")

Introduction and Investment Thesis

Pinterest (NYSE:PINS) is a visual discovery and online bookmarking social platform where users can find and save ideas for various interests with the purpose of shopping for those interests later. The company saw a huge boost in users during the pandemic, leading to a massive spike in its market value in 2021. However, with rising inflation and interest rates, Pinterest’s user growth started to erode, and the stock’s market value dropped by (82)% between 2021 and 2022. Since then, the management has taken active steps to rapidly improve its user experience by adding a suite of search, discovery, and shopping features to the platform.

The company has since seen its monthly active users grow and surpass the 2021 levels, as it stands at 498M users as of Q4 FY23. At the same time, the company has continued to invest in building strategic partnerships with advertisers in order to drive user monetization. Finally, the management has shown tremendous discipline in driving profitable growth as it continues to streamline operating expenses.

While there are risks pertaining to the overall macroeconomic condition in the US, monetization uncertainty outside of the US & Canada, and growing competition, I believe that Pinterest should be able to navigate through those. In my opinion, Pinterest is currently undervalued and presents a valuable long-term opportunity for investors at these levels.

About Pinterest

Pinterest is a social commerce-based product discovery platform where approximately 498M users visit the site every month to share, explore, and shop for ideas related to various interests. Users can also create themed collections on the platform, known as boards. Whether it’s recipes, workouts, travel, fashion, or wedding planning, users can discover and save content (images, videos, etc.) through “pins,” which are often shoppable.

Pinterest operates on a business model that doesn’t charge users for registration. Instead, the platform primarily generates revenue through advertising, particularly through “Promoted Pins.” These paid advertisements are strategically displayed on users’ boards, aligning with relevant search terms and interests of the users, offering a valuable avenue for businesses to reach a broader yet highly targeted audience who visit the site to search for inspiration to shop.

Building the bull case

Ambitious Revenue Growth Projection Amidst Expanding TAM, Gen Z Surge, and Successful Amazon Partnership

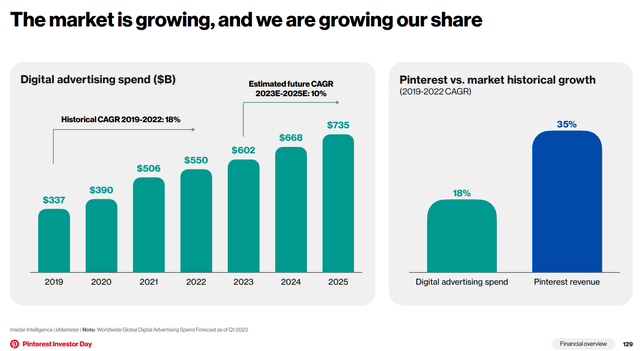

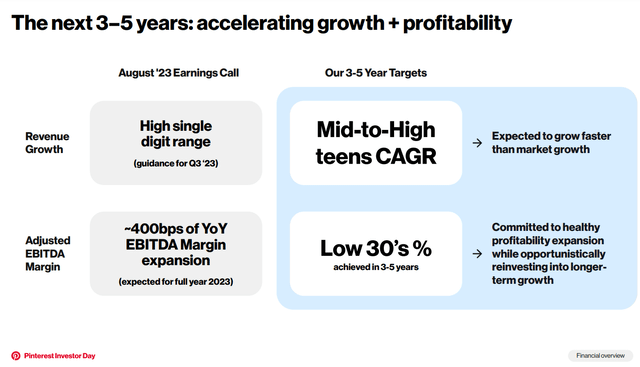

As per its latest Analyst Day Presentation, Pinterest estimates the overall digital advertising spend to grow at a CAGR of 10% from $602B in 2023 to $735B in 2025. As the company finished FY23 with a total revenue of $3.055B, that would represent a market share penetration of 0.5%. During the Investor Presentation, the management indicated that it expects to see revenue growth in the mid-to-high teens over the next 3–5 years. This would mean that Pinterest would be growing faster than the growth rate of its total addressable market (TAM), allowing the company to gain incremental market share globally in the coming years.

2023 Investor Presentation: Pinterest’s TAM and growth projection

Moving to the trends in its user base, I noticed that Pinterest’s monthly active users ((MAU’s)) grew 11% YoY to 498M as of Q4 FY23. Given the positive reversal in Pinterest’s user volume, making new all-time highs, I believe the company is well-positioned to attract new MAUs as it continues to build robust search, discovery, and shopping features to drive user engagement on the platform.

Simultaneously, the company is also experiencing a boost in its user base from Gen Z users, which now represent 42% of the total MAU’s. As Gen Z’ers graduate from school, transition to their first full-time job, and gather more spending power, I believe Pinterest should stand to benefit from the demographic tailwind to drive revenue growth, as long as management remains focused on its long-term product vision. During their Investor Presentation, the management noted that GenZ users are the fastest-growing cohort, growing at 20% YoY in Q2 FY23, 2.5x faster than the overall rate of MAU’s growth. Plus, Gen Z’ers are saving 2.4x the content compared to the rest, which I believe showcases superior engagement on the platform that ultimately leads to a shopping decision down in the user journey funnel.

Finally, I am also encouraged by management’s initiatives to expand the application of its platform in building its advertising business. Last year, the company announced its partnership with Amazon (AMZN) to direct third-party ad demand to Pinterest’s platform. In its most recent Q4 earnings call, the company also announced its third-party ad integration with Google (GOOG). I believe that through these partnerships, Amazon and Google can target Pinterest’s users with highly targeted ads that are highly relevant to Pinterest’s users as they search for shopping interests on the platform, increasing the scope of engagement and revenue.

Pinterest’s CEO noted this in his most recent Q4 FY23 earnings call about the Pinterest-Amazon partnership:

“As a smaller player in the overall digital ad ecosystem, adding third-party demand to increase the comprehensiveness of our catalog and the relevance of our ads was a key priority for us. Last year, we announced and launched our first third-party ad partner with Amazon Ads, which is scaling well, and we will continue to advance our third-party demand efforts this year and beyond to bring relevant ads that can enhance the user shopping journey.”

Pinterest’s management is focused on driving profitable growth into the future.

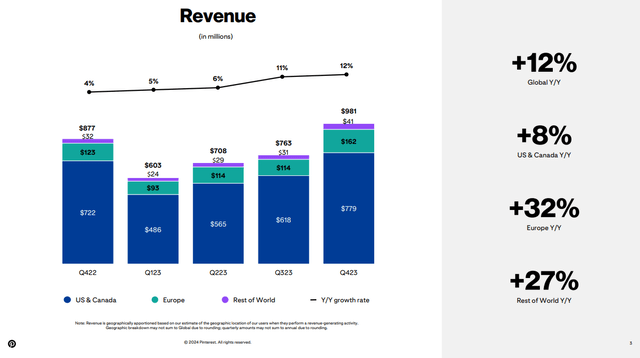

Pinterest produced solid growth on both the top and bottom lines. Revenue grew 12% YoY to $981M in Q4, and 9% YoY to $3.055B in FY23. As for the revenue drivers, Pinterest saw revenue growth of 21% from its “Europe” segment and 31% from its “Rest of the World ((RoW))” segment in FY23. In the meantime, the US & Canada, which account for approximately 80% of all revenue, grew 6% on a YoY basis. I would also like to point out that Europe’s contribution to overall revenue increased from 14% in Q4 FY22 to 16.5% in Q3 FY23.

Q4 FY23 Earnings Slides: Pinterest’s Revenue across geographies

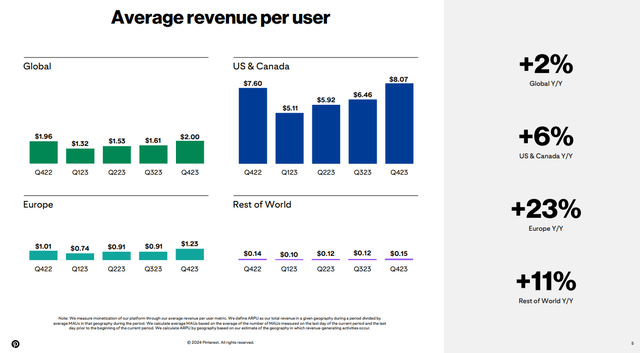

Meanwhile, Average Revenue per user (ARPU) grew 1% YoY in FY23. Although Europe and RoW saw significantly faster ARPU growth of 15% and 17%, respectively, for FY23, the dollar value of ARPU is abysmally low in Europe and RoW, compared to the US & Canada regions.

Q4 FY23 Earnings Slides: Pinterest’s ARPU across geographies

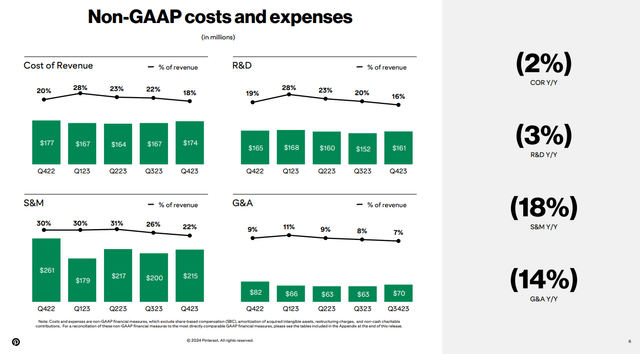

At the same time, Adjusted EBITDA grew 54% YoY to $683M in FY23, with the Adjusted EBITDA margin improving from 16% in FY22 to 22% in FY23. The improvement in Adjusted EBITDA was driven by streamlining Sales and Marketing spend, which amounted to 29% of Total Revenue in FY23 vs. 33% of Total Revenue in FY22. I believe this is a clear indication of the underlying growing strength of the operational efficiency of the company as well as management’s commitment to drive profitable growth.

Q4 FY23 Earnings Slides: Pinterest’s improving operating expenses

Shifting gears to Q1 FY24 guidance, Pinterest management is guiding for revenue growth of 15–17% YoY to $690-$705M. Meanwhile, the management expects the company to spend $450-$465M in Non-GAAP operating expenses in Q1. Assuming the company maintains its current non-GAAP gross margins in the 80% range, this should translate to an Adjusted EBITDA of approximately $100M in Q1, representing a margin of 14.5%, an improvement of 1000 basis points ((b.p)) YoY.

Looking further ahead, over the next 3-5 years, Pinterest management expects the company to produce revenue growth in the mid-to-high teens while growing its Adjusted EBITDA margin in the low 30% region, which I believe further demonstrates the management’s continued commitment to drive profitable growth.

2023 Investor Presentation: Pinterest’s long-term financial model

Building the bear case

Uncertainty pertains to slower US spending and monetization in international markets.

I believe that the growth story of Pinterest is tied to consumer spending, especially in the US, which would then drive ad revenue for the company. While global ad spending is expected to grow 5.7% YoY in 2024, there is also growing evidence that the US Fed is going to keep interest rates higher for longer as inflation remains stubbornly above target. These factors can dampen US consumer spending in 2024 and possibly beyond. Should the US economy slow down or, worse, tip into a recession, I believe Pinterest’s growth trajectory will undoubtedly be affected, as it will likely see a drop in MAU’s who would no longer be willing to shop, reducing the platform’s appeal to advertisers.

Furthermore, as per their latest earnings call, 80% of MAU’s come from outside the US & Canada, yet they only contribute 20% of Total Revenue. In my view, this indicates that there are significant challenges that Pinterest faces in optimally driving user monetization outside of the US & Canada.

Tying it together: Pinterest stands to gain 25% from its current levels.

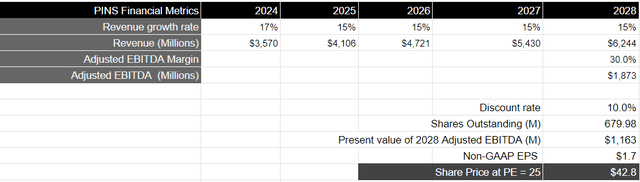

Taking Pinterest’s 3-5 year plan as per its Investor Day Presentation, I believe that the company will be able to generate revenue of at least $6.2B in FY28, assuming revenue grows 15% annually every year over the next 5 years, as the company continues to innovate on its platform to attract active users while building out its advertising business to drive effective monetization.

In the meantime, the company is expected to improve its adjusted EBITDA margins from 22% in FY23 to low-30% over the next 3–5 years. If I proceed with the assumption that Adjusted EBITDA margin will grow to 30% by FY28, Adjusted EBITDA would need to grow annually by 23%, faster than the revenue growth rate. This will be driven by focused product development, better ad products, and growing third-party partnerships that will positively impact operating leverage. In this case, the company should be able to generate close to $1.87B in Adjusted EBITDA by FY28, which would equate to a present value of approximately $1.16B if discounted at 10%.

Taking the above assumptions into consideration, I believe that the forward price-to-earnings ratio for Pinterest in FY28 should be around 25. Taking the S&P 500 as a proxy, where it has grown its earnings by 8% on average over the last 10 years, as per Factset, with a forward price-to-earnings multiple in the range of 15–18, I believe that Pinterest should be trading at a price-to-earnings multiple of 1.5x the S&P 500 in FY28. As the company matures, I believe that the revenue growth rate will normalize to low teens after FY28, with earnings that will grow more or less in line with the revenue growth rate, as most of the efficiencies in operating leverage would have been realized. This will result in a price target of $42 for Pinterest, looking at a 5-year investment horizon, which would translate to an upside of approximately 25% from its current levels.

Author’s Valuation Model

Conclusion

So far, I am deeply encouraged by Pinterest’s rapid turnaround in its product and platform strategy, which has brought back users en masse who continue to be deeply engaged. This bodes well for the company’s advertisement business to drive user monetization at the same time. Although there are risks pertaining to the overall macroeconomic condition in the US and monetization uncertainties outside of the US & Canada, I believe that the company’s product vision and commitment to profitability will drive sizable returns for the stock over a 5-year investment horizon.

Read the full article here