")

Summary

Following my coverage of CNH Industrial (NYSE:CNHI), for which I recommended a neutral rating due to my expectation that the business would see near-term weakness because of various reasons such as inventory surplus, weak macro environment and demand, etc., this post is to provide an update on my thoughts on the business and stock. I still think it’s best to stay neutral on this stock given that the concerns I had previously are still present, which could put pressure on FY24 performance.

Investment thesis

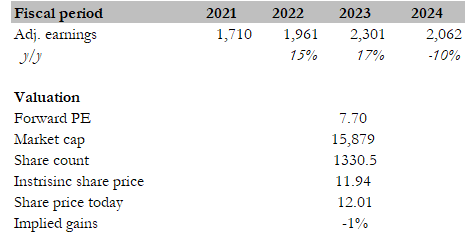

CNHI reported 4Q23 adj EPS of $0.42, which was pretty much in line with guidance of $0.41. Overall revenue (industrial only) fell by 5% to $6 billion, underperforming guidance of $6.4 billion. However, industrial adj EBIT grew by $17 million to $696 million, implying a margin of 11.6%, which was up 90bps vs 4Q22. Adj earnings came in at $556 million, ending the year with $2.35 billion in adj earnings, beating my expectation of $2.26 billion.

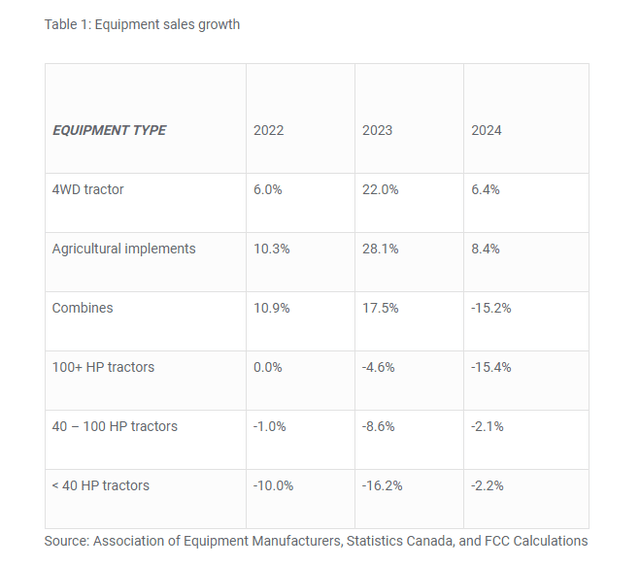

Despite the better earnings performance, I don’t think CNHI is out of the woods yet. The main concerns I had—inventory surplus and weak demand—continue to be headwinds. As of 4Q23, management still sees approximately $1 billion worth of excess dealer inventory in the agriculture segment and aims to work through this in 1H24. In particular, inventory remains elevated for certain product categories in North America, such as low-HP tractors (down ~40% in 2H23 following a surge in 4Q22), as well as large agriculture equipment in Europe. That said, CNHI is making progress on resolving this issue, as can be seen from the 40% reduction in low-HP tractors in North America since the surge in 4Q22, the healthy inventory situation in Brazil, and the moderating inventory growth on a headline basis (4Q23 grew 5%, which decelerated vs. 3Q23). In a normalized demand environment, I would give management the benefit of doubt that they can resolve this by 1H24. However, the current demand situation remains weak and uncertain. Demand for combines in the industry saw a significant drop in the most recent quarter across EMEA and North America. The continuing protests by farmers have also dampened sentiment in Europe. Even in South America, the demand situation remains poor, with declines across all product categories in 4Q23 for agriculture. In addition, based on management expectations, commodity prices are expected to be down for a couple of years, which will continue to put pressure on farmers’ income and indirectly on demand for equipment. Major players in the industry (Deere) are also sounding the alarm bells on poor agriculture equipment demand. The association of equipment manufacturers also expects a poor demand outlook for CY2024.

In agriculture, the net sales decrease of 8% in the quarter was driven by lower industry demand, especially in South America for all product categories and for combines in North America and EMEA.

So we’re starting from a better place. Soft commodity prices are likely to be down for a couple of years and I think we are just expecting the industry be flattish from here for a little while. 4Q23 earnings results call

AOEM, Canada Stats, FCC calculation

The positive takeaway that supports a bullish outlook for the next upcycle is that management noted that the agriculture equipment cycle is more resilient relative to history. As per management estimates, this cycle is unlikely to see a significant step down similar to what the industry saw 15 years ago, as current conditions are a better starting point for this cycle’s downturn. Frankly, I do agree as farmers balance sheets are a lot healthier (debt to equity ratio is now lower relative to previous decades); and the industry is now a lot more technologically advanced than before, which means better productivity and yield (i.e., a lower need for more equipment to grow, easing the magnitude of over/undersupply).

In the next cycle, CNHI would also be in a better position from a cost perspective as I expect it to successfully pull off its cost of goods sold [COGS] reduction program. Of the $550 million target, management has already achieved $185 million of cumulative cost savings as of 2023, and they are focused on achieving the remaining ~$365 million of savings this year. For comparison sake, $365 million is an additional 140bps of margin improvement based on last 12 months EBITDA and sales. Apart from the savings on COGS, management is also expecting savings from its SG&A restructuring program, which aims to cut SG&A costs by 10-15% by FY25. This translates to savings of $160-240 million by next year, with an interim target of $140-180 million in FY24. All in all, by the next up cycle, CNHI will be able to operate with a much lower cost structure (>$600 million less, which is >200bps based on last 12 months sales), that it can either share with customers or shareholders (via increased dividends or buybacks).

Valuation

Own calculation

My target price for CNHI based on my model is ~$12. Looking at how the inventory and demand situation have developed, I don’t think CNHI will be able to meet my previous expectations for $2.2 billion in adjusted earnings for FY24. Based on management FY24 adj EPS guidance of $1.55 at the midpoint, I back into an adj earnings expectation of $2.06 billion (based on 1.33 billion shares outstanding). This translates to a 10% decline in EPS. With the expectation of a decline in EPS, a weak demand outlook, and lingering headwinds from the inventory surplus situation, I don’t see any positive catalyst that will drive the valuation up in the near term. As such, I assume the valuation will stay at the current level of 7.7x forward PE.

Conclusion

My neutral rating for CNHI remains unchanged as the concerns highlighted in my previous coverage persist, which I expect to continue putting pressure on performance in FY24. Specifically, challenges such as excess dealer inventory, weak demand, and global macroeconomic uncertainties persist. The reduction in low-HP tractors inventory in North America and progress in the Brazil inventory situation is promising, but the demand situation remains fragile. That said, looking ahead, CNHI’s cost reduction programs position it favorably for the next upcycle. With a lack of visible catalyst, I don’t see a reason for the market to rerate valuation upwards.

Read the full article here