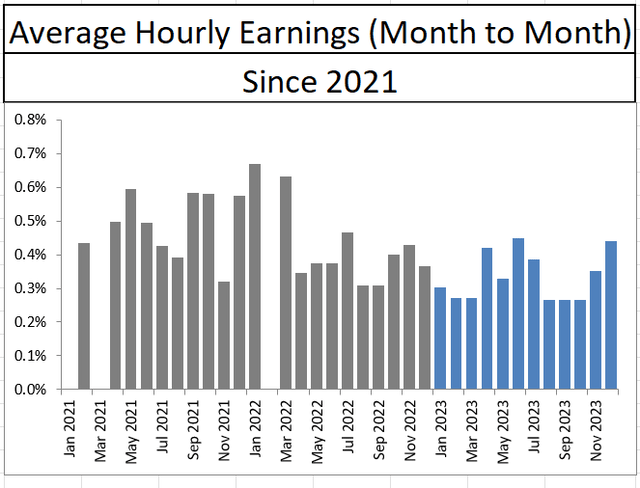

The pressure that the 55 and over crowd is placing on the supply of labor raises serious concerns about the Fed’s ability to continue to lower inflation while simultaneously lowering interest rates. The drop in labor force participation in December was likely a strong factor in average hourly earnings jumping 0.4% in December, the highest monthly jump since June.

Bureau of Labor Statistics

The December jobs report data does not support lowering interest rates. The labor supply pressures related to the exit of workers over the age of 55 are going to create a strain on employers who in turn must pay workers more to retain them. Should interest rates fall, it will further fuel this trend causing additional wage pressures and a reignition of inflation. Investors should prepare for the Fed funds rate to remain closer to the committee’s previous estimates of flat versus any other scenario.

Read the full article here