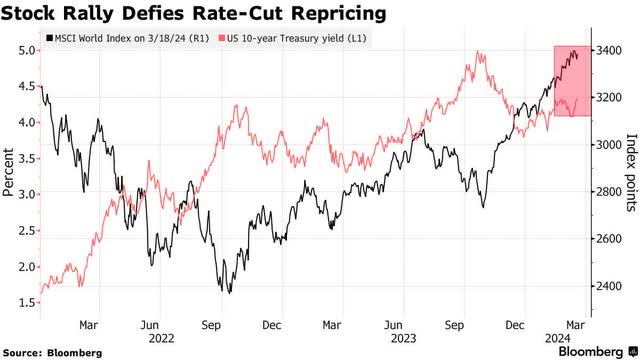

Stocks closed higher ahead of the Fed’s meeting this week, as tech behemoths Apple and Google rebounded on news that the iPhone maker will build Google’s Gemini artificial intelligence engine into its phones. Still, nine of the eleven S&P 500 sectors finished modestly in the green, while small caps struggled, which is likely due to the uncertainty about the Fed’s next move. Tomorrow, investors will be picking through the details of the Fed’s latest “dot-plot,” and parsing every word of Chairman Powell’s press conference, as well as trying to glean any clues about the direction of monetary policy from the updated Summary of Economic Projections. The goal is to determine when the Fed will begin to cut short-term rates and how many cuts will be executed this year. I think we will hear more of the same with no meaningful changes in the outlook.

Finviz

In January, the consensus was expecting six rate cuts, which were expected to start tomorrow. Today, the expectation has fallen to just three, which are not expected to start until June. Bears would have us think this is because the disinflationary trend is coming to an end with inflation reports that were hotter than expected over the past two months. If that were the case, I doubt we would have seen such robust market performance. I think expectations for rate cuts, which have simply fallen in line with the Fed’s January outlook, are a function of an economy that has shown far more resiliency than expected. Therefore, it is not in need of a more aggressive approach than the Fed outlined at the beginning of the year.

Bloomberg

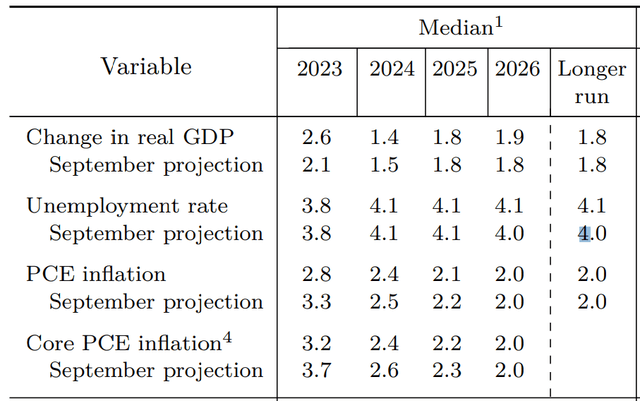

I was expecting cuts to start in March, due largely to the Fed being ahead of schedule in its projections for inflation. It is important to note that the Summary of Economic Projections, which is a consensus estimate from members updated quarterly, has a horrible 6-12 month track record of accuracy on nearly every count. Therefore, I don’t place very much importance on the absolute numbers. Instead, I focus on the direction those numbers are moving.

Federal Reserve

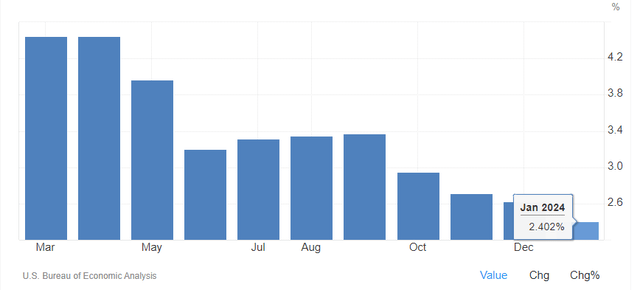

I do not see how the Fed can’t lower its year-end 2024 estimate for its preferred measure of inflation, which is 2.4%, when the core Personal Consumption Expenditures (PCE) price index is already at 2.4% as of January. This is the most important metric in terms of measuring price stability. I think we will see a forecast for a lower number in this category, but that may not influence any of the other numbers. Still, it is likely to move up the first rate cut to May.

TradingEconomics

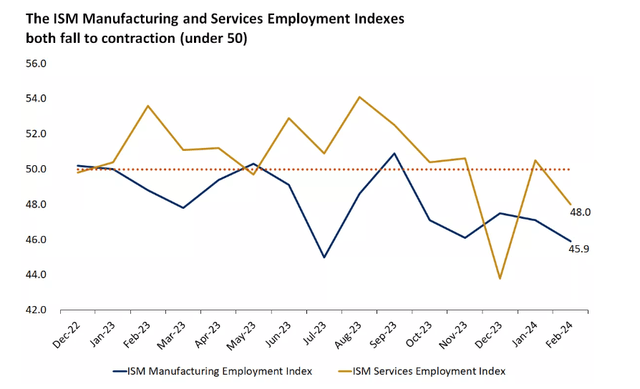

Furthermore, the rate of economic growth is starting to slow. We are starting to see this in the employment surveys for both the manufacturing and service sectors from the Institute for Supply Management. Companies start to hire fewer workers when spending starts to slow. Consumer spending is the tip of the spear.

Edward Jones

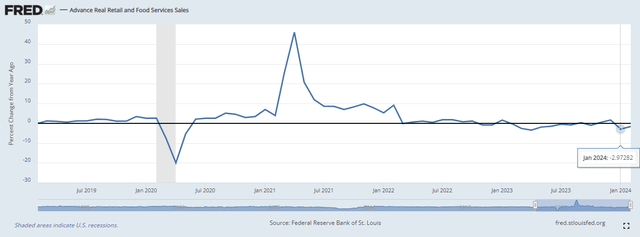

My preferred measure of consumption strength is the real year-over-year growth rate in retail sales. I do not get caught up in the monthly gyrations for any of the high-frequency economic data. That number has been in negative territory for the past three months, but retail sales cover what are predominantly goods categories, and we know that consumers have emphasized services in their purchases well above what has been typical. Overall consumer spending is still growing year-over-year on an inflation-adjusted basis. Still, the softening in retail sales is a signpost for slower rates of economic growth and employment.

FRED

Chairman Powell won’t show his hand anymore than he did in January. Yet the market is likely to start anticipating more rate cuts, which will start sooner, between now and May, as the rate of economic growth slows, bond yields edge lower, and the disinflationary trend reasserts itself.

Read the full article here