Introduction and Investment Thesis

Doximity (NYSE:DOCS) is a digital platform for US medical professionals that enables them to be more productive and provide better care for their patients. The company stock declined -15% in 2023, severely underperforming the S&P 500 and the Nasdaq 100. While Doximity is operating in a large and growing total addressable market and its management is committed to improving overall profitability, the company is seeing a slowdown in revenue growth and a decline in its net revenue retention rate. The management believes that the slowdown in revenue growth is partly attributed to an uncertain macroeconomic environment, where pharmaceutical budgets continue to come under greater scrutiny.

Based on my analysis of Doximity, I believe that the stock’s valuation is reflecting the worst-case scenario at the moment, where the company continues to see anemic growth over the next 5 years. As a result, I believe that the downside to the stock is limited. However, until I get further clarity on the management’s game plan to drive revenue growth in the coming years, it will be difficult to assess the magnitude of the upside of the stock at the same time. As a result, I believe that Doximity is a hold for now.

About Doximity

Doximity is a cloud platform that enables physicians to collaborate with their colleagues, securely coordinate patient care, conduct virtual patient visits, stay up-to-date with the latest medical news and research, monitor their work schedules, and manage their careers.

The Doximity platform is free to join and use for US medical professionals. Once verified, members gain access to Doximity’s professional social network for physicians, newsfeed, and productivity tools.

Meanwhile, Doximity’s revenue-generating customers include pharmaceutical manufacturers, health systems, and medical recruiting firms, where they offer marketing, hiring, and telehealth solutions predominantly on a subscription basis.

The Bull Case for Doximity

Doximity has a growing TAM and an innovative product pipeline.

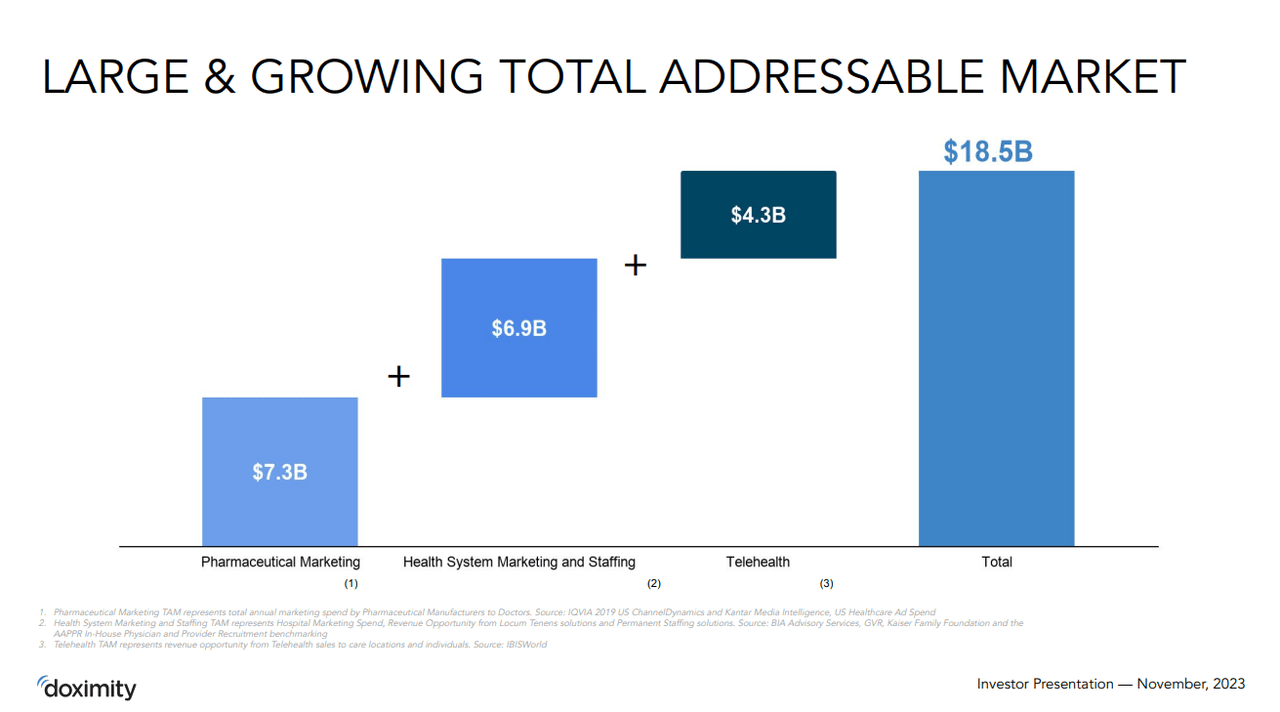

As per its latest Analyst Day, Doximity management projects their total addressable market (TAM) at $18.5B. The total addressable market size is calculated by summing the sizes of the following markets: Pharmaceutical marketing ($7.3B TAM), Health System marketing and staffing ($6.9B TAM) and Telehealth ($4.3B TAM).

As per management guidance, the company is expected to generate revenue in the range of $460M-$472M in its fiscal year, ending March 31, 2024. Should the management meet its revenue guidance, that would translate to a market share of approximately 2.5%.

2023 Investor Presentation

Over time, I expect Doximity to continue growing its social network of medical professionals, adding more members to its platform. I see this as a strength for Doximity’s platform since the company’s core revenue-generating members, medical entities such as pharmaceutical manufacturers, health systems, and medical recruiting firms, increase their revenue-based usage of Doximity’s social network by using the tool as a marketing and hiring channel similar to the network dynamics seen in broader professional networks such as LinkedIn.

I also believe that Doximity will continue to innovate to add new tools and solutions. As per the latest quarter, they introduced two new products in Q2, DocDefender and the pharmaceutical client portal.

In my view, their current product pipeline showcases the company’s commitment to innovate and meet the evolving needs of its user base. This should allow the company to attract new members and customers while increasing the engagement of existing ones.

Management continues to demonstrate superior financial discipline

Doximity was able to beat both top- and bottom-line expectations in its latest Q2 FY24 earnings report by 4.2% and 22%, respectively. Revenue grew 11% YoY to $113.6M, driven by a much faster rise in large customers contributing to $1M in revenue, which grew at 28% YoY. Meanwhile, its adjusted EBITDA grew 18% YoY to $54.2M, as the company saw its adjusted EBITDA margin expand by 2.7% points to 47.7%. This was driven by streamlining both Sales and Marketing spend and Research and Development spend, as non-GAAP operating expenses rose much slower compared to overall revenue growth at 7.6%, which allowed for the overall adjusted EBITDA margin expansion. I believe this is indicative of the underlying growing strength of the operational efficiency of the company. Meanwhile, Doximity also managed to improve its gross margins to 90.9%, driven by the scale and network effect of the platform.

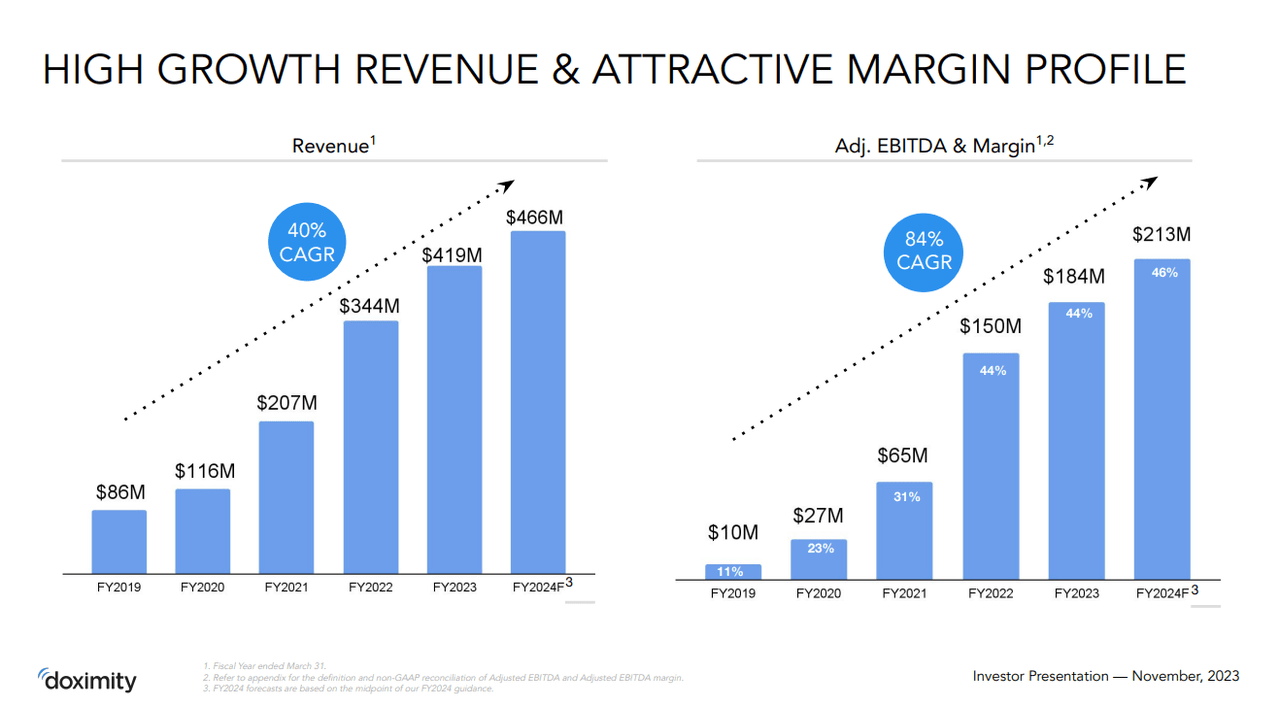

As we can also see from the investor presentation, the company management has always focused on driving profitable growth, as adjusted EBITDA has grown at a faster compounded annual growth rate (CAGR) of 84% since FY2019 than its revenue, which has grown at a CAGR of 40% during this period of time. This has allowed the company to grow its adjusted EBITDA margins from 11% in FY2019 to a projected 45.7% in FY2024. Meanwhile, the management expects revenue to grow 11.5% in FY24.

2023 Investor Presentation

The Bear Case for Doximity

Revenue growth is slowing, with net revenue retention rates falling amidst macroeconomic uncertainty

Although Doximity has shown strengths in its product pipeline and its focus on growing profitably, the company’s revenue growth has been slowing steadily. While its revenue has grown at a CAGR of 40% over the last 5 years, the company is expected to grow its revenue by 11.5% in FY24 and 10.3% in FY25, as per consensus estimates. In their latest earnings call, the management attributed the slowdown in revenue growth to the uncertain macroeconomic conditions. As per their latest earnings call, the management withdrew their 5-year growth target, though they reiterated their internal stretch target of $1B in revenue by 2028.

I believe the weakness that Doximity has experienced could be part of the broader slowdown that the pharma and healthcare industry is noticing. In 2022, Deloitte had conducted a study that examined the R&D spend of the Top 20 pharma companies in the world, where it found that the average cost to develop an asset from discovery to launch had increased by 13.5% to $2.2B. At the same time, the average forecast peak sales per asset in the pipeline also declined from $500M in 2021 to $389M in 2022. In my view, this is resulting in higher budget scrutiny across pharma companies, which is also putting downward pressure on overall sales momentum at Doximity.

Furthermore, the net revenue retention rate currently stands at 114%, which has been declining steadily, as can be seen below. While this tells me that the company is still able to generate additional revenue from upsells and expanding within existing current accounts, there is a growing spend fatigue amongst them, which aligns with the overall macroeconomic pressures.

2023 10K

Moving forward, should we see further deterioration in the net revenue retention rate, it would be a very clear indication that Doximity’s ability to retain its customers’ spending is falling behind.

Tying it together: I believe Doximity stock is a hold for now

Doximity severely underperformed the indices in 2023. The stock is currently trading at a forward price-to-earnings ratio of 33, when its earnings are expected to grow approximately 11% in FY25 as per consensus estimates, assuming an adjusted EBITDA margin of 45%–46%.

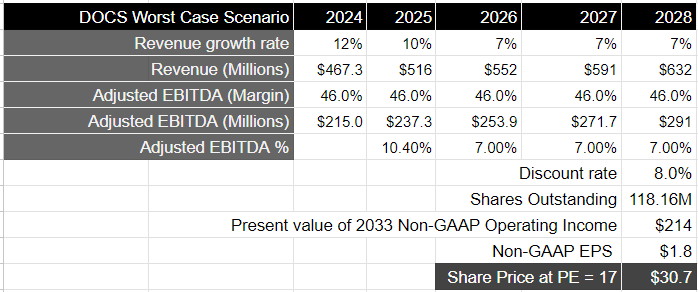

Looking at a 5-year investment horizon, the market is currently pricing Doximity to grow its earnings in line with the 10-year average of the S&P 500 at 7-8%. As the management has retracted their 5-year targets due to the uncertain macroeconomic environment, investors are attaching no additional premium to investing in Doximity vs. the S&P 500. In my opinion, this is the worst-case scenario, and it may play out if management is unable to further innovate its product pipeline to build engagement in its existing customer cohort and attract new ones. Should the worst-case scenario indeed play out, I expect Doximity to produce $291M in adjusted EBITDA in 2028, which would translate to a present value of $214, when discounted at 8%, or an adjusted earnings per share of $1.8. In this case, Doximity will be trading at a price-to-earnings ratio equal to the 10-year average of the S&P 500, which is between 15 and 18. This would equate to a share value of approximately $30, which is the current price level of the stock. Therefore, I believe that given Doximity’s current price, it is fully priced in the worst-case scenario, and I don’t expect a significant downside from current levels.

Future earnings expectations built into stock valuation over a 5-year investment horizon

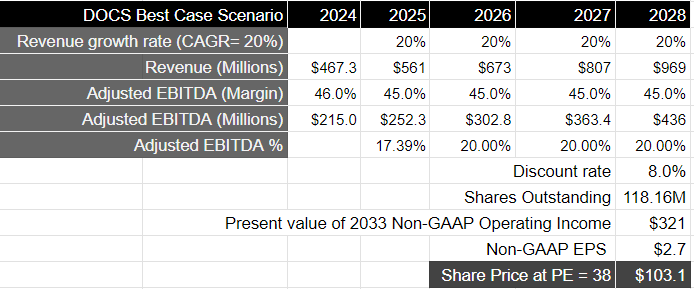

On the other hand, in the best-case scenario, if the management is indeed able to meet its stretch target goal of $1B in revenue with an adjusted EBITDA margin of 45–46%, that would mean Doximity would produce an adjusted EBITDA of $450, which, if discounted by 8%, would translate to a present value of $331M, or an adjusted EBITDA per share of $2.8. During this period of time, the company will have grown its earnings by 20%, and using the S&P 500 as a proxy, it should then be trading at 2.5x the price-to-earnings multiple of the S&P 500. In that case, the stock would rise to its previous all-time highs of $100+.

Best-case scenario for Doximity if management meets stretch target

Unfortunately, given the lack of guidance and clarity on the management’s part, the current pace of revenue growth, and slowing net revenue retention rates, I would not recommend investing in the stock based on the best-case scenario. Having said that, I also believe that the downside potential for Doximity is limited, as the stock is currently pricing in earnings growth of 7-8%, which I believe is achievable. As a result, I am going to rate Doximity a Hold and assess management’s commentary in the upcoming earnings calls to understand if the company has a game plan for the best-case scenario to play out.

Conclusion

Doximity is experiencing a slowdown in revenue growth and net revenue retention rates amidst an uncertain macroeconomic environment where pharmaceutical budgets are coming under greater scrutiny. Furthermore, I believe the main reason that investor optimism has disappeared is because the management has retracted their 5-year growth plan as of the last earnings call.

However, the company continues to drive innovation in its product portfolio and is continuing to see its network grow in a large and growing TAM.

Given the set of uncertainties, the stock is currently pricing earnings to grow at par with the S&P 500 over the next 5 years. On the other hand, if the management is able to indeed meet their stretch target of $1B in revenue by 2028, there could be a sizable upside from current levels. However, due to the lack of clarity at the moment, I would be listening to management’s commentary in the upcoming earnings calls to see if the company has a game plan for meeting its stretch target. In the meantime, since I believe the downside is priced in, I will rate the stock a Hold.

Read the full article here