: Investing In A Sweeter Future")

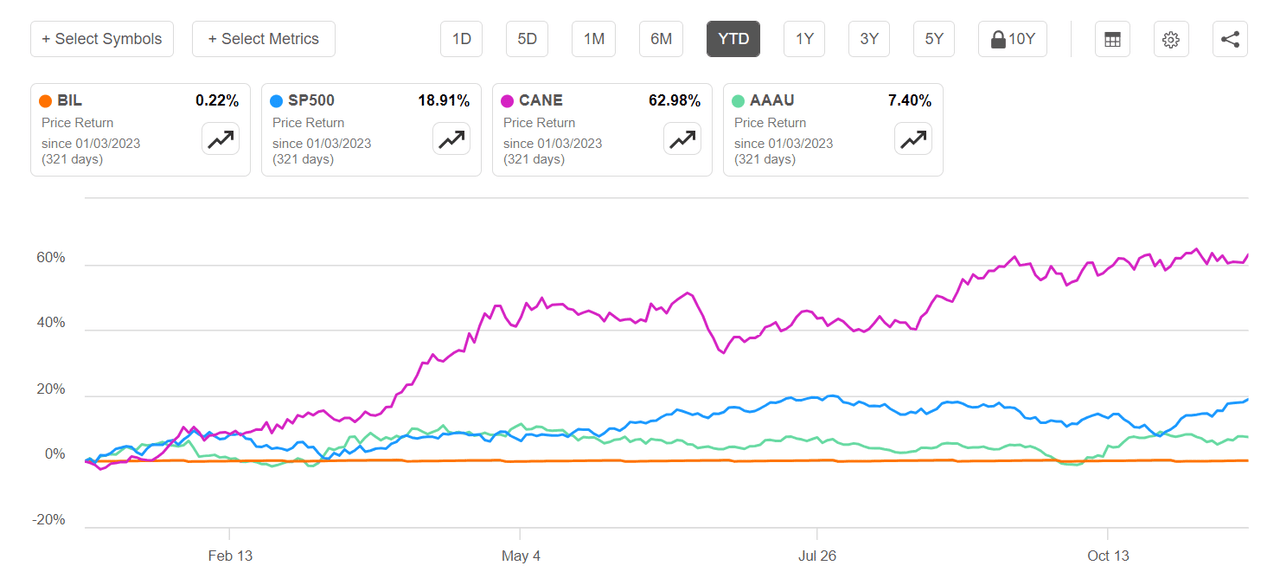

Risk is an important aspect of any type of investing, and in a volatile market, it’s even more important to try and manage your downside risks. Many investors prefer well-known and widely publicized safe havens such as government bonds or physical gold and precious metals. Against the current quasi-risk-off economic backdrop that 2023 gave us, I’d probably recommend short-term treasury bill ETFs such as the SPDR® Bloomberg 1-3 Month T-Bill ETF (BIL) or Goldman Sachs Physical Gold ETF (AAAU). However, these are not the subjects of today’s discussion.

Today, I wanted to explore a commodity ETF that has significantly outperformed both these ETFs on a year-to-date basis, is still showing strong price momentum, and is expected to show strong price appreciation in the near term. My only caveat would be that this is NOT a long-term buy-and-hold investment idea, although you could explore that option with a licensed financial advisor. This is essentially a cascade play on the forces influencing future sugar prices. The cascade in question begins with an unusually warm El Niño, which led to sugarcane crop damage in Asia, as described later on, which led to global price increases, which leads directly to my thesis of investing in sugar at this time. The cherry on top is the fact that much of the downside risk has already been mitigated, as we’ll see.

Enter the Teucrium Sugar ETF (NYSEARCA:CANE) as my investment vehicle of choice.

Seeking Alpha

If you’d invested in CANE at the beginning of 2023, your return so far would have been in excess of 30%. The downside risk here is minimal, which is important to my thesis. Commodities follow cycles, and while I certainly don’t recommend chasing these cycles, the current situation presents an excellent opportunity to generate alpha with only a modicum of risk.

Why Sugar?

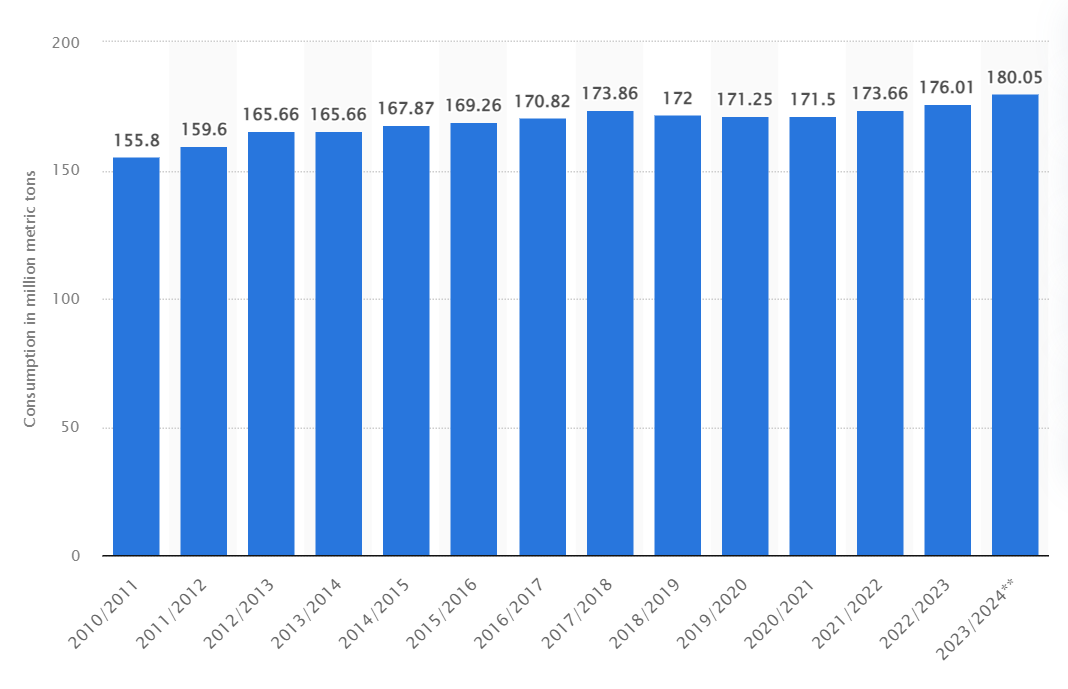

The simplest answer is that sugar is one of the most highly traded commodities in the world, and consumption has been growing for a long time. The real answer is that nobody looks to generate huge alpha with commodities. But just look at these estimates from Statista, which shows consumption moving a little more steeply from the 2020/2021 period up to the current period; a CAGR of roughly 1.6%.

Statista | Global Sugar Consumption 2010A to 2024E

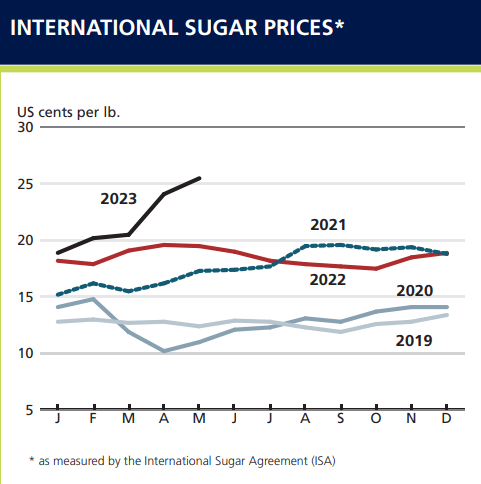

Zooming into the short-term, the October 2023 CPI report from the Bureau of Labor Statistics in the U.S. shows that the sugar and sweets segment saw a price increase of 5.2% over the prior period. Globally, as well, prices are set to increase even further due to significant crop damage caused by El Niño in two of the world’s largest sugar-exporting countries – India and Thailand. The United Nations Food and Agriculture Organization is predicting a production decline of at least 2% for the 2023-2024 crop season. Of course, Brazilian exports should help offset that to a certain extent, but there’s a problem. Brazil is technically ‘down under’, or in the Southern Hemisphere, so its sugarcane harvesting won’t be done until around the end of the first quarter of 2024. That means there’s an opportunity here for outsized gains.

Another source helps put this in a much more dire perspective:

The world now has less than 68 days of sugar in stockpiles to meet its needs, compared with 106 days when they began declining in 2020, according to data from the USDA.

And here’s the result of that…

Fao.org

Investing in sugar now is probably the best way to generate that alpha in your portfolio. Of course, the expense ratio for CANE is a little steep at 0.29%, but the IRR over the next 1 to 2 quarters should adequately offset that without allowing it to erode your total return too much.

With that, let’s look at the ETF itself, how it’s performed on different timelines, and why it makes sense to invest at this particular time.

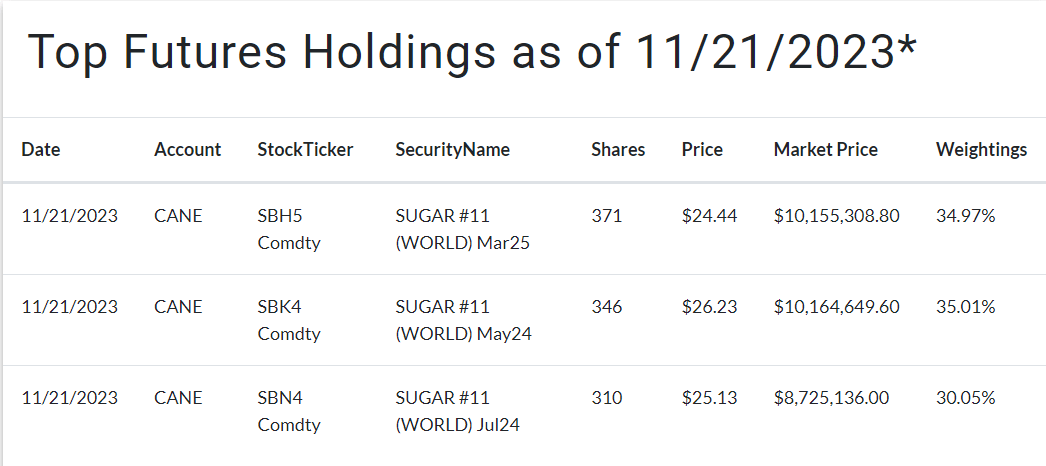

About CANE ETF Holdings

CANE holds mostly sugar futures, as outlined below:

“The three futures contracts for sugar (“Sugar Futures Contracts”) that are traded on the Intercontinental Exchange, also known as ICE Futures US (“ICE Futures”), are specifically:

(1) the second-to-expire Sugar No. 11 Futures Contract (a “Sugar No. 11 Futures Contract”), weighted 35%,

(2) the third-to-expire Sugar No. 11 Futures Contract, weighted 30%, and

(3) the Sugar No. 11 Futures Contract expiring in the March following the expiration month of the third-to-expire contract, weighted 35%.”

Teucrium | Teucrium Holdings

The fund also invests in mutual funds – specifically, the Goldman Sachs Financial Square Government Fund Inst (FGTTX) – as well as commercial paper, equities, and cash, but the bulk of its holdings are concentrated in sugar futures. Investors should also note that the ETF does NOT track sugar spot prices. It makes its money primarily from rolling over its futures contracts.

CANE ETF Performance

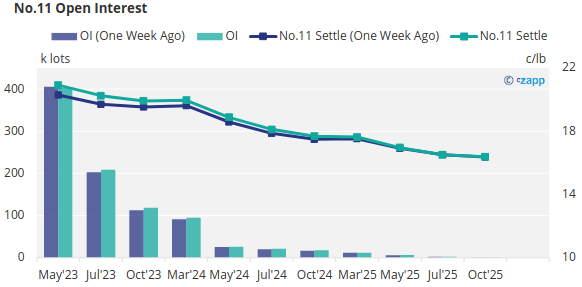

Since CANE doesn’t pay a dividend like many other ETFs, your entire return is dependent on sugar futures and how Teucrium Trading executes its futures rollover strategy. However, there’s a clear distinction between this strategy and the one used by the benchmark S&P GSCI because of the laddered structure of Teucreum’s contracts. While this protects the investment to a great extent from the effects of contango, the important point is that it can deliver outsized returns when sugar futures are in steep contango. Admittedly, this is a rare occurrence and only happens during times of mass market upheaval, as in March 2020, but you can see that March 2024 futures are expected to be in contango, albeit not as steeply as we’d want it to be.

Czapp | Sugar Futures OI and Settle

Another view is that commodity prices in comparison to equities are now at 50-year lows, and it could be time for another supercycle. I feel that’s quite speculative at this point, but it’s undeniable that sugar is in a bullish phase right now.

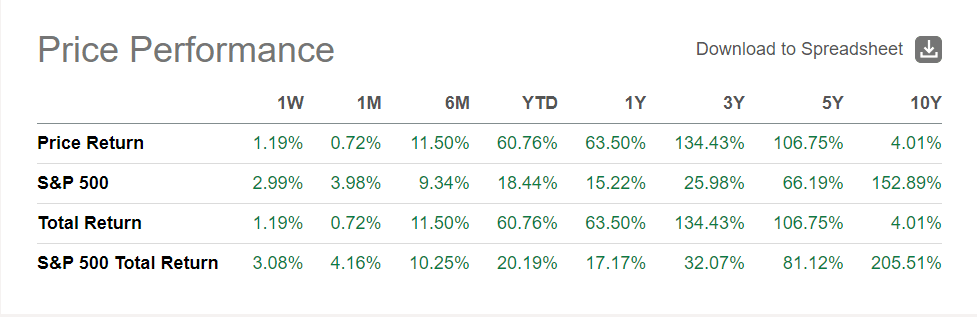

Case in point: CANE’s returns this year are undeniable. We’ve seen the YTD figure of +60% earlier in the article, but here’s how it’s performed on different timelines.

CANE vs SP500 Price and Total Return for Different Periods

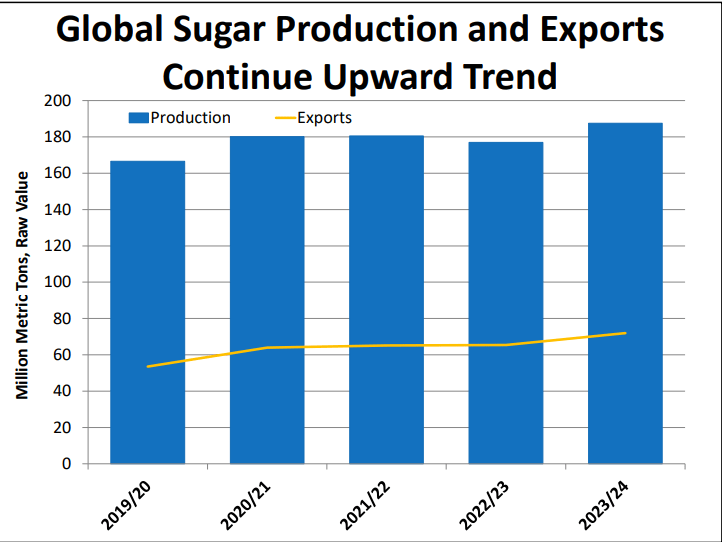

The first thing you’ll probably notice is the poor 10-year performance. This is not an investment for the long term. Remember: The core of my thesis here is that the global sugar supply is likely to be tight until Brazil’s output after Q1 helps offset the crop damage-related losses of the year. The other aspect is the demand side. Global demand for sugar is only going to increase in the future, as projected in the following chart.

USDA FAS

Downside Risks

I don’t wish to downplay the risks involved in this investment idea. Commodities are volatile by nature because they’re subject to the vagaries of the weather, political posturing, supply-chain dynamics, and other macro forces that dictate changes in the price of sugar futures.

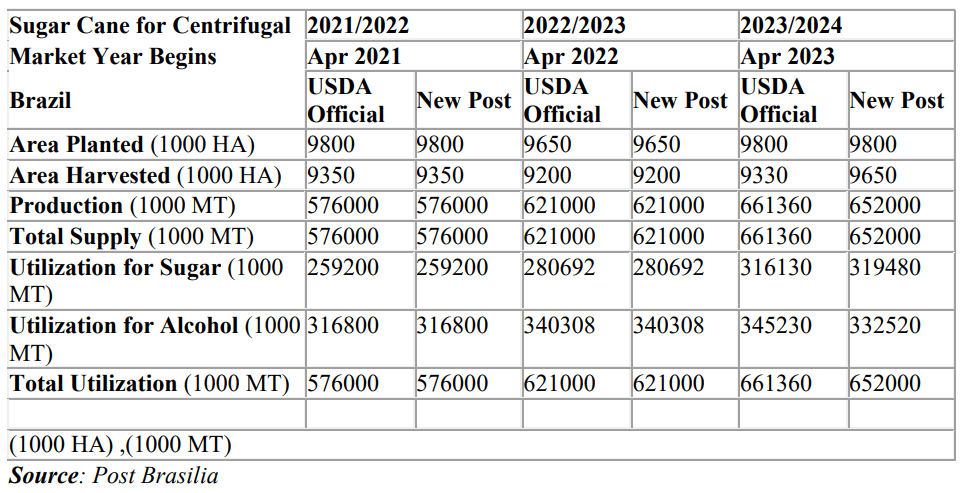

One example of this is Brazilian sugar exports. Brazil is expected to see a 20% increase in its current cycle, but there’s also a catch – because sugarcane is also needed for the ethanol industry. The risk here is that an increase in ethanol prices might just tip the scales against the amount of sugarcane produced for making sugar versus what’s required for making ethanol. A similar phenomenon was seen earlier this year, when Petrobras (PBR) cut fuel prices, which in turn pushed down ethanol prices in relation to sugar prices, thereby prompting mills to focus on sugar production over ethanol production. The fact that sugar prices are even more elevated now has prompted a smaller increase for ethanol and a larger one for sugar, in terms of the sugarcane supply being apportioned between sugar and ethanol, as shown in the table below.

To summarize, projected utilization for sugar is expected to go from 280 MMT to somewhere between 316 and 319 MMT, while the same figure for ethanol is expected to go from 340 MMT – either down to 332.5 MMT or slightly increase to 345 MMT.

Via USDA FAS

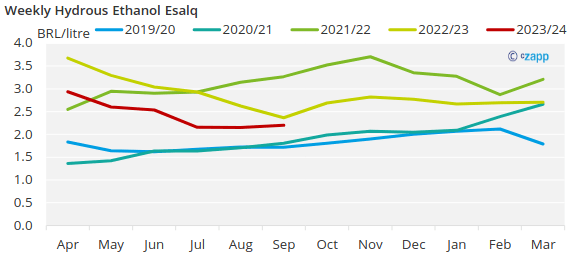

In other words, although the risk of a shift in this sugar-ethanol production ratio is certainly there, that risk is largely ameliorated by the fact that sugar prices are still on the rise, while ethanol prices are on the decline, as seen below.

Czapp

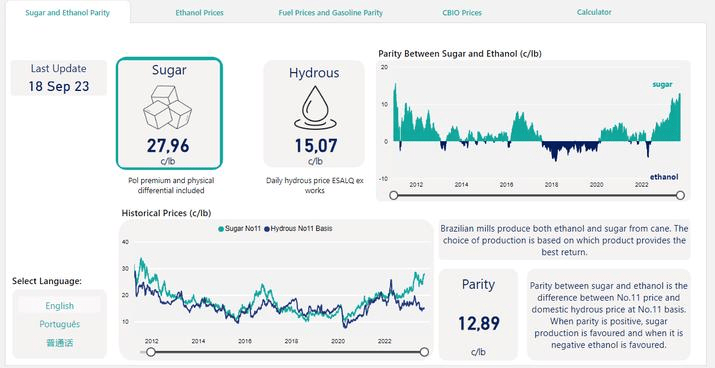

One of the key indicators of this is parity, which is the price differential between sugar and ethanol, as clearly outlined in this infographic – also from Czapp.

Czapp

And that’s where my confidence in this thesis comes from, really. If you remember, one of my most important considerations is to manage downside risk for bullish investments, and it just so happens that the market itself is doing that for us; but, again, only for the time frame of this thesis, which stretches into the first quarter of 2024 and into April, when the official season begins for last year’s cane crop. In reality, it could play out over an even longer time frame, depending on various factors such as the weather, etc. in 2024 in sugar-producing markets.

High-Level View for Investors

I’m rating CANE a Strong Buy for the reasons listed above, with the gist of my thesis being that the ETF is very likely to benefit from the set-up for the 2023/2024 sugar season. With Brazil still in the game, there’s certainly some amount of risk, but that’s largely mitigated by the sugar-ethanol price parity, which is the highest we’ve seen in over a decade.

Opportunities like this don’t present themselves so neatly packaged, and if you’re willing to step out of that safe-haven comfort zone and take on a modicum of risk, this could end up being a truly sweet deal. Of course, I have to qualify that by saying that I am not a licensed financial advisor, so please do your own DD before investing in anything I recommend. These are just my evidence-based opinions that may or may not play out as intended. As always, only invest what you’re willing to lose. Good luck!

Read the full article here