")

Cass Information Systems, Inc. (NASDAQ:CASS) recently delivered a new recognition from a massive conglomerate that may bring new payment functionalities, and may bring new customers. I think that recent investments in technology, headcount growth, and the ability to deal with large amounts of data will most likely bring further net sales growth. Volatility in the interest rates and new technologies are, in my view, risks to consider, however I think that Cass currently trades a bit undervalued.

Cass Information Systems’ Business Model

Cass Information Systems offers comprehensive information processing and payment services to large companies in the United States. Its wide range of services ranges from freight invoice qualification to payment management, auditing, accounting, and transportation reporting.

Additionally, Cass excels in processing invoices related to telecommunications facilities and services, offering expense management solutions. The company holds various trademarks, such as FreightPay, Transdata, and Ratemaker, and patents for managing employee expenses. The company’s services include Touchpoint, Gyve, and WasteVision. In addition, it has specialized indices such as Cass Freight Index and patents to communicate expense management information.

Client diversification is a strength, not depending significantly on one client or group. This strategy, supported by innovations and intellectual properties, highlights the strength of the company’s business model in offering payment, qualification, and expense management services through multiple brands and specialized solutions.

Recent Agreement With FedEx (FDX) And Earnings

I think that it is a great moment for reviewing the Cass’ business model, mainly after its agreement with FedEx. The company was recognized as 2024 FedEx Certified Freight Bill Audit and Pay Provider. It means that Cass will be able to enhance its solutions to clients. Besides, other large companies may appreciate the relationship with FedEx, and may be willing to work with Cass. As a result, in my view, we could see improvements in future net sales growth.

Cass Information Systems, Inc. the leading global provider of freight audit and payment solutions, has been recognized as a 2024 FedEx Certified Freight Bill Audit and Pay Provider. This elite program recognizes freight payment providers that meet or exceed FedEx’s stringent standards for EDI capabilities, remittance quality, dispute management, and more. Source: Cass Information Systems Awarded Status as FedEx Certified FBAP Provider

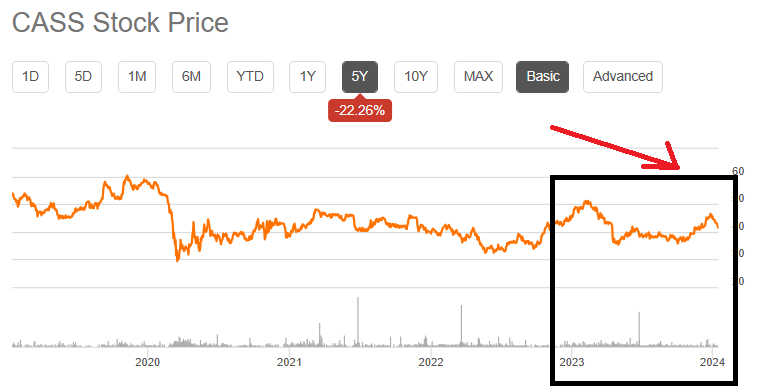

It is also worth taking a look at the recent earnings and price dynamics. The company reported better than expected revenue in Q3, but the EPS was lower than expected. Additionally, in 2023, the company noted lower than expected EPS and revenue, which may help explain the current stock price dynamics. Cass is currently trading at a lower price mark than that in 2020.

Source: Seeking Alpha Source: 10-Q

Stable Balance Sheet

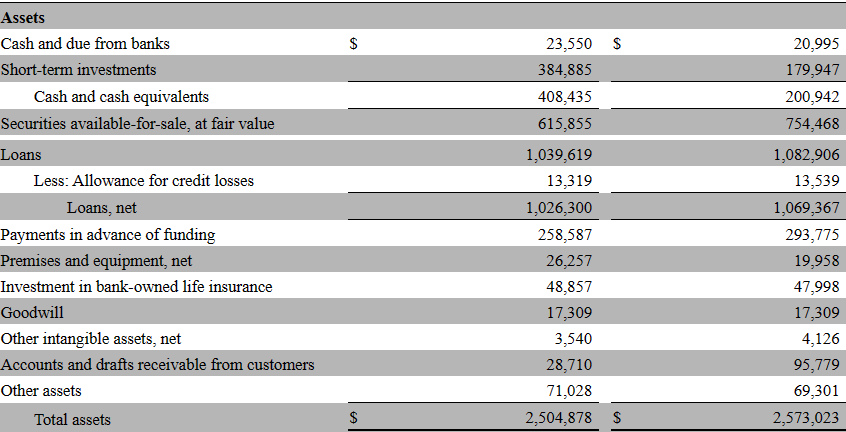

In the last quarter, Cass Information included cash and due from banks of about $23 million, short-term investments worth $384 million, and loans of about $1 billion. Payments in advance of funding were worth $258 million, with premises and equipment worth $26 million and total assets of about $2.504 billion.

Source: 10-Q

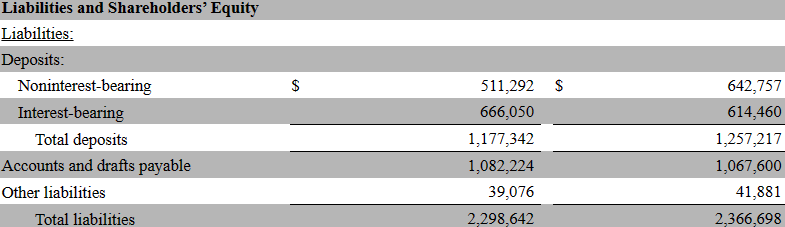

Liabilities include interest-bearing deposits of $666 million, total deposits of $1.177 billion, accounts and drafts payable of close to $1.082 million, and total liabilities of close to $2.298 billion. The asset/liability ratio is larger than 1x, so I would say that the balance sheet appears stable.

Source: 10-Q

Debt

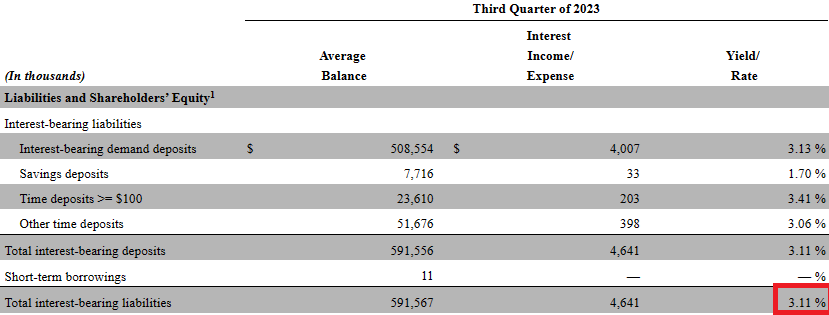

In the last quarterly report, Cass noted interest-bearing liabilities including interest rate close to 3.11%. I believe that it is worth keeping in mind the interest rate to assess the WACC.

Source: 10-Q

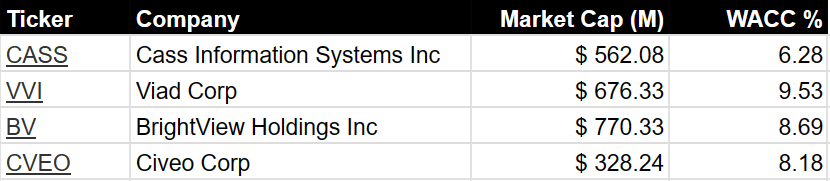

According to other investors and analysts out there, competitors report a WACC close to 6%-9.5%. Given the figures and the cost of debt, I think that a WACC close to 6% would be conservative.

Source: Gurufocus

Data Management Capabilities May Enhance Transaction Processing

Cass’ strategy focuses on different key points such as data acquisition, data management, and business intelligence. In my opinion, these competencies, supported by an integrated and efficient approach, allow Cass to deal with large volumes of transactions. The core competencies, strengthened through shared business processes, drive strategic business units. In my view, the ability to deal with large volumes will most likely facilitate links to large companies. In sum, these relationships could bring net sales growth and some economies of scale.

Higher Processing And Financial Fees Thanks To The Current Interest Rate

Given the recent increase in the interest rates in the United States, Cass benefited quite a bit. Even if the interest rates decline in the coming months, I would say that Cass may benefit for some time. In this regard, in the last quarter, both processing fees and financial fees increased as compared to the same quarter in 2022.

Source: 10-Q

It is also worth noting that Cass recently reported headcount growth and further investments in technology initiatives. In my view, companies that expect deteriorating business conditions do not hire more personnel or invest in new technologies. With this in mind, I would say that Cass remains optimistic about the future.

The Company recorded net revenue of $49.2 million during the three months ended September 30, 2023, up 4.3% from the three months ended September 30, 2022, primarily driven by higher processing and financial fees, along with rising interest rates which positively impacted net interest income. Operating expense increased 10.3% primarily driven by an increase in full-time equivalent employees and other expenses related to strategic investments in technology initiatives. Source: 10-Q

Cass’ Stock Repurchase Program Could Bring Demand For The Stock

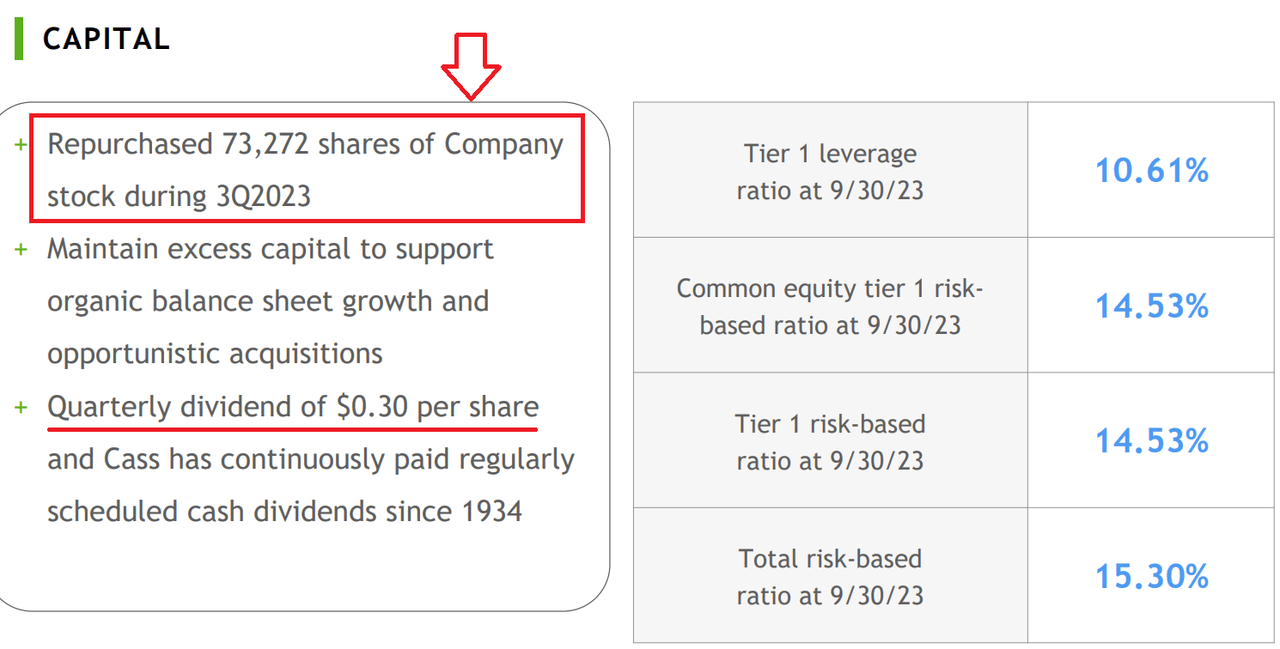

In the last quarter, Cass acquired close to 73k shares of the company, and also declared a quarterly dividend of $0.3 per share. Given the previous history of dividend payments that includes many decades and the stock repurchase program, we may see stock demand coming in the future. Most analysts may assume that Cass buys its own shares because they are cheap. In my view, companies do not usually buy their own shares when they are expensive.

Source: Quarterly Presentation

Competitors And EV/EBITDA Multiples

The company’s competition consists of several major competitors and numerous small freight bill auditing firms throughout the United States. Although they offer transportation payment services, few of these firms compete on a national level, focusing on competing on price, functionality, and service levels.

Through its Expense Management business unit, the company also competes with other companies in the United States that manage energy and waste bills, being one of the main providers in this area. Cass’s uniqueness lies in not being exclusively affiliated with any energy service provider.

Source: Seeking Alpha Source: YCharts

My Financial Expectations Based On Previous Assumptions And Stock Valuation

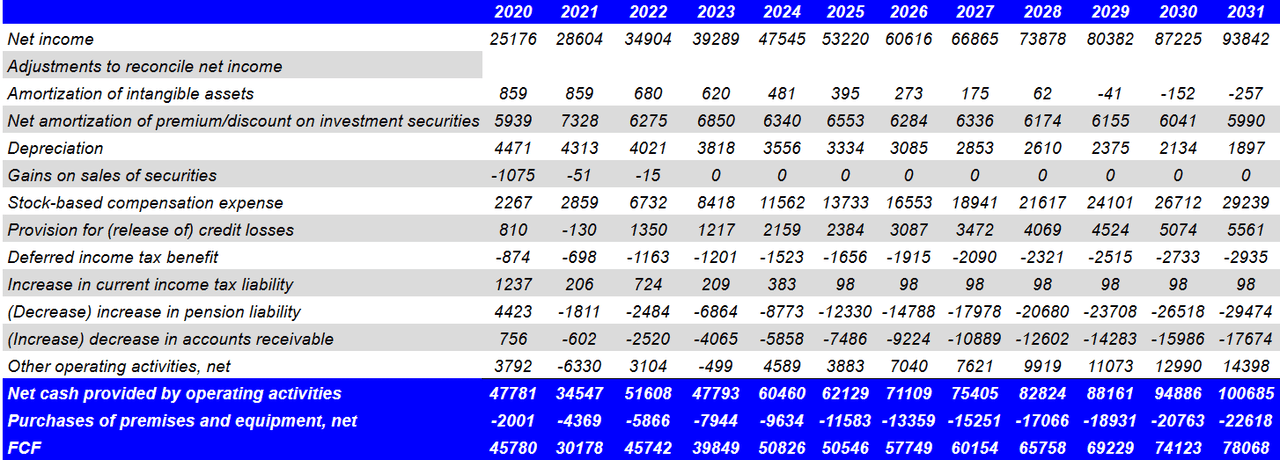

My expectations include 2031 net income of about $93 million, with depreciation of about $1 million, stock-based compensation expense worth $29 million, and provision for credit losses close to $5 million. Additionally, with deferred income tax benefit of close to -$3 million and changes in decrease in accounts receivable of close to -$18 million, I obtained net cash provided by operating activities worth close to $100 million. Finally, also assuming purchases of premises and equipment of -$23 million, 2031 FCF would stand at close to $78 million.

Source: DCF Model

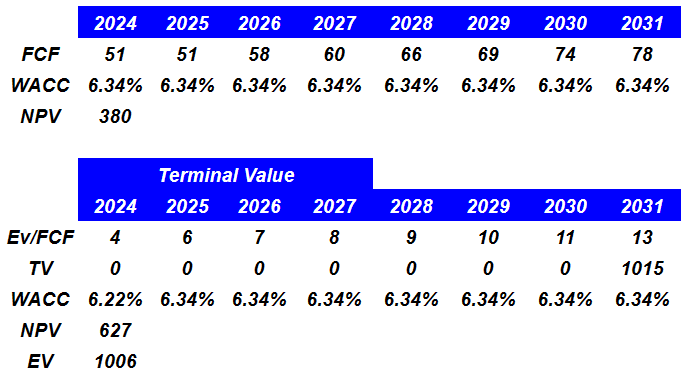

Now, if we assume a WACC of 6.34% and FCF ranging from $51 million to $78 million, the net present value would stand at $380 million. If we also include an exit multiple of 13x FCF, the NPV of future terminal value would stand at $627 million, and the enterprise value would not exceed $1.006 billion.

Source: DCF Model

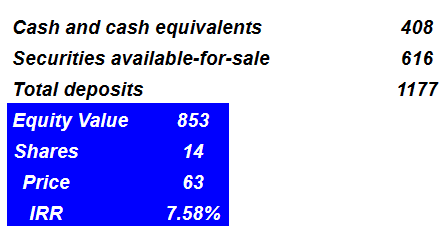

By adding cash and securities available for sale, and subtracting total deposits, the implied equity would stand at $853 million. The implied stock price would be $14 per share, and the internal rate of return would be not far from 7%-8%.

Source: DCF Model

Risks

Cass’ operations are significantly dependent on net interest income, being vulnerable to fluctuations in interest rates, government policies, and economic conditions. Disintermediation, caused by rate volatility, could negatively affect the company. As a result, I think that fees could lower, which may bring lower FCF margins and FCF decrease.

In addition, there is a risk coming from customers not paying their obligations with Cass. If the company has to report allowance for credit losses, I would be expecting a decline in profitability. Stock owners may decide to sell their shares as their expectations about the future of the business may lower. In sum, the stock price could decline.

Although the Company regularly reviews credit exposure related to its customers and various industry sectors in which it has business relationships, default risk may arise from events or circumstances that are difficult to detect or foresee. Under such circumstances, the Company could experience an increase in the level of provision for credit losses, delinquencies, nonperforming assets, net charge-offs and allowance for credit losses. Source: 10-k

The introduction of new products and technologies by competitors as well as changes in industry standards and practices could render Cass’ services obsolete. Besides, failure to adopt or develop new technologies could result in loss of customers, which may also lead to lower net sales growth and FCF growth.

My expectations with regard to net sales growth, FCF margins, and trading multiples could also be wrong. There are analysts out there expecting net income growth in 2024 and 2025. Their expectations may also be too optimistic. As a result, in the future, lower earnings or lower FCF than expected may bring stock price declines and a reduction in the demand for the stock.

The company also has some exposition to declining fuel prices due to its freight and shipping customers. Lower oil price could lead to lower net sales growth and lower net income growth. In this regard, Cass noted the following in the last annual report.

Lower oil prices can also result in lower gas and fuel prices, negatively affecting the dollar amounts of the invoices that Cass processes for its freight and shipping customers. A decline in oil prices could have an adverse effect on the Company’s revenues and could significantly impact its results of operations. Source: 10-k

My Conclusion

Cass Information exhibits a diversified business model, supported by trademarks, patents, and a diverse customer base with large partners like FDX. In my view, strategy focused on data acquisition and management as well as business intelligence will most likely bring more demand for clients dealing with large amounts of data. Besides, recent stock repurchases and dividends could also bring demand for the stock, and enhance the stock price. There are obvious risks associated with lower interest rates, and new technological developments are factors to consider. With all that being mentioned, I think that Cass currently trades a bit undervalued.

Read the full article here