")

Introduction

It’s time to do one of my favorite things: discuss Extra Space Storage (NYSE:EXR).

As much as I love REITs, so far, I have only bought two of them. Both are self-storage REITs.

Although one could make the case that owning two self-storage REITs in a concentrated 20-stock dividend portfolio may not be the best way to diversify, I have two things to say:

- I am not done buying REITs, as I have a number of them on my watchlist, including residential and industrial real estate.

- Although buying self-storage goes against my focus on buying companies in industries with high entry barriers (another rule I’m breaking here), I am in love with this industry for a number of reasons.

Related to point two, the other day, I found research from the Lindsey Self Storage Group, which gave us ten reasons why self-storage REIT estate is superior.

Allow me to paraphrase the ones that I find most important:

- Quick Eviction Process: Self-storage allows landlords to lock out non-paying tenants within 5-6 days, a faster process compared to other real estate investments. Especially in residential housing, landlords in some states are limited when it comes to evictions.

- Flexible Lease Terms: Self-storage leases are for 30 days, automatically renewable, providing advantages like quicker rent increases and easier eviction of undesirable tenants.

- High Depreciation: Self-storage investments offer high depreciation, protecting income from taxes on other investments.

- Low Operating Costs: Operating costs for self-storage are lower compared to other real estate investments, typically around $3.00/sq. ft, including all expenses.

- Minimal Personnel Requirement: Self-storage facilities require fewer personnel, with larger sites managed by two people and even smaller facilities operated by one full-time employee.

- Universal Need: Self-storage caters to a broad spectrum of needs from individuals, companies, or businesses in both good and bad economic times, making it a versatile investment.

With that said, my most recent article on EXR was written on November 10, when I went with the title “I’m Not Done Buying 5.5%-Yielding Extra Space Storage.”

Since then, EXR shares have rallied 25%, including dividends, beating the impressive 10% return of the S&P 500.

In this article, we’ll discuss why EXR was able to outperform the market, what to make of new developments in the self-storage industry, and how I’m dealing with the changed risk/reward in light of company and industry/economic developments.

So, let’s get to it!

A Fed-Fueled Rally

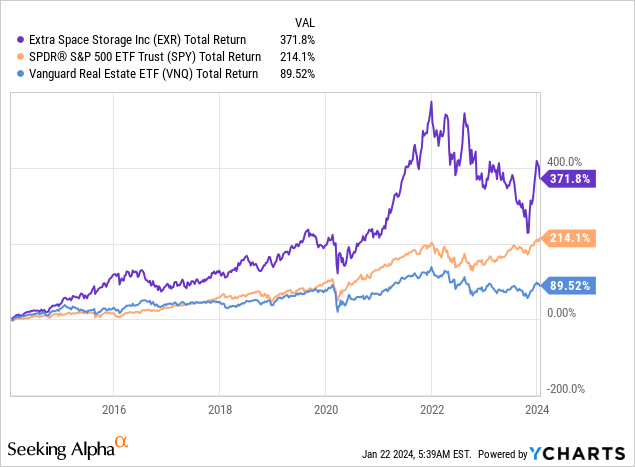

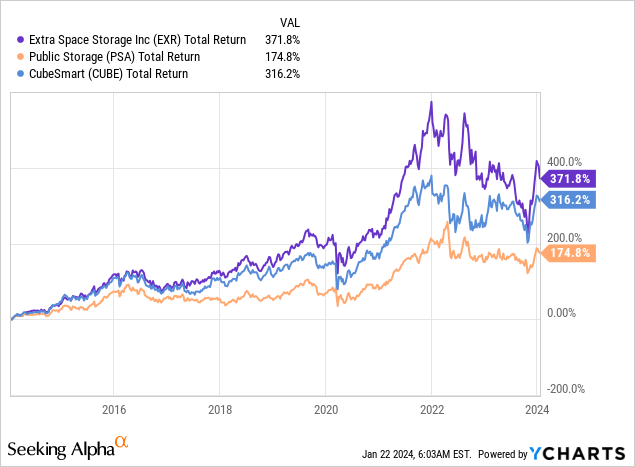

Including dividends, EXR has returned 372% over the past ten years, beating the 214% performance of the S&P 500 by a wide margin. The Vanguard Real Estate ETF (VNQ) returned just 90%, which is one of the reasons why I am so very picky when it comes to buying real estate investment trusts.

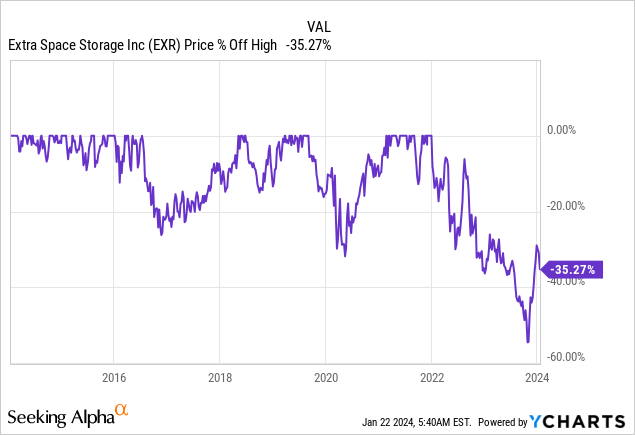

Unfortunately, as the chart above already suggests, this return did not happen without some major bumps in the road.

The chart below confirms that investors have been through three major sell-offs over the past ten years. The worst sell-off is the most recent one.

Even after rising 45% from their 52-week lows(!), EXR shares are still 35% below their all-time high, which shows just how volatile America’s largest self-storage operator has become.

Essentially, there are three major reasons for that:

- Self-storage, in general, is a cyclical asset class that relies on consumer and housing health.

- Real estate stocks are very sensitive to interest rates, as higher rates make it much harder to expand using debt and refinance maturing debt.

- Extra Space bought Life Storage in a $12.7 billion deal. Although EXR has a top-tier M&A track record, this deal added more uncertainty.

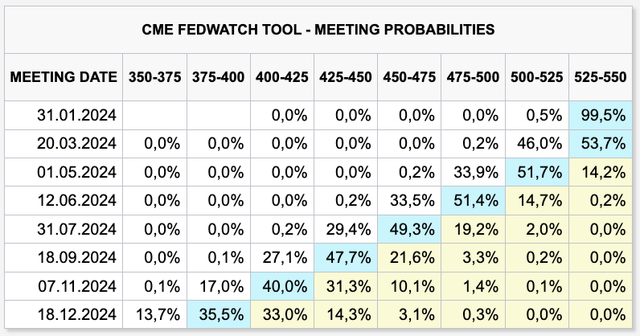

With that in mind, the reason why EXR’s stock price started to fly is the decision of the market to price in no less than six rate cuts for 2024!

CME Group

Market participants now expect the Fed to cut rates to the 3.75% to 4.00% range in December, making it one of the steepest (potential!) easing cycles without an expected recession since the Fed was founded.

Unfortunately, I am not convinced yet that this rally is sustainable.

For example, core inflation is still close to 4%. It is unlikely that central banks start cutting aggressively until they are forced to.

The other day, I tweeted that San Francisco Fed President Mary Daly came out saying it may be “premature” to believe that rate cuts are around the corner, as the Fed wants to see more evidence that inflation is on a consistent path to 2%.

The keyword here is “consistent,” as the Fed is very afraid of a second wave of inflation the moment it starts easing.

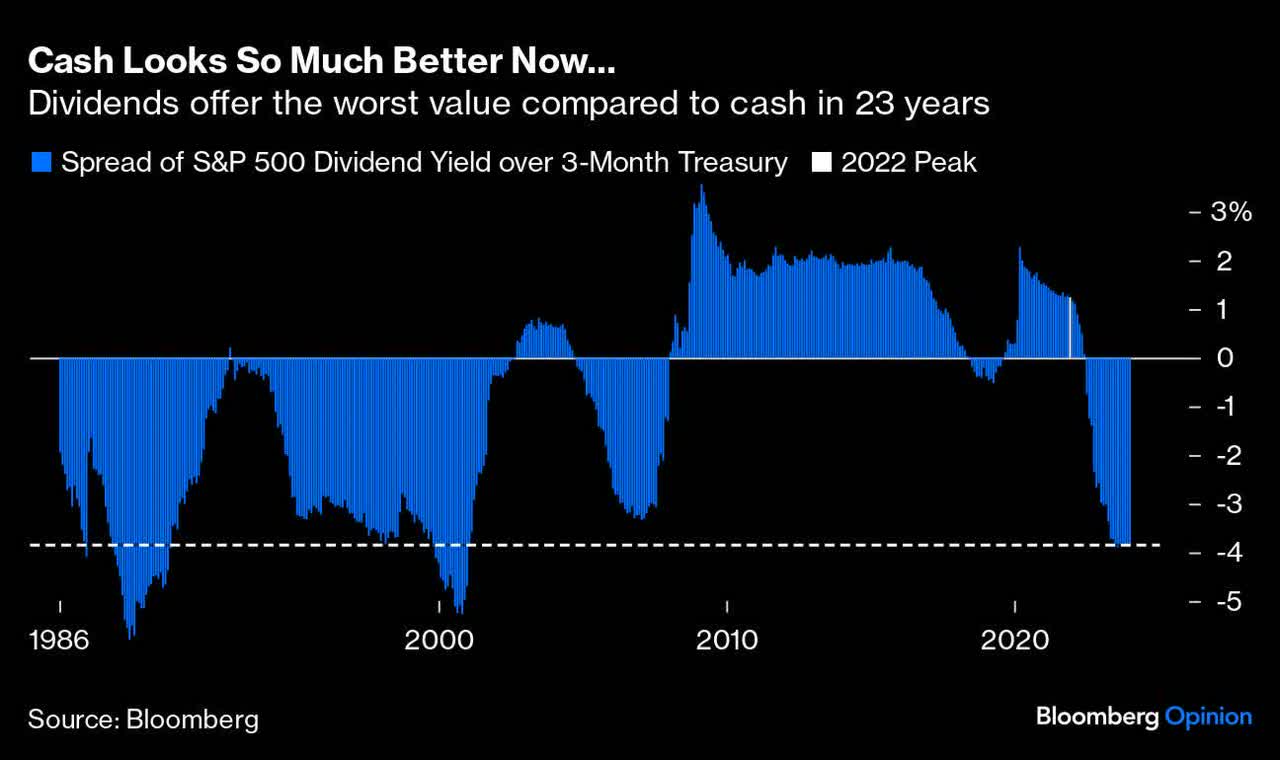

Furthermore, we’re now at a point again where bonds are more attractive than stocks if rates do not keep dropping.

Bloomberg

In other words, the risk/reward has gotten a bit poor again, which is why I am covering EXR again.

After all, I want to buy more, and I want it to do at even better prices.

Strength Amid Headwinds

As the chart below shows, the three biggest self-storage operators in the United States (accounting for 29% of the entire market) have lost momentum in early 2022.

It’s no surprise that they lost momentum back then, as they started to encounter a mix of headwinds, including rising rates and weakening housing market fundamentals.

This has resulted in a weaker self-storage market as well.

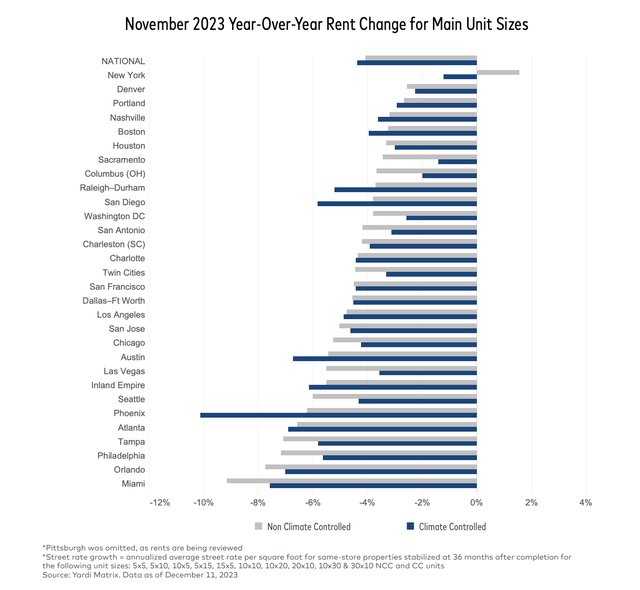

As reported in the Yardi Matrix December 2023 Self-Storage report, the industry grapples with challenges stemming from the housing market, as soaring housing costs and stagnant incomes contribute to one of the least affordable housing markets in the past 30 years.

This situation pressures home sales, affecting storage occupancy and putting downward pressure on street rates.

Despite national asking rate growth remaining stable, street rates continue to decline annually and sequentially.

Meanwhile, the housing slowdown has pushed occupancy back to pre-COVID levels, especially in Sun Belt markets that previously benefited from COVID-era migration.

Annual street rate growth remains negative, with the average annualized same-store asking rent per square foot dropping by 4.2% nationwide.

However, despite the challenges posed by the slow housing market, annual street rate growth remains stable.

Same-store national street rates for combined NCC (non-climate controlled) units and CC units show declines of 4.1% and 4.4% year-over-year, respectively. The stability in rent declines indicates that, while storage demand is affected, the situation is not worsening.

Yardi Matrix

In light of these challenges, EXR stands strong.

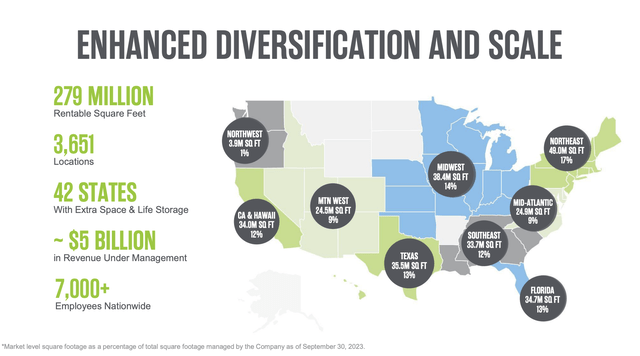

In its most recent 3Q23 quarter, the company reported a number of tailwinds, including the successful merger with Life Storage, adding over 1,200 stores to its portfolio, and over 2,300 new team members.

It now owns roughly 280 million of rentable square feet, which translates to more than 4,800 NFL football fields!

This massive footprint also comes with fantastic diversification, as it has no market with more than 17% exposure.

The company has significant exposure in markets with subdued supply, like California and the Northeast, and significant exposure in Sunbelt growth markets.

Extra Space Storage

Furthermore, the combined portfolio, now totaling 3,651 stores, is expected to enhance diversification, stability, and operational efficiencies for both property-level and external growth.

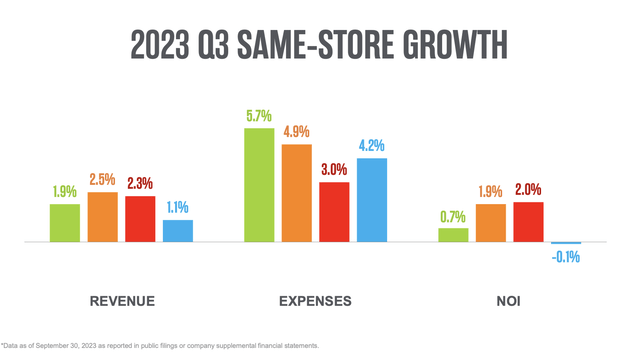

In the third quarter, revenue growth for the Extra Space same-store pool flattened, but the 1.9% same-store revenue increase exceeded expectations.

This growth was attributed to high average occupancy of 94.4%, as existing customer behavior remained strong, with a solid length of stay, muted vacates, and acceptance of rate increases.

However, expenses came in higher than estimated, primarily due to unexpected property tax increases.

This offset the revenue outperformance and resulted in a modest miss in the same-store net operating income (“NOI”).

Extra Space Storage

This was also one of the reasons why the stock did so poorly before the Fed-fueled rally brought new hope.

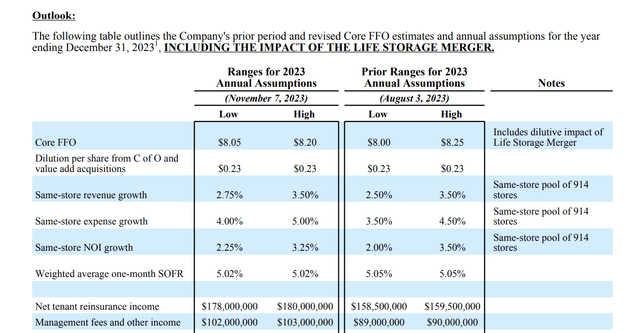

As a result, the core FFO (funds from operations) range for 2023, including the short-term dilutive impact of the Life Storage merger, was tightened to $8.05 to $8.20 per share, maintaining the previous midpoint.

Extra Space Storage

This range accounts for the overall performance in line with expectations and the integration of Life Storage remaining on track.

The company is also upbeat about its future, as it believes it has a much stronger operating platform through the Life Storage merger, positioning the company for outsized future growth.

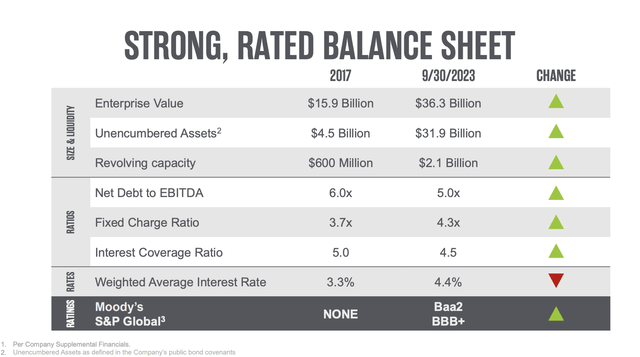

It also has a top-tier balance sheet.

With the merger, the company assumed $2.4 billion in Life Storage’s publicly traded bonds at the same coupons and maturities. S&P Global upgraded the company’s credit rating to BBB+ after the merger based on promising future interest expense savings and operational synergies.

Extra Space Storage

BBB+ is just one step below the A range, giving EXR one of the best balance sheets in the REIT sector.

This also bodes well for the risk/reward.

The EXR Risk/Reward

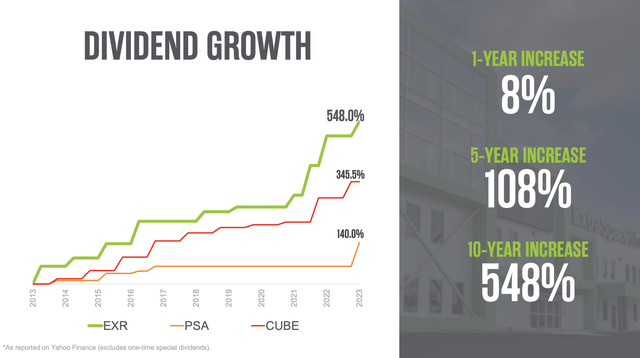

One of the biggest benefits of owning EXR is its dividend. The company currently pays $1.62 per share per quarter, which translates to a yield of 4.4%.

On February 16, 2023, this dividend was hiked by 8%. The five-year dividend CAGR is 14.0%, which is one of the highest numbers in the REIT space.

Going back to 2013, the company has hiked its dividend by roughly 550%, outperforming both of its largest peers by a wide margin.

Extra Space Storage

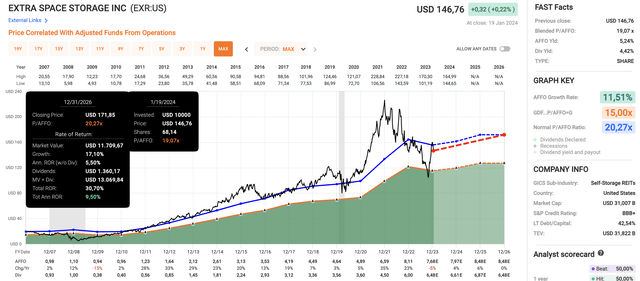

Furthermore, this year, the company is expected to generate $7.97 in adjusted FFO (“AFFO”), which puts the payout ratio at 81%.

Although I do not expect dividend growth to remain close to 10% in this environment, there are reasons to be upbeat, as the stock has an implied annual return of roughly 10%.

Using the data in the chart below.

- This year, AFFO is expected to increase by 4%, potentially followed by 6% growth in 2025 and 0% growth in 2026.

- EXR currently trades at a blended P/AFFO ratio of 19.1x, which is a bit below its long-term normalized multiple of 20.3x.

- Combining its 4.4% dividend yield, a return to 20.3x AFFO, and expected AFFO growth rates, EXR has an implied annual total return of 9.5%.

FAST Graphs

Going back to 2007, EXR has returned 14.5% per year.

With all of this in mind, EXR is now my sixth-largest investment. It briefly was my second-largest holding before losing momentum.

As such, I am not in a huge need to buy more EXR, as I try to keep my portfolio balanced.

However, as I am convinced that EXR is one of the best dividend stocks on the market, I am eagerly looking to press the Buy button again.

I hope to see a decline toward $130 per share again, which I believe could be triggered by the market’s realization that we may not get a steep central bank easing cycle after all.

My EXR rating remains a Buy rating to reflect its long-term potential.

Takeaway

In a market with tremendous uncertainty, Extra Space Storage stands strong, showing resilience amidst challenges.

Despite sector headwinds and a slow housing market, EXR’s strategic moves, including the successful Life Storage merger, have fortified its position.

With a massive and diversified portfolio, the company navigates evolving market dynamics.

While EXR faces short-term challenges, its long-term potential, balanced portfolio, and impressive dividend track record make it a compelling investment.

As the market fluctuates, EXR remains a standout choice for those seeking stability and growth in the REIT sector.

Read the full article here