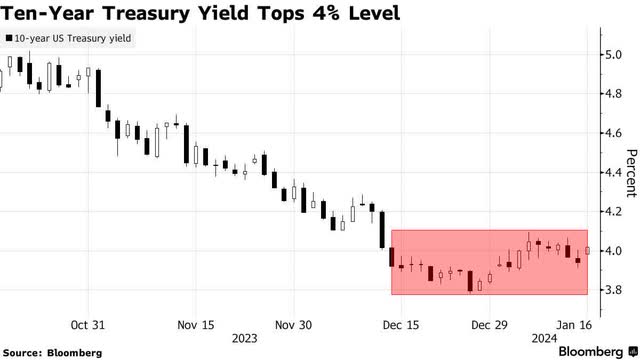

I’ve noted that the stock market has been looking for excuses to pullback and consolidate its fourth-quarter gains since the beginning of the year. It comes as no surprise that Fed Governor Christopher Waller, who has consistently leaned hawkish, was yesterday’s excuse. In testimony to a Senate committee, he asserted that there is no need for policy to be “rushed” in reference to when rate cuts would begin. He said that rate policy on an inflation-adjusted basis would be overly tight if not for the strength of the current economy. That modestly lowered the probability of a rate cut in March, which is still better than 60%, but it was sufficient to instigate selling in stocks and bonds, while strengthening the dollar.

Finviz

I cringe when I hear supposedly intelligent policy makers discuss future interest rate decisions, which work with a lag, based on coincident or lagging economic indicators. If it were not for the obvious attempt to manage expectations, I’d have a very different view of the markets and economy. This is one of several excuses to resolve the overbought condition we faced at year end, which is a process that should play out over the coming days and weeks until we set the stage for a run at new all-time highs in the S&P 500. Until then, prepare for a scare from bears, as we saw them do in March and October of last year.

Bloomberg

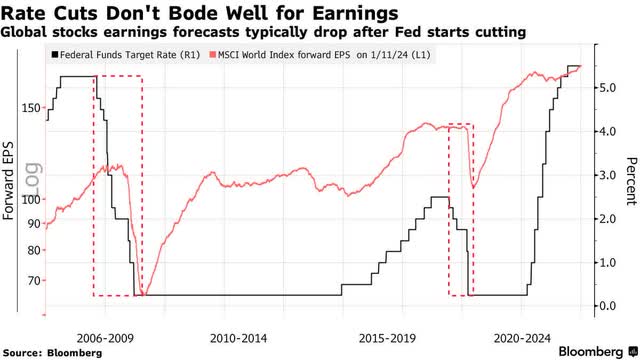

I’m seeing warnings that rate cuts from the Fed are a foreboding sign for corporate earnings. The supposed proof is in the chart below, which shows the Fed rapidly cutting short-term rates in concert with rapidly declining forward earnings estimates during the prior two rate-cut cycles. The Fed does cut rates when the economy is headed for a recession and corporate profitability is eroding, but that does not necessitate that if the Fed starts to cut in March and each meeting thereafter, we will see a steady decline in earnings expectations. The difference between today and the prior to cycles is that we are now on track for a soft landing rather than an economic downturn necessary to extinguish an excess that built up during the expansion.

Bloomberg

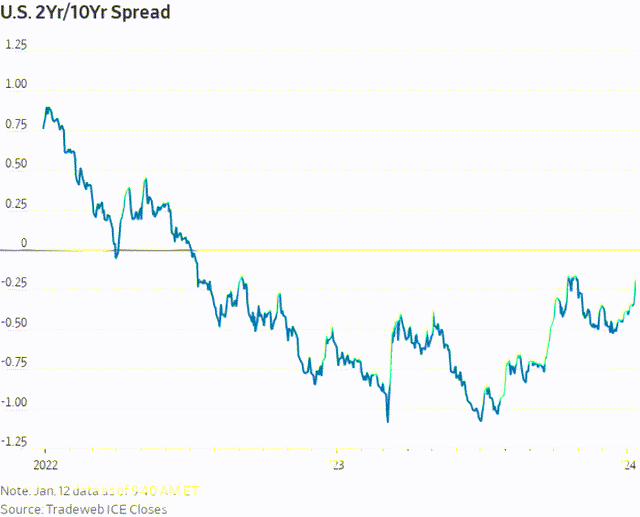

Another development that is being described as a foreboding sign is the un-inverting of the Treasury yield curve, whereby short-term rates fall back below long-term rates. This is close to happening between the 2-year and 10-year Treasury yields. Typically, the un-inversion occurs as a recession approaches, because the Fed is in a panic to lower short-term rates to stave off an economic downturn. Today, the rate cuts have everything to do with disinflation and nothing to do with a lack of economic growth.

MarketWatch

The most important variable this year is the timing of rate cuts. The Fed must thread the needle with them in terms of lowering rates soon enough and rapidly enough to avoid having the rate of economic growth slow too much. At the same time, it does not want to reignite inflation by loosening financial conditions too much, thereby stoking a surge in risk asset prices that creates an inflationary wealth effect.

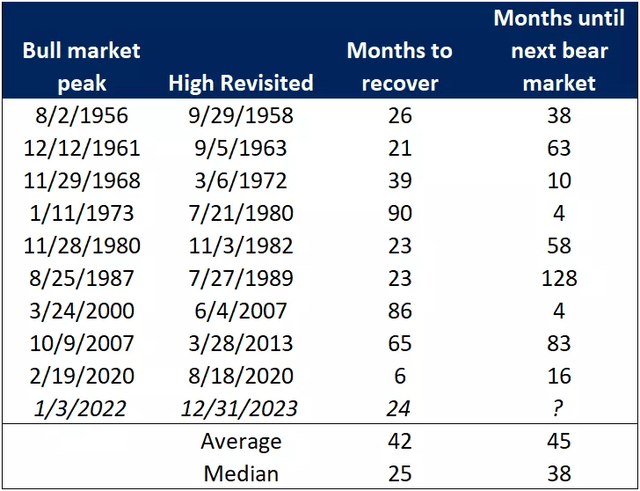

I am going to focus on the incoming economic data, as well as listening to markets to see whether they are on track. Assuming we continue to see new all-time highs in the major market averages, as we did for the Dow Jones Industrials at the beginning of the year, my confidence will build. New all-time highs typically portend positive performance in the year ahead. I think the S&P 500 looks poised for its own new all-time high in the near term. If so, it will have been 24 months since the prior bull market peak, which is right on target with the median length of time it typically takes. Once a new high is achieved, we usually don’t see another bear market for three more years. The anomalies, as seen in the chart below, were in 1980 and 2007, but I don’t see similarities between today and those periods in history.

Edward Jones

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

Read the full article here