")

We previously covered Opera Limited (NASDAQ:NASDAQ:OPRA) in December 2023, discussing its improved monetization trend and growing ARPU, leading to its strong financial performance in FQ3’23 and raised guidance for FY2023.

Combined with the depressed valuations and attractive dividend yields, we had reiterated our Buy rating for the stock then.

In this article, we shall discuss why we are maintaining our Buy rating for OPRA, as the management offers an excellent FY2024 guidance. This is attributed to the improved monetization through the gaming platform, Opera Rx, contributing to its growing advertising and search revenues in higher ARPU regions.

Combined with the management’s use of the robust cash flow for shareholder returns, we believe that OPRA continues to offer both value and growth opportunities at current levels.

The OPRA Investment Thesis Remains Attractive, Despite The Recent Rally

For now, OPRA has delivered an excellent FQ4’23 earnings call, with revenues of $113M (+10.1% QoQ/ +17.3% YoY), adj EBITDA of $27.76M (+16.8% QoQ/ +21.8% YoY), and GAAP EPS of $1.38 (+666.6% QoQ/ +527.2% YoY).

For FY2023, the numbers are at $396.82M (+19.8% YoY), $93.71M (+37.6% YoY), and $1.86 (+1,228.5% YoY), respectively.

However, readers must also note that the FQ4’23 EPS includes a one-time $105.94M gain following the updated valuation of the OPay investment, resulting in an additional boost in its EPS by $1.18.

After adjustments, OPRA reports an estimated FQ4’23 adj EPS of $0.19 (+5.5% QoQ/ -13.6% YoY) and FY2023 adj EPS of $0.69 (+392.8% YoY), respectively.

With a consistently expanding top/ bottom line, it is unsurprising that the company reports excellent Free Cash Flow generation of $72.45M (+69.1% YoY) and margins of 18.3% (+5.4 points YoY) in FY2023.

Much of its tailwinds are attributed to OPRA’s growing Monthly Active Users [MAU] of 313M (+2M QoQ/ -11M YoY) and expanding annualized ARPU of $1.44 (+9.9% QoQ/ +22% YoY) by the latest quarter.

It is apparent that the management’s efforts to boost adoption of the high-ARPU users in the North America, Latin America, and Europe regions have been paying off extremely well, balancing the decline of the low-ARPU users in emerging markets.

Most importantly, much of OPRA’s high ARPU users are attributed to gaming users whom adopted Opera GX, with 27.8M in MAUs across PC and mobile (+1.7M QoQ/ +7.8M YoY/ +26.25M from FQ4’19 levels of 1.55M) and annualized ARPU of $3.51 (+17% QoQ/ +6.3% YoY) in FQ4’23.

This has led to the growing advertising revenues of $67.8M (+11.5% QoQ/ +19.3% YoY) and search revenues of $44.7M (+9.5% QoQ/ +14.6% YoY), as advertising dollars return in view of the increased likelihood of a soft landing in 2024.

Much of the top-line tailwinds are also well balanced by OPRA’s prudent operating expenses of $43.39M (+10.2% QoQ/ +6.1% YoY), resulting in its expanded operating margins of 18.1% (+1.2 points QoQ/ +2.2 YoY/ +18.4 from FY2019 levels of -0.3%) by the latest quarter.

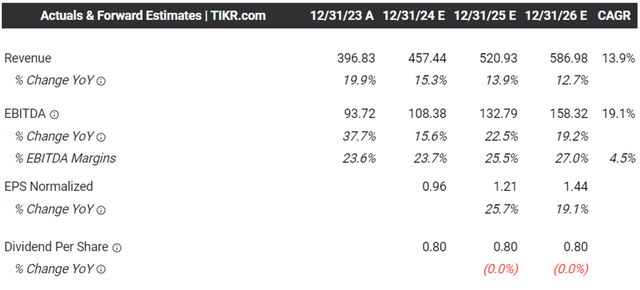

The Consensus Forward Estimates

Tikr Terminal

The same has been observed in OPRA’s exemplary FY2024 guidance, with revenues of $457.50M (+15.2% YoY) and adj EBITDA of $108M (+15.2% YoY) at the midpoint, implying adj EBITDA margins of 23.6% (inline YoY).

It is evident that the management aims to intensify their R&D efforts in generative AI customized content, while investing in closed-loop advertising (without relying on third-party signals and cookies) for users who do not like ads.

This is on top of the intensified focus on the gaming platform, Opera GX, which has been a top-line driver over the past few years, lending support to its user growth and top/ bottom line expansion.

These developments have also directly contributed to the consensus raised forward estimates, with OPRA expected to record a top/ bottom line CAGR of +13.9% and +27.7% through FY2026.

This is compared to the previous estimates of +13.5%/ +19.9% and the historical top-line growth at +20.6% between FY2017 and FY2023, respectively.

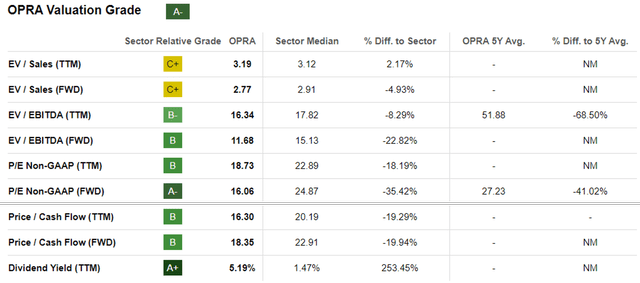

OPRA Valuations

Seeking Alpha

As a result of the profitable growth trend, it is unsurprising that the market has upgraded OPRA’s valuations to FWD EV/ EBITDA of 11.68x and FWD P/E of 16.06x, compared to the 9.27x and 11.04x reported in early January 2024, respectively.

Readers must also note that the stock remains discounted compared to its 5Y valuation mean of 51.88x/ 27.23x, the sector median of 15.13x/ 24.87x, and the browser peers, including Alphabet (GOOG) at 11.70x/ 20.49x and Microsoft (MSFT) at 24.20x/ 34.57x, respectively.

While OPRA remains a small player with 2.47% in the global browser market share as of February 2024 (-0.08 points MoM/ +0.21 YoY), compared to GOOG’s Chrome at 65.3% (+0.89 points MoM/ -0.46 YoY) and MSFT’s Edge at 5.07% (-0.29 points MoM/ +0.79 YoY), it is undeniable that the former has been rapidly improving its monetization rate, as discussed above.

As a result of the immense prospects, we believe that OPRA remains well positioned for long-term growth, making it an excellent opportunity for both value and growth oriented investors.

So, Is OPRA Stock A Buy, Sell, or Hold?

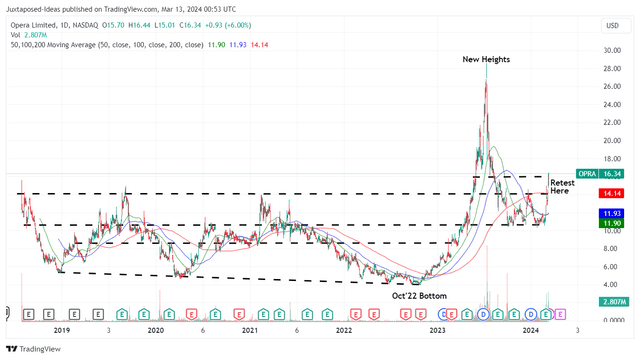

OPRA 5Y Stock Price

Trading View

For now, OPRA has rapidly broken out of its 50/ 100/ 200 day moving averages, while appearing to retest its previous resistance levels of $16s.

Based on the FY2023 adj EPS of $0.69 and the FWD P/E of 16.06x, it is apparent that the stock is trading above our fair value estimates of $11.00.

On the other hand, based on the consensus FY2026 adj EPS estimates of $1.44, the stock offers a relatively attractive upside potential of over +40% to our long-term price target of $23.10.

With practically zero debt, the OPRA management has also been putting much of its robust cash flow towards excellent shareholder returns, with 5.34M of its shares retired over the LTM/ the equivalent 5.6% of its float, and 25.25M/ 22% since FY2019, respectively.

This is on top of the annualized dividends of $0.80 per share, implying a relatively attractive forward yield of 4.8% based on the stock prices at the time of writing, compared to the US Treasury Yields of between 4.07% and 5.37%.

Combined with the improving Book Value per Share at $10.69 (+15.6% QoQ/ +7.3% YoY/+39.3% from FQ4’19 levels of $7.67), it is apparent that the management has consistently delivered sustainable growth thus far.

As a result of the (prospective) dual pronged returns through capital appreciation and dividend payouts, we are reiterating our Buy rating for the OPRA stock after a moderate dip for an improved margin of safety.

Read the full article here