Investment Thesis

The Tyson Foods, Inc. (NYSE:TSN) investment thesis surrounds their ability to recover margins back to historical levels. In the latest fiscal year, GAAP Gross Margins collapsed to 5%, a significant drop from the 2022 level of 12.5%. This decline was primarily attributed to rising input costs, pushing Cost of Sales to unprecedented levels. I am initiating a buy recommendation on the company due to the optimistic guidance projecting TSN to return to profitability this fiscal year and I believe the company stands to benefit from their productivity program. Several factors look appealing, including the valuation, projections, improved credit risk, and the company’s position to adapt to changing consumer preferences.

Background

TSN operates in the food industry and is the second-largest processor and marketer of chicken, beef, and pork. Together with its subsidiaries, it operates major US food brands such as Jimmie Dean and Hillshire Farm under its Prepared Foods segment. Beef contributes 37% of sales followed by Chicken at 30%, Prepared Foods at 19%, and Pork at 11%. TSN has achieved their market-leading position through principal marketing and a competitive strategy that includes identifying target markets and utilizing a national distribution system.

However, due to the nature of business and growing concerns around animal welfare and the environment, TSN has been at the heart of many controversies and more recently during the COVID-19 pandemic. Allegations surfaced that TSN had failed to implement sufficient COVID-19 protocols, leading to lawsuits against the company. The resolution of these legal proceedings remains uncertain, leaving the outcome undetermined as to whether compensation will be awarded to victims or whether TSN pay a fine.

The 2022 productivity program

TSN saw the launch of their new three-pillared productivity program in 2022, with ambitions to drive a better and more agile organization. The first pillar aims to generate cost savings amongst the finance and HR departments of the firm. The second pillar addresses the use of digital and AI predictive analytics to drive efficiency across the organization and the third aims to leverage automation robotics. Originally, relative to 2021, they are targeted cost savings of $1 billion by 2024 but, surpassed this target a year earlier than first forecast.

Initiatives undertaken to achieve this restructuring, include relocating staff to their head office in Arkansas and reducing headcount. So far, the company is anticipating pre-tax charges of $224 million from the 2022 program, with more possible restructurings as the company evaluates future growth prospects and business strategies.

In my opinion, the drive by the company to expand productivity is encouraging, especially when targets are met a year earlier than forecast.

Inflationary Market Impacts

TSN has benefitted from rampant food inflation over recent years, sales grew 13.2% in 2022, above the 10-year CAGR, driven by a 12.3% increase in prices. However, since poultry and pork inflation has moderated, the company has begun reducing prices across a range of products. In the 3 months to December TSN reduced prices across Pork, Chicken, and Prepared Goods, but managed to maintain growth in their Beef segment, for an overall gain in sales of 0.4%.

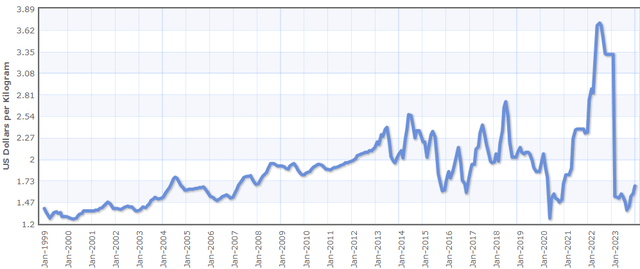

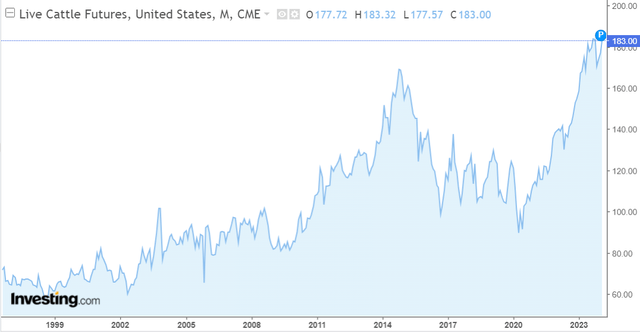

Profitability shows a contrasting picture, the Beef segment swung to a loss in December due to inventory write-downs but, in comparison, pork and chicken have recovered with margins moving back towards historical levels. The figures below show poultry and cattle prices, both types of meats experienced rapid inflation during 2021 and 2022, poultry prices have fallen back and below levels pre-COVID, in contrast, beef has continued its trend up squeezing margins for TSN. The reason for the rapid inflation is that cow inventories are the lowest in 73 years, as a result of a 3-year prolonged drought in the US. That strong demand has led to an increase in cattle futures, that are squeezing profits. So far, it doesn’t look like cattle farmers are increasing cattle numbers, so the squeeze could continue into 2024.

poultry price chart (index mundi) cattle futures chart (investing.com)

Guidance looks good, TSN are forecasting Adjusted Operating Income of $1 billion – $1.5 billion with sales broadly flat on the prior fiscal year. That would equal Adjusted Operating Margins close to 3% and a fine recovery from current conditions.

Longer Term

The OECD is forecasting most of the growth in demand for meat to come from middle-income and lower-income economies due to disposable income and population growth. But 96% of TSN sales are situated in the US, a high-income country. The main deterministic factors driving demand for meat in the US are human, health, environmental, and animal welfare motivations. Poultry has the lowest carbon footprint and is considered white meat for dietary reasons. As a result, poultry is expected to form 45% of total meat protein in high-income countries by 2032, slightly up from 2022 and up in comparison to other meats.

What does this mean for TSN? For TSN this is inherently positive. They manage a vertically integrated supply chain of poultry meat and this produces the highest operating margins of any other segment. As poultry becomes a larger source of business, margins should improve and the company will become more profitable.

Credit Risk

Credit risk has improved since September, TSN added $911 million in cash resulting in a balance of $1.5 billion which is sufficient to cover the August 2024 principal. Later principals include 2026 and 2027 but with TSN generating over $1 billion in Free Cash Flow and with profitability returning, the risk of default doesn’t feel as high as it did in September, another reason I am initiating a buy on TSN.

TSN annual report

Valuation

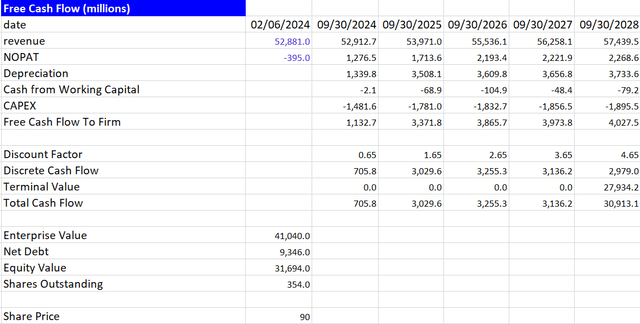

At the current share price and with a multiple of 8x it feels like the market is pricing in Operating Margins getting to 3% and then not growing at all. With the productivity program and long-term prospects for poultry growth, that feels unlikely. So I have Operating Margins reaching 5% by 2026 and in a conservative scenario have EBIT margins staying at 5% to 2028. With a multiple of 9x which is the 10-year P/CF median, I get a share price of $90 which is an upside of 58%.

Source: Author’s calculations

Next Quarter and risks

Even though consumers are facing higher prices than they were 2-years ago I think they will continue to buy brands they know and trust. Last year three out of four households purchased a TSN product, and I believe this strong market penetration will continue into the next quarter.

Moving on to the segments, I think Prepared Foods will continue gaining traction into the next quarter, with better operations and lower raw material costs continuing to drive margin expansion. In Chicken, I think the strategic moves they took to improve live operations, yield, and labor will benefit margins further and TSN will continue to see a recovery here. In beef, I think spreads will remain tight and profits squeezed, as cattle futures continue trending higher. In Pork, the supply side is improving, which is benefitting spreads, so similar to Chicken expect a continued recovery in margins.

The first obvious risk here is a bad outcome from the COVID-19 lawsuit and bad publicity. Aside from that, if food inflation picks up again and spreads tighten the company could face losses and struggle to meet its outstanding debt obligations. I think in the Beef segment the tight spreads will continue until the supply side improves, but in Chicken and Pork, I think spreads will expand mitigating the company’s credit risk.

In my view if TSN reduce their guidance on Adjusted Operating Income that would be a basis to downgrade my recommendation.

Conclusion

TSN is a company coming out of recovery. On the demand side, the company is positioned well to become a more profitable organization as high-income countries turn to white meats and specifically Chicken when consuming protein.

Before I would have had TSN as a Hold because of the credit risks, but it feels like the market is now seriously mispricing this security. My conservative valuation approach has the share price potentially 58% up from today’s price and that is without considering the effects of poultry becoming a larger portion of sales. We could see margins reach 8% by 2028 which doesn’t feel impossible considering the company has achieved this in the past.

Read the full article here