By Derek Deutsch, CFA, & Mary Jane McQuillen

Macro Clouds Lift a Little for Clean Energy

Market Overview

U.S. equities rose in the fourth quarter to end the year near all-time highs, helped by falling bond yields and growing optimism that the U.S. economy will pull off a soft landing. Signs of cooling inflation and a slowing labor market reversed a two-year climb in yields and increased the likelihood that the Federal Reserve had completed its tightening cycle. The benchmark Russell 3000 Index gained 12.07%, led by the real estate sector (+18.18%), which enjoyed some rate relief as 10-year U.S. Treasury yields (US10Y) fell 70 bps, mega cap stocks in the information technology (IT, +17.06%) and consumer discretionary (+13.10%) sectors, and cyclical financials (+15.12%) and industrials (+13.52%) sectors. Defensive consumer staples (+5.70%), health care (+7.17%) and utilities (+8.66%) sectors made positive gains but trailed the market in a risk-on quarter, while falling commodity prices made for negative returns for the energy sector (-6.57%).

Against this backdrop the Strategy outperformed, helped by strong contributions from economically sensitive financials stocks such as JPMorgan Chase (JPM), which weathered a challenging 2023 for financials and was a top contributor for the year after we entered our position in the first quarter following the banking crisis. Consumers and small businesses continue to look healthy, while spending has returned to pre-pandemic levels and new customer spending growth remains robust. JPMorgan’s integration of First Republic (OTCPK:FRCB) is proceeding as well as or better than expected, and in a year where cash deposits were dynamic, JPMorgan was able to gain share and retain customers due to its financial strength and diversity of offerings. Elsewhere in financials, BlackRock (BLK) also performed well as a leading asset manager that benefited from strong markets and its superior competitive position.

“Short-term interest rates are likely at peaks may drop in 2024, offering a potential macro tailwind for clean energy.”

Other positive contributions came from a variety of sectors, with strong execution a common denominator. Salesforce (CRM) delivered a high-quality quarter driven by data cloud and early AI uptake, which are fueling more aggressive customer purchasing activity. Combined with strong margin and free cash flow performance and plans for ongoing margin expansion and buybacks, this helped Salesforce cap off a year of significant rerating for the stock. Membership warehouse club retailer Costco (COST) reported better than expected earnings per share and operating margins in the quarter and announced its highest special dividend in a decade. Costco is also enjoying solid membership renewals and is poised for its e-commerce to return to growth.

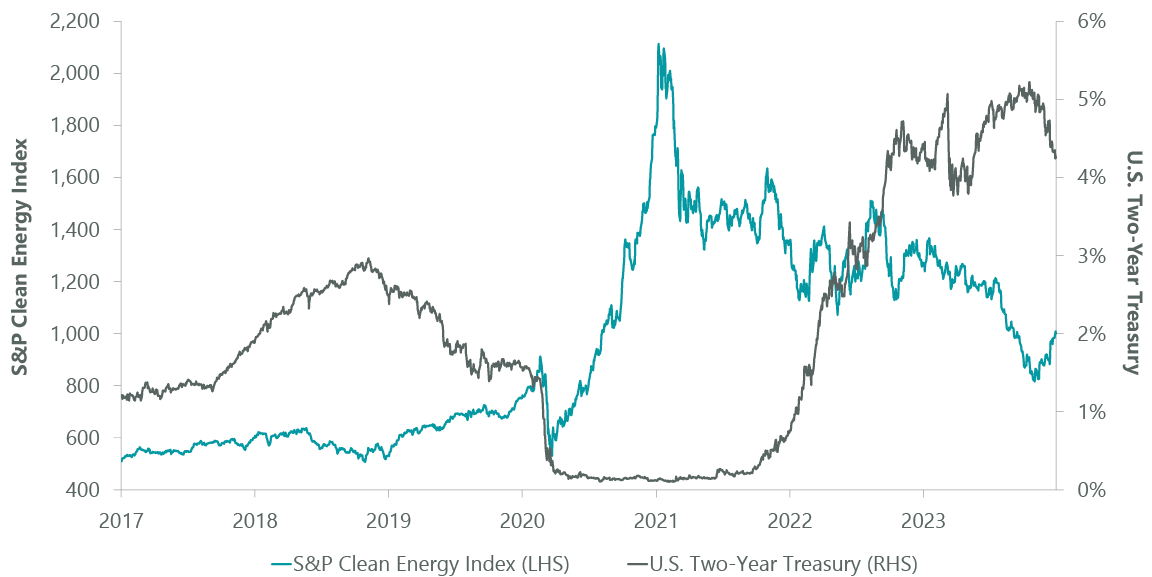

Interest-rate-driven headwinds pressured valuations for clean energy stocks throughout 2023 (Exhibit 1), and for much of the fourth quarter weighed on detractors SolarEdge Technologies (SEDG) and Shoals Technologies (SHLS). From a macro perspective, however, short-term interest rates are likely at peaks and yields may come down further in 2024, offering a potential macro tailwind for clean energy. SolarEdge and Shoals felt some of this tailwind in December, as they gained 18% and 12%, respectively, in the month. The timing in 2024 could be fortuitous for clean energy as a whole, as it would occur just as significant delayed cash flows from the Inflation Reduction Act (IRA) begin to fill balance sheets.

Exhibit 1: Rate Sensitivity of Clean Energy Stocks

As of Dec. 31, 2023. Source: ClearBridge Investments, Bloomberg Finance.

Other detractors included McCormick (MKC), which reported a mixed third quarter, with lower sales driven by a slower than expected recovery in China. Strong gross margin progress for McCormick overall and favorable market share progress in the key markets of North America and Europe should support its long-term growth opportunity. In IT, Cisco Systems was lower amid concerns of enterprise networking demand normalization and potential inventory correction.

Portfolio Positioning

We were active in adjusting the portfolio to reflect the shifting environment in the quarter, reducing our health care exposure ahead of a potentially volatile election year. We trimmed UnitedHealth (UNH) and BioMarin Pharmaceutical (BMRN) positions and exited Progyny (PGNY) and Thermo Fischer Scientific (TMO), the latter resetting its 2024 guidance and reinforcing our preference for Danaher (DHR), which has higher exposure to bioprocessing, which has positive prospects for a rebound in 2024.

Danaher also recently spun off Veralto (VLTO), an industrials business focused on water and product quality whose shares we inherited and to which we added in the quarter. Veralto is the market leader in water quality analysis and offers treatment solutions that improve the water cycle as well as packaging printing solutions that include traceability applications for food and beverage, consumer packaged goods and pharmaceutical products. Veralto’s water quality business has a clear positive environmental impact and is attractively levered to secular growth drivers around increasing threats of water contaminants and water scarcity. Veralto is a unique high-quality company with above-average industrial organic and inorganic growth. With 100% free cash flow conversion, nearly best-in-class operating margins and almost 60% of its revenues recurring, Veralto is a strong earnings compounder. Management has long-tenured Danaher roots and while M&A in Veralto’s businesses has been limited, the company’s management and board are highly experienced in M&A, offering a potential path to further growth as the spinoff allows more focused resources to accelerate organic growth and reignite margin expansion.

Outlook

The economic outlook is improving with the probability of a recession decreasing, and the Fed likely to pivot and lower the federal-funds rate in the months ahead. For the fourth quarter, more S&P 500 companies have issued negative than positive EPS guidance, although the year-over-year overall growth rate is still expected to be positive. This is consistent with a soft landing scenario of slower, but still positive, growth. In this environment we are cautiously optimistic and have positioned the portfolio to have some exposure to both defensive as well as cyclical characteristics. We remain focused on investing in companies that we believe can outperform through full market cycles and maintain our conviction that high-quality companies with leading sustainability profiles will prove to be rewarding long-term investments.

Portfolio Highlights

The ClearBridge Sustainability Leaders Strategy outperformed its Russell 3000 Index benchmark during the fourth quarter. On an absolute basis, the Strategy had gains in all 10 sectors in which it was invested (out of 11 sectors total). The main contributors were the IT and financials sectors.

On a relative basis, overall stock selection and sector allocation were beneficial. Stock selection in the financials, consumer staples, health care and consumer discretionary sectors were the main contributors. A lack of energy holdings was also beneficial. Conversely, stock selection in the IT sector and a health care overweight detracted.

On an individual stock basis, Microsoft, Apple, JPMorgan Chase, Salesforce and Costco were the largest contributors to absolute performance in the quarter. The main detractors from absolute returns were positions in SolarEdge Technologies, Shoals Technologies, McCormick, Cisco Systems and Aptiv (APTV).

Other positioning moves involved the sale of Bloom Energy (BE) in the industrials sector, as expectations for free cash flow generation have been pushed further out, and Charles Schwab (SCHW) in the financials sector, as the company’s cash sorting issues could take longer to play out and visibility is low, with potential for negative revisions.

ESG Highlights

An Enhanced Internal Engagement Initiative

Engagement to drive positive change in public equities has been a longstanding part of ClearBridge’s investment decision making and active ownership. As a long-term shareholder with an average stock holding period of five years, ClearBridge has cultivated strong and lasting relationships with company management teams. With this unique position and decades of industry experience, we’ve taken steps to better structure, measure and communicate the progress and outcomes of key engagements, and in 2022 we launched an enhanced internal engagement initiative, Engage for Impact (EFI).

The initiative encourages targeted engagements that we believe have a strong likelihood of creating positive impact, which we define as the creation of long-term positive environmental or social outcomes for the benefit of all stakeholders in public companies: their investors — our clients — and their employees, customers, suppliers and communities.

While we believe our work can often influence significant improvement at the company level, we also recognize we are one of many shareholders working to create change. In many cases this collective voice is what ultimately leads to positive, real-world impact.

As a part of this new initiative, investment team members develop specific “asks” or areas of improvement for priority target companies. Progress against these “asks” is then monitored and reported on over time.

As long-term investors, our company engagements can take place over a multiyear period. Therefore, throughout the course of the engagement, we track and categorize company progress by stages (Exhibit 2).

Exhibit 2: Engage for Impact Progress Framework

Source: ClearBridge Investments.

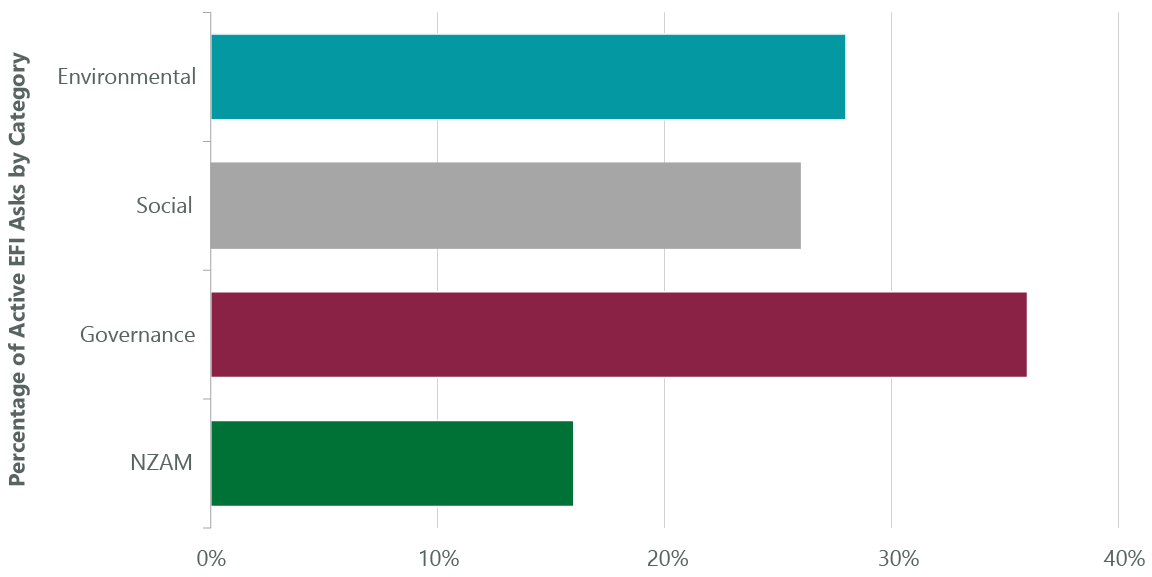

Using this framework, we can better monitor and track a company’s responsiveness and progress against key performance indicators and report on these outcomes over time. EFI engagements follow a consistent structure, prioritize topics closely aligned with value creation, represent a wide variety of sustainability topics (Exhibit 3), and are often rooted in firmwide focus areas like net zero, biodiversity, human rights, as well as diversity, equity and inclusion.

Exhibit 3: Engage for Impact Asks by Category

As of Dec. 31, 2023. Source: ClearBridge Investments.

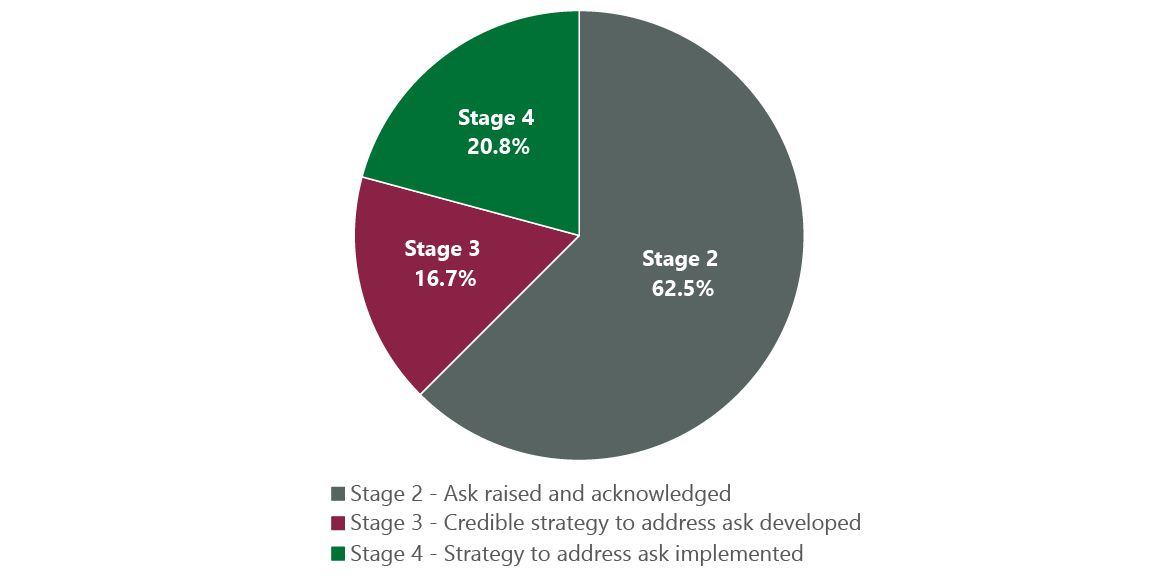

Given this enhanced initiative is still in the early stages, most of our EFI company asks are currently categorized as early stage or in-process (Exhibit 4). Examples of company asks focused on reducing emissions, improving labor relations, expanding electric vehicles (EVs), improving board effectiveness and implementing total shareholder return (TSR) metrics convey the spirit and overall benefits of the initiative.

Exhibit 4: ClearBridge Engage for Impact Asks by Stage

As of Dec. 31, 2023. Source: ClearBridge Investments. Stage 1 is not captured in the data because all EFI asks in the initiative have progressed past that stage.

Decarbonizing Aviation: United Parcel Service (UPS)

Reducing emissions is a common ask among ClearBridge’s company engagements broadly. For an EFI with United Parcel Service (UPS), we acted on the opportunity to formulate a specific ask for a reduction in Scope 1 and 2 emissions from its aviation fleet, which comprises ~300 planes. We actively engage with UPS on setting aggressive carbon reduction targets as its stock is held in a strategy that is in-scope for ClearBridge’s net-zero commitment.

In our engagements with UPS, we have discussed how due to heavy reliance on future technologies such as sustainable aviation fuel, the company recognizes it cannot credibly set a company-wide target approved by the Science-Based Targets initiative (SBTi) at this time. However, the company has acknowledged our ask as a key area of focus over the next 10-15 years and recognizes decarbonizing its aviation fleet is a key part of the global energy transition. It also recognizes the need to align all other parts of the business with a net-zero pathway in an effort to decarbonize. Efforts currently underway include investments in electrical vertical takeoff and landing aircraft and full electrification of its ground fleet, with a 2025 goal of 40% alternative fuel for ground vehicles, up from 24% today. We will continue to engage UPS as a stage 2 EFI to monitor progress against other reduction targets and continue to urge the company to decarbonize its aviation fleet.

Bettering Driver Relations and Expanding EVs: UBER

In stage 3 of an EFI the company has acknowledged the ask and has developed a credible strategy to address it. The company may even have begun and be well along in addressing it, as is the case with Uber and two asks we have formulated to: 1) improve driver satisfaction, and 2) expand its adoption of EVs toward achieving its net-zero goal.

We’ve engaged Uber since its IPO in 2019 as concerns over employee classification have led to questions of worker pay and benefits that we felt overshadowed other merits of its rideshare business, for example rideshare’s democratization of transportation and Uber’s impressive safety record.

In December 2019, we met with the company to discuss driver earnings and shared our view that drivers should remain contractors with added benefits and pay protection. At that time, Uber had already shifted its operating philosophy to a more conciliatory approach and improved relationships with contracted partners with guaranteed pay minimums, portable benefits and bargaining rights.

We continued the conversation as part of regular meetings with the company over subsequent years, and at a January 2024 meeting with Uber’s CEO, CFO and other representatives, we were pleased with progress made against both asks. Management highlighted improvements made to the driver experience, including technology, earnings and worker flexibility. Specifically related to driver earnings, the primary concern, drivers on the platform currently earn an average of ~$36 per utilized hour on a gross basis and low-$20s net of expenses and overhead. Up-front fares, which are now being rolled out globally, provide improved earnings transparency. On fairness, where drivers see anywhere from a 0% to 50% take rate (the percentage Uber takes of gross margins), Uber plans to share weekly reports with drivers clarifying take rates and distributing make-whole payments where appropriate.

To achieve its SBTi-approved net-zero goal by 2040, Uber is focusing on driver incentives and education to drive adoption of EVs across its platform. Results so far are promising and getting better: 4.7% of Uber’s trip miles driven in the U.S. and Canada are completed in zero-emission vehicles, even though EVs represent just ~1% of total cars on the road in the U.S.

Enhancing Board Quality and Operational Efficiency: Comcast (CMCSA)

Comcast is also at stage 3 in its EFI action as it is making measurable progress on EFI asks regarding 1) addressing some concerns from third-party governance research providers on overboarding and board effectiveness, 2) setting verified science-based targets and 3) addressing efficiency of operations, specifically as it relates to suppliers.

In December 2019, we engaged Comcast on a variety of ESG topics and raised the issue of board independence. We followed up in May 2020 when we discussed a proxy proposal on the split Chairman and CEO role. Following this meeting, Comcast improved the independence of its board, upping the percentage of independent director nominees from 80% in 2019 to 89% in 2022, as well as improving board diversity, from 40% of director nominees being diverse by gender or race in 2019 to 44% in 2022.

In December 2022, we continued the conversation around board effectiveness and engaged the company on its board structure, raising concerns around overboarding or having board members sit on too many boards, which may compromise their ability to serve the board effectively. This issue has been flagged by third-party governance research providers.

In a December 2023 engagement, Comcast shared that it was making progress addressing overboarding by bringing down the average tenure of its board by incorporating a policy on director overboarding into its corporate governance guidelines that limits the number of public company boards on which directors may serve. As part of the policy, no director who also serves as CEO at a public company may serve on more than three public company boards. A notable example is lead independent director Ed Breen, who is also the current CEO of DuPont de Nemours. He proactively sought to reduce the number of boards he sits on and chose not to stand for re-election to the board of International Flavors & Fragrances at the company’s 2023 annual meeting.

Also at our December 2023 meeting, Comcast disclosed its Scope 3 emissions for the first time and committed to setting a verified science-based target. The company has begun engaging suppliers on committing to set a verified target, and going forward, it will set clearer targets around Scope 3 emissions. Regarding our ask around operational efficiency, Comcast has reduced the electricity needed to deliver each byte of data across its network by 36% since 2019 and is pushing its suppliers to be more efficient.

Improving Incentive Metrics and Committing to Net Zero: Western Digital (WDC)

In a completed EFI journey, Western Digital has implemented a strategy to address asks we made over several engagements to 1) institute relative total shareholder return (TSR) incentive metrics to evaluate shareholder value creation compared to industry peers, 2) improve energy intensity levels of manufacturing in line with industry peers and 3) commit to a net-zero target.

Specifically, Western Digital reduced the energy intensity of manufacturing its products by >13% from FY21 to FY22. It added relative TSR metrics to its incentive comp, which we view as positive as it aligns management compensation with execution, whereas before management would benefit from the fact their industry is growing faster than the broader market. On the third ask, in June 2023 the company announced an ambitious target and has committed to net zero Scope 1 and 2 emissions across its operations by 2032. Its target includes goals to reduce Scope 1 and 2 emissions by 42% by 2030 and to reduce Scope 3 use-phase emissions/terabytes by 50% by 2030, both from a 2020 base year. Its targets were approved by SBTi in 2021, and since then Western Digital has achieved nearly 15% absolute Scope 1 and 2 emissions reductions.

We look forward to sharing more successful EFI case studies in the future as our EFI target companies continue to make measurable progress against our asks.

Derek Deutsch, CFA, Managing Director, Portfolio Manager

Mary Jane McQuillen. Head of ESG, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. Performance source: Internal. Benchmark source: Standard & Poor’s. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here