Ulta Beauty (NASDAQ:ULTA) is expected to report earnings on Thursday 14th of March. For more background information about the company please refer to my previous article “Ulta Beauty: Time to Re-Accelerate”, in which I explained my bull thesis. This article will give a short preview about the upcoming earnings.

I last covered ULTA in November, initiating a “buy” rating below $400 per share and the stock has risen by over 40% since then. The market is a bit confused about this company, rating it as either a mature retailer or a promising growth company. The company now trades back at around the same level of $550 per share, like it did in April/May of 2023 before the lows of October/November.

Previous Article (Ahoy Alpha, 2023)

The market has relatively high expectations for the upcoming earnings call after the stock gained about 40% in the last quarter. The expected numbers are $7.53 earnings per share and $3.52B in total revenue for Q4 2023. For the full year of 2023 that amounts to $11.7B in revenue and $25.52 in EPS, which is 9.5% revenue growth and 6.5% earnings growth compared to FY2022.

We expect the company to meet these expectations, but we are not adding to our position at this point because we believe that the company trades at around fair value. The best recent opportunity to buy at a margin of safety price was near the October lows. We therefore rate the company as a “Hold”, but we will pay close attention to the upcoming earnings call to understand management’s long-term strategy. In the case that management presents a convincing long-term strategy for future growth, we will consider adding to our position. Most importantly, we want the company to start expanding internationally to re-accelerate growth because of the large potential of global beauty markets.

Estimating FY2023 numbers

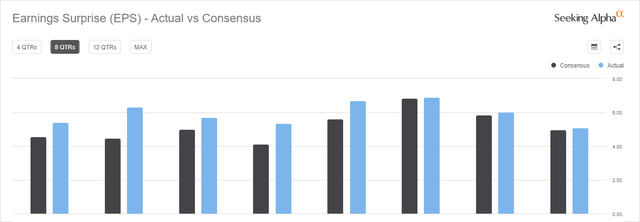

Using the updated company guidance of 10% net sales growth for FY2023, EPS of $25.20 to $25.60, and $950m in buybacks for the full year, we expect the company to perform in line with their own guidance. The company raised its guidance last quarter because of good performance, and I expect them to reach these numbers given their good track record beating expected EPS numbers every time in the last 2 years and never missing on guidance.

So taken together, I believe that there is a possibility for a small earnings beat on the cards. The $950m buyback program will decrease shares outstanding by about 3.5% which should spur EPS growth. US consumer spending during the holiday season also grew more than expected according to the National Retail Federation, with health and personal care retailing sales up 9% YoY.

ULTA track record (Seeking Alpha, 2024)

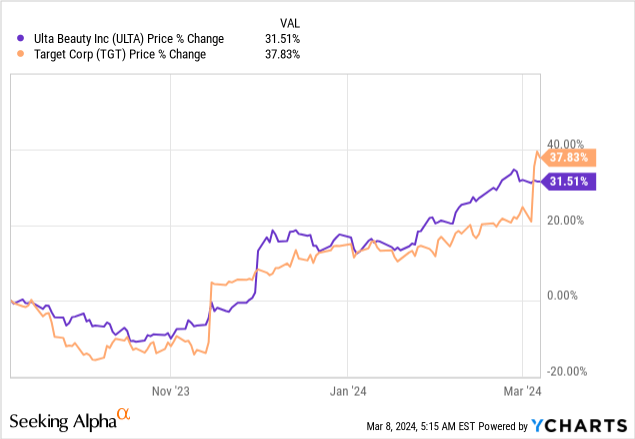

To get a better understanding of the market, we can look at a similar business that has reported earnings last week before ULTA does. In particular, Target (TGT) is a good comparison because it is a similar business as a discretionary retailer, and ULTA products are now increasingly sold at Target’s locations as part of their new collaboration with the shop-in-shop concept, see below.

ULTA shop-in-shop at Target (Target, 2021)

You can see in the chart below that ULTA’s stock price (in purple) roughly follows TGT’s stock price (in orange). When TGT reported strong earnings in November and TGT’s stock rose, ULTA shares gained a few weeks later as well. TGT recently reported strong earnings again, high above expectations showing sequential improvements in sales growth and revenue. We expect this relationship to hold and ULTA to report good numbers as well based on their own updated guidance and the strong reported numbers from TGT last week. Moreover, ULTA’s biggest competitor, Sephora owned by LVMH reported good numbers for Q4 FY2023. Overall, these positive signals coming from similar businesses provide confidence for ULTA’s upcoming earnings report.

The bar is set pretty high for ULTA, so there is possibility for disappointment. Beyond the numbers for this quarter, investors want to see a long-term plan from management about what they aim to achieve in the coming five to ten years. In the case that there is no clear plan announced for future growth, it might be time to sell and the stock may lose a couple percentage points as investors lose excitement about the company’s future and exit their positions. If the company does announce a convincing plan for the coming years, then it might be a good decision to hold or add to our long-term ULTA position.

Conclusion

Our rating for ULTA going into the earnings call is a “hold” after a 40% surge in the past quarter. We will pay close attention to their upcoming earnings call and see what management has in store for us. At these price levels, we argue that the undervalued buying opportunity has disappeared, and we will not add to our position at this moment in time. That being said, we believe the company is trading around fair value at this point priced at around the same levels of April 2023, and the company is performing well, so there is no clear reason to sell. The company provided good guidance and TGT reported strong numbers, so we expect the company to report numbers in line with analysts’ estimates. However, depending on the plans announced in the earnings call, we will re-evaluate our long-term ULTA position and possibly add or sell in the future. We expect to see a clear plan for the coming years from management.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here