")

The wisest are the most annoyed at the loss of time.”― Dante Alighieri

Shares of interleukin 6 inhibitor concern Tourmaline Bio, Inc. (NASDAQ:TRML) have rallied 200% since their public debut via reverse merger in October 2023. In TOUR006, the company potentially possesses a best-in-class therapy for both thyroid eye and atherosclerotic cardiovascular diseases. With both indications at the Phase 2 stage and competition expected to release Phase 3 data in 2025, Tourmaline warranted further investigation. An analysis follows below.

Seeking Alpha

Company Overview:

Tourmaline Bio, Inc. is a New York City based clinical-stage biopharmaceutical concern focused on the development of therapies that target diseases where interleukin 6 (IL-6)-induced inflammation plays a pivotal role. It has one asset in the clinic, TOUR006, which is pursuing two indications. Tourmaline was formed in 2022 and went public in October 2023, when it reversed merged into failed kidney transplant concern Talaris Therapeutics, with the new company emerging with cash of ~$210 million. Its first trade post-merger was conducted at $10.32 a share. Since that time, shares of TRML have enjoyed a significant surge. The stock currently trades around thirty bucks a share and sports an approximate market capitalization of $650 million.

The company in-licensed anti-IL-6 antibody TOUR006 from Pfizer (PFE) in May 2022 after the latter had studied it in the treatment of Crohn’s disease, lupus, and rheumatoid arthritis from 2010 to 2016 but elected to shelve it due to an internal reshuffling of program priorities, somewhat prompted by external competition from other IL-6 offerings. After previously promising cell therapy asset FCR001 derailed in a Phase 3 study, Talaris let go of 95% of its staff and sought strategic alternatives, ultimately landing on Tourmaline. In the reverse-merger transaction, legacy Talaris shareholders received a $64.4 million dividend and 22% ownership interest in the new company. Another 59% went to legacy Tourmaline shareholders, with the 19% balance earmarked for private placement investors who provided capital of $75 million.

Company Website

TOUR006

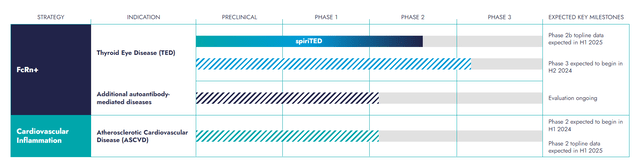

The investors in the new concern were essentially placing bets on TOUR006, which is being evaluated for two indications: thyroid eye disease (TED) and atherosclerotic cardiovascular disease (ASCD).

Company Website

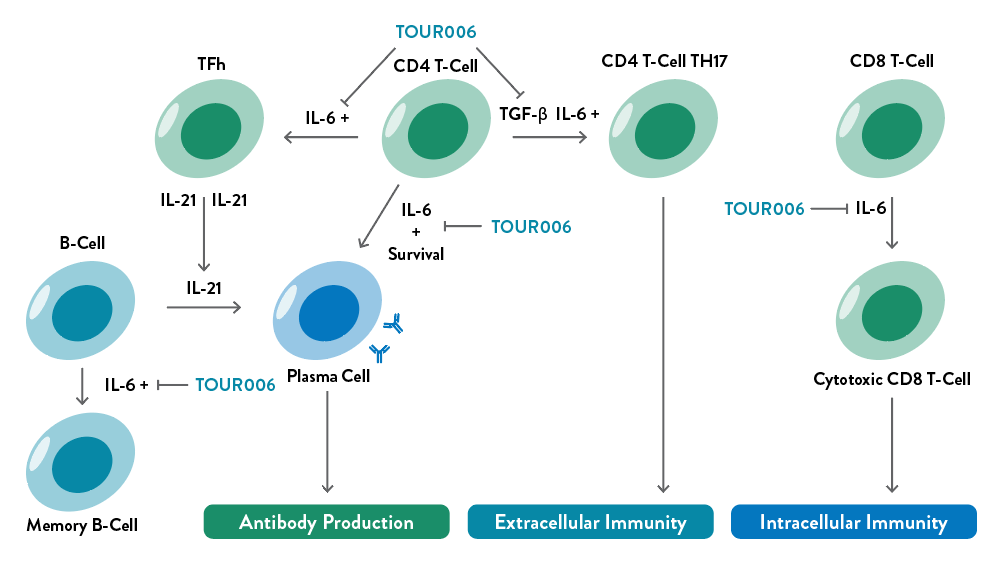

IL-6 inhibition therapies are already approved for ten indications, encompassing FY22 sales of ~$3.5 billion. However, management believes the number of additional indications that could benefit from IL-6 therapies is substantial, especially autoantibody driven maladies. TOUR006 appeared as a low-risk candidate for study against autoantibody disorders such as TED and ASCD, owing to its long half-life (~7 weeks), subcutaneous administration, and prior clinical package that suggested it could block IL-6 without significant safety concerns (only two of Pfizer’s 448 clinical patients developed anti-drug antibodies).

After acquiring its rights, Tourmaline entered TOUR006 into an ongoing Phase 2b trial (spiriTED) for the treatment of TED, an autoimmune disease characterized by proptosis (bulging eyes) and double vision that afflicts ~30,000 Americans annually. Its pathophysiology is driven by autoantibodies that bind to the TSH (thyrotropin) receptor, common in cell types surrounding the eye and the thyroid. In fact, up to 95% of TED patients also suffer from Graves’ hyperthyroidism. Management believes that elevated IL-6 levels are a significant contributing factor in TED pathogenesis.

Approximately two-thirds of TED patients are diagnosed as moderate or severe, with the former being treated with steroids, and the latter attacked by Amgen’s (AMGN) intravenously administered IGF-1R inhibitor Tepezza (teprotumumab). However, Tepezza is the subject of over 50 lawsuits regarding hearing loss and impairment events likely due to on-target IGF-1 pathway inhibition. It also must be administered once every three weeks eight times. Roche’s (OTCQX:RHHBY) subcutaneously injected IL-6 inhibitor Enspryrng (satralizumab) is approved for neuromyelitis optica spectrum disorder, but there is currently no FDA-approved IL-6 therapy for TED. That said, Roche has entered satralizumab into a Phase 3 TED trial (Satra-GO) with top-line data due in 2025.

More than a year behind, TOUR006 is under investigation in the 81-patient spiriTED 2b study encompassing three cohorts in a first-line setting. Two cohorts will receive either 20mg or 50mg TOUR006 administered once every eight weeks three times, with the other receiving placebo. The primary endpoint is proptosis response at week 20. Top-line data from spiriTED are expected in 1H25, although Tourmaline is expecting to initiate a Phase 3 TED study for TOUR006 before those results are announced (in 2H24) with a top-line readout anticipated in 2026.

As for ASCD, the company has clearance from the FDA to initiate a Phase 2 trial for TOUR006, which should occur in 1H24, with results anticipated in 1H25. For this indication, there are over 24 million Americans, of which 55% exhibit elevated C-reactive protein (CRP) levels, a biomarker for IL-6 signaling. TOUR006 is in competition with other clinical IL-6 inhibitors, including CSL Behring’s clazakizumab, which is administered once-monthly intravenously with ~5% of patients experiencing anti-drug antibodies; and Novo Nordisk’s (NVO) ziltivekimab, which is administered once-monthly subcutaneously but with patients subject to anti-drug antibodies at a ~10% clip. By contrast, Tourmaline is hoping that TOUR006 will separate itself through once quarterly administration and a lower number (~1%) of patients experiencing anti-drug antibodies.

The company’s trial will evaluate three dosages of TOUR006 (15mg, 25mg, and 50mg once quarterly) and one placebo dose in 120 cardiovascular disease patients with chronic kidney disease (CKD) after a six-month dosing period. Primary endpoints will include several biomarkers, including high-sensitivity CRP, serum amyloid A, fibrinogen, and lipoprotein(a) levels. Competitor Novo Nordisk has entered ziltivekimab into three Phase 3 cardiovascular outcome trials covering ~22,000 patients, of which the most significant (as far as Tourmaline is concerned) is a ~6,200 patient ASCVD study ‘ZEUS’ with its primary endpoint the time to first occurrence of a major adverse cardiovascular event, defined as cardiovascular death, non-fatal myocardial infarction, or non-fatal stroke. Data are expected from that study in 2025. Also, CSL Behring’s clazakizumab is undergoing assessment in two studies, but both are related to kidney disease.

Pfizer Deal Economics

To onboard TOUR006, Tourmaline paid $5 million upfront and issued stock to Pfizer equal to 15% of its total outstanding post-transaction. Tourmaline is also potentially on the hook for development and regulatory milestones of $128 million and commercial milestones of $525 million, plus low double-digit royalties less than 15% on net sales. Also, Pfizer has first right-of refusal on any out-licensing deal in the U.S.

Balance Sheet & Analyst Commentary:

Although no real burn rate has been established, management believes that its cash of ~$210 million (as of October 20, 2023) is enough to operate through 2026.

Surprisingly, given the relative newness of Tourmaline, the company has quite prolific and positive sponsorship from the Street, with six buy or outperform ratings versus no holds or worse. Their median price objective is $46.50.

Two insiders were active shortly after the company went public, with CEO Sandeep Kulkarni (4,000 shares at $16.99) and board member Parvinder Thiara (1,000 shares at $17.31) buying on November 17, 2023.

Verdict:

It should be noted that they are both up handsomely since their purchases. With a potentially best-in-class IL-6 inhibitor featuring superior once-quarterly subcutaneous administration, there is plenty to like regarding TOUR006. Furthermore, management believes its sole asset has applications beyond the two indications it is currently pursuing, including autoantibody driven diseases such as myasthenia gravis and autoimmune encephalitis.

That said, its Phase 2 trials, which are both scheduled to be read out in 1H25, are meaningfully behind its respective clinical competition. And besides for TOUR006 entering the clinic for a Phase 2 cardiovascular disease trial, there are no needle-moving catalysts in 2024. Although its sole asset has exhibited some early promise, shares of TRML have gotten ahead of themselves. With a 200% rally since going public and little data forthcoming for more than a year, I plan to maintain my small stake in TRML, until a meaningful pullback transpires, at which time, I will probably accumulate a few more shares.

The invariable mark of wisdom is to see the miraculous in the common.”― Emerson

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here