For most of the last 15 months, we have held strongly negative views on DNP Select Income Fund (NYSE:DNP). This has generally worked out and the CEF has struggled to make headway in this timeframe.

Seeking Alpha

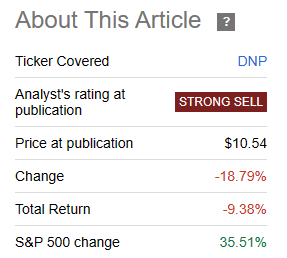

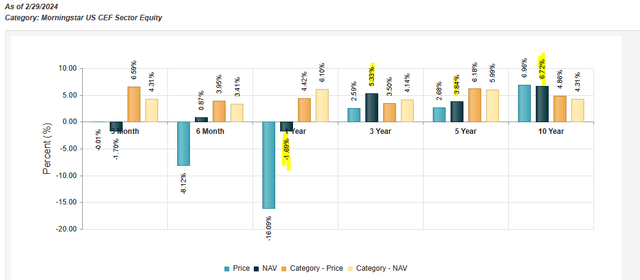

Since the “Strong sell” rating in October 2022, the CEF has underperformed the S&P 500 (SPY) by almost 45% on a total return basis.

Seeking Alpha

On our last coverage we upgraded this to a “Hold” and cited the primary factor as follows.

We don’t believe it will work out in the medium term. In the short term, the Z-score on DNP has really blown up. A big negative number here suggests that the fund is currently priced cheaper than it has been in the past. So there is some risk of DNP rebounding here. We are upgrading this to a “Hold”, from a “Strong Sell”.

Source: One Clear Winner Amongst Utility CEFs

We go over three reasons today as to why we are shifting back into the “Sell” zone.

1) Dead Cat Bounce At Least Partially Over

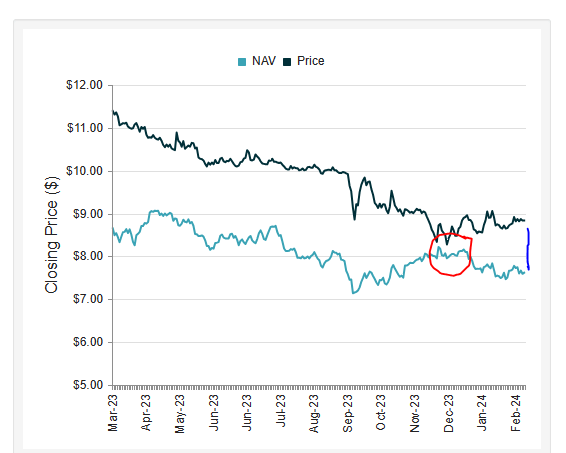

Investors must be wondering what exactly are we talking about as the CEF is not materially higher than when we switched to a “hold”. In fact, it is about as flat as things can get. But the devil here is in the details. Underneath the surface the fund’s NAV has had a terrible performance relative to the market. The NAV has dropped close 4.5% and this has led to the reopening of the jaws. Below, you can see the circled area as what we were looking at in late November- early December, as the key reason for some optimism.

CEF Connect

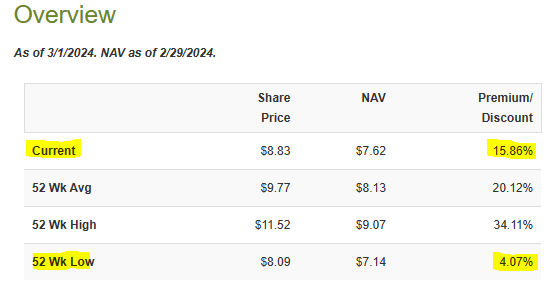

After years of trading at an outlandish premium, DNP’s price was almost the same as its NAV. Our experience is that most of the time, this at least leads to a temporary bottom and it has been a foolish move to ignore this setup. That worked as we expected, with the recent NAV premium now at 15.86%.

CEF Connect

Yes, this appears to be in the middle of the path, but there are zero reasons to bid funds up to these levels of premiums, especially when you consider reason number 2.

2) Distribution Still Looks Wild

Yes, it is a managed distribution plan and it can go on for longer than many expect. It is also true that you won’t get a personal “RSVP” to the day of the rug pull.

The Board of Directors adopted a Managed Distribution Plan, which provides for the Fund to continue to make a monthly distribution on its common stock of 6.5 cents per share. Under the Managed Distribution Plan, which required an SEC exemptive order to implement, the Fund will distribute all available investment income to shareholders. If and when sufficient investment income is not available on a monthly basis, the Fund will distribute long-term capital gains and/or return capital to its shareholders. The Board may amend, suspend or terminate the Managed Distribution Plan without prior notice to shareholders if it deems such action to be in the best interest of the Fund and its shareholders

Source: DNP

DNP is distributing 78 cents annually and that works out to over 10% on its NAV. The fund has not generated total returns of anywhere in the ballpark of 10% in the last 1, 3, 5 or 10 years.

CEF Connect

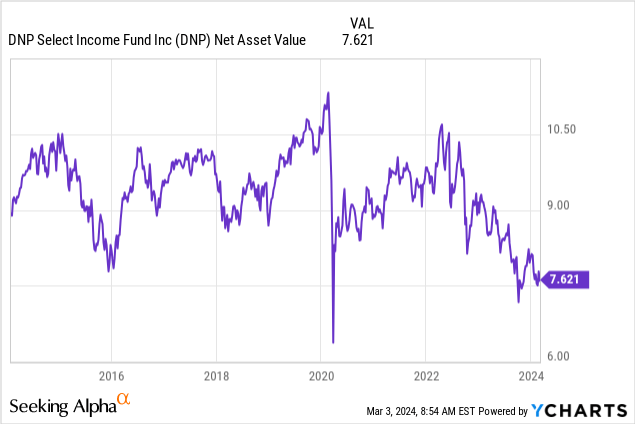

So distribution sustainability requires a heavy measure of faith and one that we lack here. With the market at all-time highs, DNP’s NAV is down under its 2016 lows.

That NAV depletion has come from constantly paying more than it earns as visualized by total returns over various timeframes.

3) Risk Management Requires A Sell

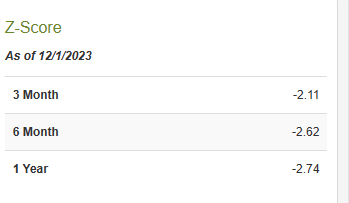

There is some math behind our work here and investors may recall that the upgrade to “hold” was built a bit on Z-scores at the time. DNP had a negative 2.11 3 month Z-score and even lower numbers for 6 months and 1 year.

CEF Connect From December 1, 2023

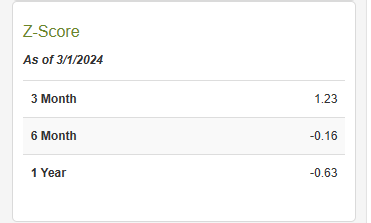

Today, we are in very different territory.

CEF Connect

Your downside risks are back on the table. With these funds carrying fat and undeserved premiums, you can be right about a cut once and wrong up to 4 times, and still come out ahead by avoiding all of them. The reason is when even one cuts the distribution, your losses on that one outweigh the extra distributions from the remaining 4. Flaherty & Crumrine Income Securities Fund (PFD) is a great example of how a distribution story chase can turn into a nightmare. Details can be seen here.

Verdict

The fundamentals for utilities are not the best in the world. The companies have racked on a lot of debt and most are struggling under this higher for longer environment. When they choose to deleverage, it hurts the bottom line and hurts it hard. Take the case below where the company sold assets to get leverage back in line and this was the result.

Dominion Energy (NYSE:D) -2.7% in early trading Friday after saying in an investor presentation that it expects FY 2024 adjusted earnings in the range of $2.62-$2.87/share, below $3.03 analyst consensus estimate.

Source: Seeking Alpha

Dominion’s earnings are actually a great example as their 2024 numbers will be 35% below its 2019 earnings. They are well into the deleveraging phase and earnings look to be bottoming. But most other utilities have a way to go get leverage back in line. Based on what DNP owns, we think 6%-7% annual returns on NAV are probable.

DNP

There are downside risks to this forecast, considering that DNP employs a rather heavy dose of leverage. If you actually get that distribution cut over the next 5 years, something we give a 90% probability to, you could swing from a 15% premium to a 15% discount. That should wipe out almost all your distributions. Total returns on a purchase here would badly trail even holding a 5 year Treasury note. We rate this a Sell and would get more constructive if we saw pricing within 2% of NAV.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here