")

The following segment was excerpted from this fund letter.

Pershing Square Holdings (OTCPK:PSHZF)

Pershing Square Capital Management (PSCM), the investment management company established by William A. Ackman in 2003, has always had a significant profile, arising from its methodology and the highly confident nature of its founder. In the nine years between 2004-2012 PSCM compiled a net return of 20.4% per annum. Believing – quite rightly – that the concentrated style of investment undertaken by the firm would benefit from permanent, rather than semi-open- ended capital, Pershing Square Holdings (PSH) was launched at end 2012 and IPO’d in October 2014 at a price of $25 per share.

PSH is especially interesting having compiled a strong stretch of performance since staring into the abyss in 2016-17, but still trading at above a 30% discount to NAV, despite a strong management shareholding, consistent share buy-back program and detailed presentations.

E72DT has a small shareholding in PSH in the belief that the discount can be further narrowed and NAV grow as a result of catch-ups in two of PSH’s “lagging” investments, potential for the vehicle to be “onshored”, as well as the over-riding motivation of management company profits and personal stockholdings. We acknowledge some of the easy money has been made but believe the next 2-3 years may provide a changed structure which will serve to close up the discount to NAV as well as growing asset backing.

As has been the case with many managers who have not previously run closed end, publicly listed vehicles, the additional public and regulatory attention seemed to play with Ackman’s psyche. From 2015 – 2018, PSH racked up four successive down years losing a cumulative 34.4% of NAV, against an S&P500 index return (not benchmark) of +32% over the same period.

So what happened? In many ways, Ackman hadn’t lost his expertise but had started to believe his own publicity and became extraordinarily distracted from the core business. In December 2012, at the Sohn Conference Foundation, Ackman presented for three hours on the multi-level sales business Herbalife (HLF), where Pershing Square had initiated a significant short position. This was followed by an unsavoury, unscheduled live debate on CNBC1 between Ackman and Carl Icahn, calling in and disclosing a long position.

Ackman also willingly participated in a documentary “Betting on Zero”2 effectively documenting evidence against HLF. Over time, whilst Ackman may have been fundamentally correct about some aspects of HLF, Pershing Square misjudged HLF’s willingness to repurchase its own shares with debt – funded by a strong cash flow (at the time) – together with the fact that other hedge funds smelled blood with Ackman caught in a short squeeze as the share capital contracted and free float diminished aided by Icahn and others.

The beginning of the end of the HLF short trade is plain to see in PSH Q3 2017 quarterly report3 and the five-year escapade, which was imported into PSH, finally concludes at end February 2018.

In 2015, the all-consuming significant investment in Valeant Pharmaceutical4 was made; Ackman’s (and CEO Mike Pearson) attempts to fight back against the claims of Valeant acquiring other companies and therapeutics to then cease the R&D spend and ratchet up prices of lesser known drugs were increasingly discredited.

The final nail in the Valeant coffin was the agreed revelation5 that Valeant had engaged in improper revenue recognition via a subsidised mail order pharmacy, Philidor. For an investment professional known for enormously detailed presentations on investee companies6, this was embarrassing indeed. Even worse, the whole messy saga was laid out in a Netflix documentary, “Drug Short”7 where short-sellers who successfully bet against Valeant illustrated the type of skills expected of a credentialled player (and insider) such as Ackman, making him appear especially foolish and captured by management. Ackman exited Valeant with a $3billion loss in March 2017.

The combination of poor returns and adverse publicity took its toll on PSCM. In October 2014, PSCM held assets under management of US$18billion of which US$6.3bn (~35%) was PSH8; by end 2017, firm assets are down to US$9.3billion and PSH $4.24bn (~46%).9

In January 2018, Ackman took decisive action in an attempt to prevent the whole show falling into the abyss, with significant cost reductions and a refocus of his own role to concentrate on research and ideas. This was swiftly followed in March 2018 by a $300million tender (9.5% of shares being 22.3million at a price of $13.47/share) to buy back PSH shares after an attempt by Ackman personally to do so was rebuffed by regulators. However, shareholders voted to remove the 4.99% shareholder restriction cap on PSH in Q1 2018, and Ackman plus other members of the investment management team embarked on a significant buying spree. Between May & October 2018, Ackman acquired 23.7m shares at an average price of $15.01 to bring his holding to 39.9m shares or 18%; the entire team held 20% of PSH stock.

As with other (a carefully chosen adjective because there are not many) fund management turnarounds, the upturn did not commence immediately with PSH returning -0.7% in 2018 largely as a result of poor equity conditions. However, the realignment of management objectives with those of the PSH entity has been significantly rewarded in the past five years with NAV/share climbing from $17.30 at end 2018 to the end 2023 figure of $65.04.10

However, in three of the five years, performance has been aided by well-structured macro- economic bets, notably:

-

- 36.6% addition from credit default swaps being triggered due to COVID in CY2020;

- 7.7% accretion from interest rate swaptions in CY2021;

- 14.3% accretion from interest rate swaptions in CY2022; and

- Likely significant gains from interest rate positions in CY2023.

Hence, only the stunning 58.1% return in CY2019 was fully comprised of the outturn from stock picking.

The current portfolio is dominated by only eight positions (Alphabet is held in both Class “A” and Class “C”) forms together with the two small positions in Fannie Mae and Freddie Mac; Universal Music Group (UMG.AS) is held directly and as part of a special purpose vehicle and is the largest component of the ~$14billion portfolio valued at ~$3billion.

PSH only publish the exact portfolio twice per annum and there are significant derivative positions on occasions which can add or detract from performance. We follow the portfolio from PSCM’s 13-F filings with the SEC given that PSH accounts for some 87% of the domestic US holdings. There will be an update to shareholders on 8 February 2024 and the 2023 Annual Report will be available at end March 2024.

Our best estimates11 of the NAV of $12.06billion at 31 December 2023, using some reverse engineering, are as follows:

|

Value ($mn) |

Performance 2023 |

$mn |

||

|

Alphabet (x2) |

1,679 |

+58.3% |

Cash, receivables, other |

1,000 |

|

CP Kansas City |

1,038 |

+6.0% |

||

|

Chipotle |

1,897 |

+64.8% |

Trade liabilities |

(203) |

|

Hilton Hotels |

1,632 |

+44.1% |

Deferred tax liability (HHH) |

(85) |

|

Howard Hughes Corp |

1,403 |

+11.9% |

Performance fee |

(255) |

|

Lowes |

1,368 |

+11.7% |

Bonds at par |

(2,609) |

|

Restaurant Brands |

1,587 |

+20.8% |

NET OTHER |

(2,152) |

|

UMG (inc SPV attribution) |

3,298 |

+18.6% |

||

|

Other |

302 |

NET ASSETS |

12,062 |

|

|

TOTAL PORTFOLIO |

14,213 |

Per share |

$65.04 |

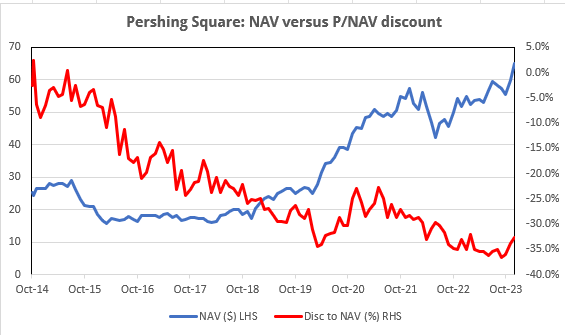

After a lengthy period underwater – and giving shareholders a little of a free ride – PSH’s NAV is back over its prior high water mark (HWM) at 31 December 2023 with NAV of $65.04 against a HWM of $56.23, thereby triggering the 16% performance fee in addition to the standard 1.5% ongoing fees.

But, as the above chart clearly shows, improved NAV performance does NOT translate into a narrowing discount to NAV of any consequence. Bluntly, this is the big issue for Ackman to solve – because there is over $775million12 in it: just for him

Where to from here? Why do we still Hold?

It is clear to most, and there have been several clues given by Ackman himself, that Ackman/PSCM are wedded to the “permanent capital” structure. PSH’s assets under management of $14.7billion leave only $2.1billion with other investors in the “core” strategy, and the residue of the firm’s managed assets (~$1.5billion) are in special purpose vehicles such as PS VII Master which holds ~76million UMG shares and of which PSH itself owns 28%13. So PSCM has nearly fully converted to this format.

The logical next step is to turn PSH into an operating company – which would fulfill Ackman’s wishes of a “Berkshire” type structure14 – but would require the “onshoring” of PSH. That would only be possible by PSH becoming an operating company15 with (say) 40% of the assets being public investments. This is not going to happen overnight, but moves towards it may be seen in the further increase in shareholding of Howard Hughes Holdings to 37.6% of the property company16. Even a full acquisition of HHH would likely not satisfy the onshoring idea since, on a pro-forma basis, securities would still be ~54% of total assets of ~$21billion.

The calculation above assumes a sale of Chipotle (CMG), which we view as being a possibility given the forward P/E of 41x; Ackman has shown a willingness to divest retail food franchises of strength in the past through the sale of Starbucks (SBUX) in January 2020. In the meantime, PSH gives us another discount exposure – in tandem with Bolloré (OTCPK:BOIVF) and Vivendi (OTCPK:VIVEF) – to UMG (OTCPK:UMGNF).

So, is an investment in Howard Hughes Holdings (HHH) desirable with its equity market capitalisation of $4.3billion and enterprise value estimated at $9billion (subject to working capital) desirable?

Arguably, the investor issue with issue with HHH is the complexity of the company – which precludes a detailed analysis in this report – with its mix of completed developments, multiple projects under construction, and an enormous landbank in five desirable locations from a demographic and tax standpoint: Houston, Phoenix, Las Vegas, Maryland and Hawaii. Only four sell side analysts seem to cover the company. HHH has been heavily tarnished by the Seaport development in downtown Manhattan, which obviously suffered during COVID, but in the last quarter was the subject of a $700m impairment charge. That – of course – was aligning an appropriate valuation ahead of a hoped for spin-off in 2024, to leave the main company in a clean position.

E72DT has a holding in another “condominium” rental/industrial/commercial development company centred in Washington DC and its environs: FRP Holdings (FRPH), which is a family controlled entity but also has the benefit of a 90% margin aggregates royalty. The shares were moribund for some time but saw greater interest once the residential developments were stabilised – in FRPH’s case with significant rentals. We suspect HHH is in a similar position when investors can identify hard asset value through cash on completed sales or a place a firm yield on rentals.

HHH does fit PSH’s desire for attractive long-term returning assets, of which UMG is arguably its best. PSH is a modest 1.7% position in the E72DT portfolio – sadly given its recent strong performance – but we continue to expect positive evolutions – over time. Our main concern is ensuring the largest shareholder and manager keeps his eye on the ball amidst other distractions. The past five years have proven his intellect and performance capability when disciplined.

|

Footnotes 1 25 January 2013 (https://www.youtube.com/watch?v=6QWZbxeJd6g) 2 “Betting on Zero” released 14 April 2016 (Zipper Brothers Films, Biltmore Films) 3 Q3 2017 4 Now Bausch Health Companies (NYSE: BHC) 5 SEC Press Release 31 July 2020 “Pharmaceutical Company and former Executives Charged with misleading financial disclosures” 6 Examples: 50 slides on Howard Hughes Corp (Ira Sohn Conference – 8 May 2017); 2’44” 128 slide presentation regarding UMG (https://www.youtube.com/watch?v=BpeHWiRuu2k); 43 slides on Starbucks (“Doppio” 9 October 2018) 7 Episode 3, S1 of the “Dirty Money” series on Netflix (2018) 8 PSH Monthly Performance Report October 2014 8 PSH Monthly Performance Report December 2017 10 PSH Monthly Performance Report December 2023 11 We could be wildly wrong here. 12 21% of 185 million shares x (NAV – price) 13 PSH owns ~105.3million UMG shares directly 14 Interview with Fifth Avenue Synagogue May 2021 (https://youtu.be/mU0DrHB6u9s) containing, for example “If you follow him (Buffett) from the mid-1950s to the late 1960s he managed what is best described as an activist hedge fund and then he gave his investors the option in effect… he basically said look I’m going to return all the assets but if you’d like you can go along with me in a company called Berkshire Hathaway. Sort of merged his hedge fund into what became this… what was a textile company at the time, and became a conglomerate that he’s managed over time. The benefit… what was interesting is he gave up the right to receive a share of the profits in exchange for permanent capital which tells you how he valued it, or how highly he valued it. We started about 12 years in at Pershing Square. We launched a public entity, structured as a European closed-end fund with a business plan to get to the same place ultimately as Buffett.” 15 Hedge funds cannot be listed on US public exchanges 16 18,851,725 shares held of issued capital of 50,078,903 Copyright and Disclaimer ©Other than material being the property of its respective owners, this presentation is copyright 2023 East 72 Management Pty Ltd. All Rights Reserved. You may not reproduce parts of this work without permission, which can be sought by email, but you are free to distribute the work in its entirety with full attribution. This communication has been prepared by Andrew Brown and East 72 Management Pty Limited (E72M) (ACN 663980541); E72M is Corporate Authorised Representative 001300340 of Westferry Operations Pty Limited (AFSL 302802) of which Andrew Brown is a Responsible Manager. While E72M believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. E72M and its related companies, their officers, employees, representatives and agents expressly advise that they shall not be liable in any way whatsoever for loss or damage, whether direct, indirect, consequential or otherwise arising out of or in connection with the contents of an/or any omissions from this report except where a liability is made non-excludable by legislation. Any projections contained in this communication are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of E72M and therefore may not be realised in the future. This update is for general information purposes; it does not purport to provide recommendations or advice or opinions in relation to specific investments or securities. It has been prepared without taking account of any person’s objectives, financial situation or needs and because of that, any person should take relevant advice before acting on the commentary. The update is being supplied for information purposes only and not for any other purpose. The update and information contained in it do not constitute a prospectus and do not form part of any offer of, or invitation to apply for securities in any jurisdiction. The information contained in this update is current as at 31 December 2023 or such other dates which are stipulated herein. All statements are based on E72’s best information as at 31 December 2023. This presentation may include officers and reflect their current views with respect to future events. These views are subject to various risks, uncertainties and assumptions which may or may not eventuate. E72M makes no representation nor gives any assurance that these statements will prove to be accurate as future circumstances or events may differ from those which have been anticipated by the Company. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here