")

Generally speaking, experiencing revenue growth is a positive thing for companies. However, it doesn’t always mean that bottom line improvement will follow. And at the end of the day, it’s the profits and cash flows of an enterprise that determine its value, not the amount of sales it brings in. A good example of a divergence between growth and profitability can be seen by looking at automotive retail firm Sonic Automotive (NYSE:SAH). Back in October of 2022, I wrote a bullish article about the company because of how cheap the stock was. Some of the firm’s financial results were less than ideal. But that was acceptable given how affordable units were at the time. After rating the company a ‘buy’, the stock went on to achieve upside for shareholders of 25.9%. For a little over a year, that is a fantastic amount of appreciation. Having said that, the upside did fall short of the 35% seen by the S&P 500 over the same window of time.

The problem, I believe, has not to do with anything from a growth perspective. And it is true that shares are very attractively priced at this point in time. In fact, they are amongst the lowest in this market. Having said that, profits and cash flows have pulled back since the end of 2022. The good news is that management is working to rectify these issues. And if they do, the end result for investors could be very positive. Because we have yet to see meaningful progress on this as of yet, I have decided to keep the business rated only a ‘buy’. But given how cheap the stock is, I could become even more bullish on it if bottom line results start to improve materially.

The picture has changed

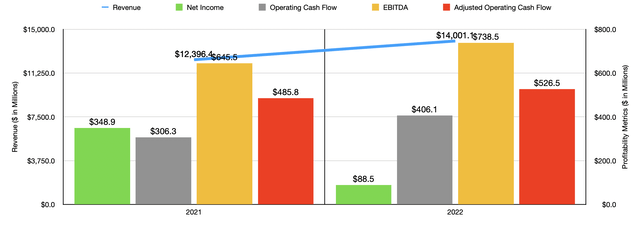

If you were to assess the investment worthiness of Sonic Automotive by only its annual results, you’d be perplexed as to why the firm has fallen short of the broader market. Revenue in 2022 came in at a rather strong $14 billion. That’s 12.9% above the $12.40 billion generated in 2021. When it comes to the new vehicles the company sells, the number of units dropped slightly from 103,486 to 103,283. However, revenue per new unit sold jumped around 12% from $49,456 to $55,402. This is not surprising if you have followed the automotive retail space closely. Overall unit sales were down compared to the year prior when it comes to the US market at least. Automotive strikes, combined with supply chain issues when it comes mostly to things like microprocessors, caused unit sales to drop and prices to rise.

Author – SEC EDGAR Data

On the used retail side, there was a much larger drop of around 6% when it comes to number of units sold. They declined from 183,292 to 173,209. However, this did not stop revenue per unit from increasing. It jumped around 20% from $26,609 to $31,842. This was accompanied by a 4% decline in wholesale vehicle units sold from 36,795 to 35,323. And in this case, revenue per unit jumped around 38% from $9,980 to $13,727. Driven largely by three $120.4 million of impairment charges, profits for the company declined from $348.9 million to $88.5 million. However, as the chart above illustrates, all of the other profitability metrics for the enterprise improved from 2021 to 2022.

Author – SEC EDGAR Data

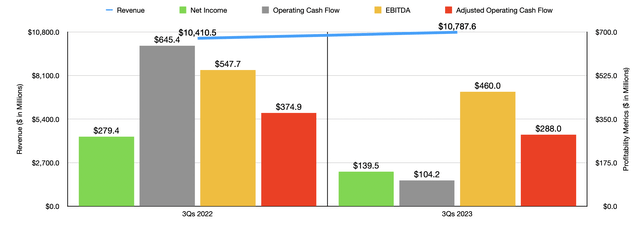

That picture started to change when we entered into the 2023 fiscal year. Revenue continued to increase year over year, climbing from $10.41 billion in the first nine months of 2022 to $10.79 billion in the first nine months of last year. New unit sales actually increased during this time, and revenue per new unit rose modestly. But the cost of procuring these vehicles rose even more significantly, causing gross profit per new unit to drop about 26%. On the used vehicle side of things, the company reported a 4% increase in volume sold. In this case, revenue per unit dropped by about 8%. And that, combined with a higher cost of procurement, sent gross profit per unit down around 25%. As a result of these factors, net income plummeted from $279.4 million to $139.5 million. If it were just that, it would be understandable. But as the chart above illustrates, all three cash flow metrics that I looked at also worsened year over year.

Last year, management acknowledged that some of the company’s problems related to the EchoPark segment of the company, which focuses largely on the sale of used vehicles. In June of 2023, the company indefinitely suspended operations at eight of those locations, as well as 14 related delivery and buy centers. This was followed up by some other asset closures later on in the year. Management has also worked hard to get the total days worth of supply at this unit down to between 30 and 40. It’s now down to 37 compared to the 57 that it was at the same time one year earlier. The problem with the unit, in my opinion, is that when you’re dealing with low priced vehicles, margins are already tight. Management pitches the segment as a place where consumers can get used vehicles priced at up to $3,000 below market value. For context, for the 2022 fiscal year, used vehicle sales and wholesale sales combined accounted for 43% of the company’s revenue but for only 8% of its gross profit. This is a radically different strategy than the luxury brands that comprise about 52% of the company’s revenue and the import brands that make up 18%.

For 2023, the picture was looking even worse. It is true that the largest of the company’s segments, the Franchised Dealerships segment, was experiencing weakness on the bottom line year over year, with segment profits dropping from $472.2 million to $357.2 million. But it was undoubtedly the used vehicle side of the company, the EchoPark segment, that was in the red. It went from a segment loss of $100.6 million in the first nine months of 2022 to a loss of $116.5 million the same time of 2023. Even while management continues to cut costs and focuses on growing sales associated with the Franchised Dealerships part of the business, it plans to get to EBITDA breakeven for the troubled EchoPark segment by the first quarter of the 2024 fiscal year. If they can achieve that, then upside potential could be rather meaningful seeing as how management views the addressable market opportunity as representing about 2 million vehicle sales each year.

Author – SEC EDGAR Data

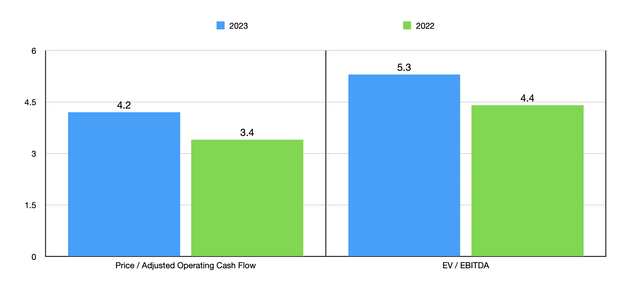

We don’t really know what to expect for the final quarter of 2023. But if we annualize the results seen for the first nine months of the year, we would expect adjusted operating cash flow of $435.8 million and EBITDA of $620.2 million. Using those results, I was then able to value the company as shown above. The 2023 data does show that the stock is more expensive than if we were to use the data from 2022. But in both cases, shares look rather attractive. I then, in the table below, compared the company to five similar firms. When it comes down to the price to operating cash flow approach, Sonic Automotive ended up being the cheapest of the group. And when it involves the EV to EBITDA approach, it was tied with one other as the cheapest.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Sonic Automotive | 4.2 | 5.3 |

| Group 1 Automotive (GPI) | 9.5 | 6.6 |

| Asbury Automotive Group (ABG) | 16.7 | 5.3 |

| Lithia Motors (LAD) | 24.4 | 8.5 |

| AutoNation (AN) | 6.8 | 6.7 |

| Penske Automotive Group (PAG) | 8.0 | 7.7 |

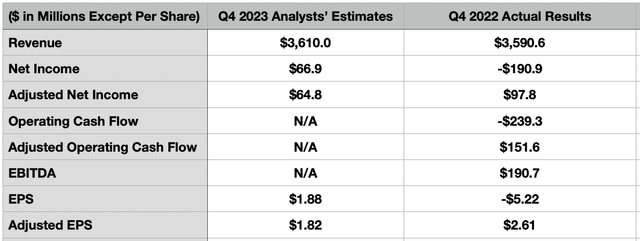

It is worth noting that the picture can always change. The next opportunity for such a change is just around the corner. Before the market opens on February 14th, the management team at the business is expected to announce financial results covering the final quarter of the 2023 fiscal year. Analysts expect revenue to come in at $3.61 billion. But that would be only marginally higher than the $3.59 billion reported one year earlier. Earnings per share are expected to be $1.88, translating to profits of $66.9 million. That would stack up nicely against the $5.22 loss per share reported one year earlier. On an adjusted basis, however, earnings are expected to fall from $2.61 per share to $1.82. That would bring adjusted profits down from $97.8 million to $64.8 million. Neither management nor analysts gave forecasts when it came to other profitability metrics. But in the table below, you can see what some of these were for the final quarter of 2022. In all likelihood, the final quarter of 2023 will have looked a bit worse.

Author

Takeaway

There is no denying that Sonic Automotive is facing some issues from a profitability standpoint at this time. That is rather unfortunate. However, the long-term outlook is almost certainly going to be positive. A larger population should lead to additional car sales over time. Cash flows are still attractive even in spite of the weakness and the stock is amongst the cheapest out there when it comes to this industry. Management also is taking advantage of this opportunity. During the first quarter of 2023, the firm allocated $90.7 million toward buying back stock. They did not buy back any during the second quarter but did go on to buy back $86.8 million worth in the third quarter. That still leaves the company $286.8 million worth of capacity under its existing share buyback program. In fact, since 2019, the company has repurchased around 21% of its outstanding units. Although I am not a huge fan of buybacks myself, I love seeing them when shares are this cheap.

All things considered, this data suggests to me that Sonic Automotive should be a good prospect for value oriented investors. And because of that, I have no problem keeping it rated a ‘buy’ for now.

Read the full article here