")

Introduction

It’s time to discuss a company I believe is one of the most underappreciated dividend growth stocks.

That company is Huntington Ingalls Industries, Inc. (NYSE:HII), one of the largest defense constructors in the United States and the backbone of the Navy.

I held the company for a while in my dividend growth portfolio before I decided to sell it. As weird as that may sound, given that I just called it “underappreciated,” my decision was solely based on me being massively overweight defense companies.

In fact, I have been bullish on HII for many years, making the case that the pandemic problems it had were just temporary headwinds.

My most recent article on the stock was written on December 6, when I went with the title “Huntington Ingalls Is One Of The Most Underappreciated Dividend Stocks On The Market.”

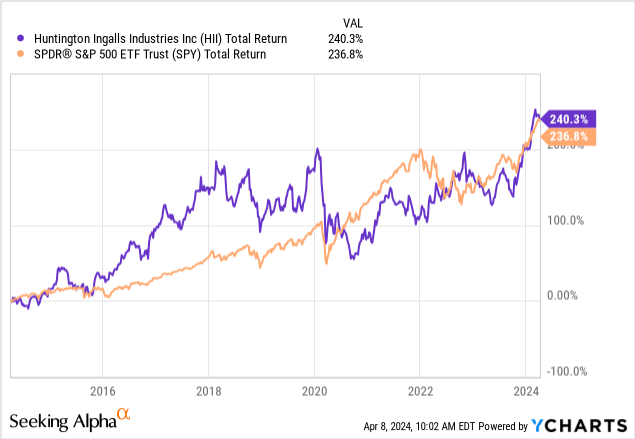

Since then, it has returned 19.4%, beating the 13.5% performance of the S&P 500 (SP500) by roughly 600 basis points.

This also brings HII back on top when it comes to the 10-year performance.

Since April 2014, HII has returned 240%, beating the tech-heavy S&P 500 by a few points.

That’s a fantastic performance, especially when we consider that HII went sideways for roughly four years when pandemic-related issues caused operating challenges.

Now, HII is back, as it benefits from strong demand, a very favorable long-term outlook, improving operations, and a focus on shareholder distributions.

Even better, despite its recent rally, the stock is still attractive, with a high likelihood of prolonged double-digit annual returns.

In this article, we’ll discuss all of this and more.

Huntington Ingalls Is A Special Stock

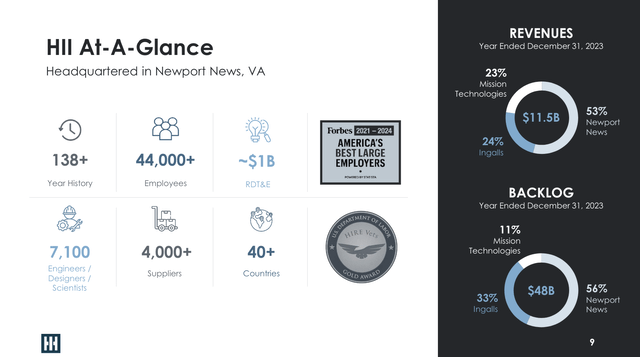

With a market cap of $11 billion, Huntington Ingalls is much smaller than some of its peers, including Lockheed Martin (LMT), RTX Corp. (RTX), and Northrop Grumman (NOC).

However, the company is not less important to America’s armed forces.

Huntington Ingalls Industries

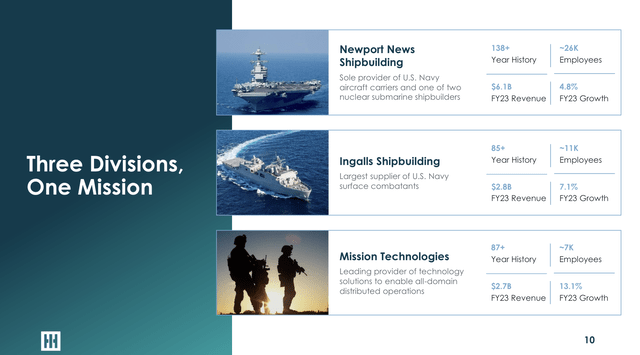

On the contrary, the company, which was spun off from Northrop Grumman in 2011, is the backbone of the Navy. It has close to $50 billion in backlog and generates revenue in three major segments:

- Newport News (53% of 2023 revenues): This segment is the sole provider of U.S. aircraft carriers and just one of two shipbuilders. When it comes to moats, it’s difficult to beat what Huntington Ingalls brings to the table!

- Ingalls (24%): This segment is the largest supplier of Navy surface combatants. In 2023, it grew by 7.1%, beating Newport News by 230 basis points.

- Mission Technologies (23%): This segment has been built over the past few years through M&A that allowed Huntington Ingalls to compete for high-tech projects as well. This includes multi-domain technologies and related services that are increasingly important for America’s defense forces.

Huntington Ingalls Industries

Over the past ten years, HII has invested 4.1% billion in facilities and technologies, spending roughly 5% of its revenues on capital expenditures.

This has allowed the company to position itself for what is likely a very bright future for Navy hardware.

For example, despite recent budget uncertainty, HII is upbeat about defense spending. This is what the company said during last month’s Investor Day:

Now we were extremely pleased to see the President’s budget and the strong support for amphibs. Obviously, that is absolutely critical to our expectations going forward. And so that is a step in the right direction. We were honored to host senior leadership from the Marine Corps just a couple of days ago, and they also, as you would imagine, are in a very good place with respect to that. – HII 2024 Investor Day.

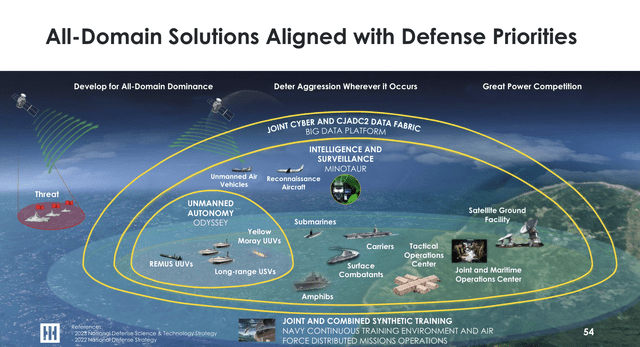

Generally speaking, the company makes the case that as geopolitical tensions escalate and global security threats become more severe, there is an increasing demand for advanced naval vessels and maritime capabilities.

Bear in mind that while a big metal ship may not scream “high-tech” the way an advanced Reaper drone or an F-35 jet does, the Navy allows the U.S. (and its NATO peers) to address security issues anywhere in the world.

Essentially, aircraft carriers are mobile military bases. As bullish as I am on advanced military technology and the new Space Race, the Navy is here to stay.

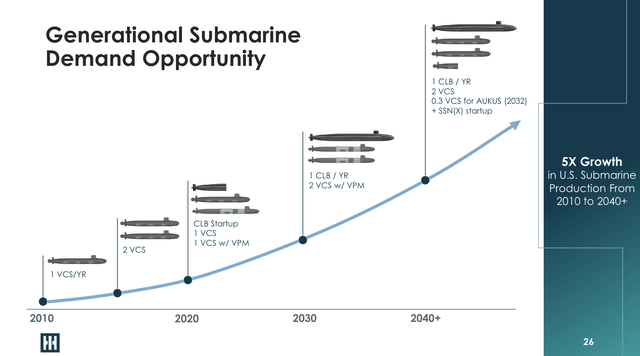

Moreover, the company sees 5x growth in U.S. submarine production beyond 2040.

Huntington Ingalls Industries

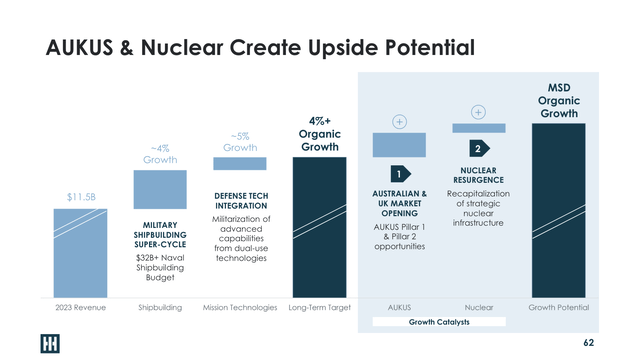

As we can see below, the company expects to achieve more than 4% long-term organic growth, with mid-single-digit growth potential, fueled by AUKUS (a security pact between the U.S., U.K., and Australia) and nuclear subs.

Huntington Ingalls Industries

Regarding my prior nuclear sub comments, Huntington Ingalls has accelerated the hiring process:

As the demand for nuclear-powered submarines increases, Newport News Shipbuilding said it’s working to hire 3,000 skilled trades workers this year and a total of 19,000 within the decade. – HII Press Release.

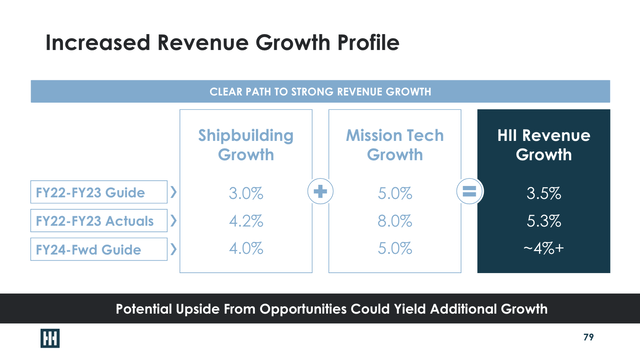

Moreover, the company’s backlog provides visibility for future revenue, with over 75% of projected revenue over the next three years already under contract, and guidance indicating a path to consistent growth in both shipbuilding and mission technologies.

Huntington Ingalls Industries

Even better, Mission Technologies, which is a heavyweight in C5ISR and Cyber & Electronic Warfare, has a 1.9x book-to-bill ratio, which indicates that for every $1.00 in finished work, the segment receives $1.90 in new orders. This is highly supportive of future growth.

Huntington Ingalls Industries

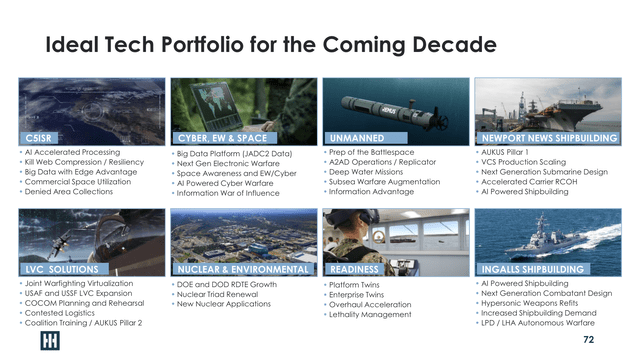

Adding to that, the company is actively pursuing additional growth opportunities, including major construction programs, maintenance and modernization projects, and new business acquisitions.

These opportunities include (but are far from limited to):

- Refitting ships for new technologies, including hypersonic weapons.

- Working on autonomous ships (smaller, mass-produced weapons).

- Renewing the Nuclear Triad.

- Implementing next-gen electronics.

- Applying AI to ships and shipbuilding processes.

- Boosting “big data” applications in C5ISR.

Huntington Ingalls Industries

This may be a silly comparison, but think of HII as a car company, except there are just two car companies (the other is General Dynamics (GD)) that are capable of buying the cars needed for American roads.

HII and GD essentially dominate their industry.

Now, the car industry is going through a rapid transformation. Not only do people need more cars, but they also need to update the cars they have with new technologies.

This is somewhat of a “forced” demand upswing that tremendously benefits HII.

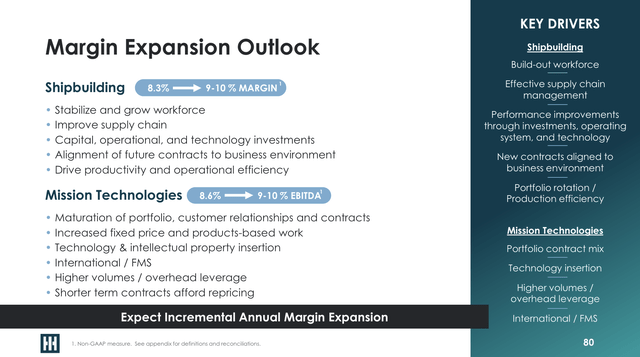

Especially, the technology trends are expected to support ongoing supply chain improvements to significantly grow margins in both shipbuilding and technology segments.

Huntington Ingalls Industries

As one can imagine, this is excellent news for shareholders.

The HII Shareholder Wins

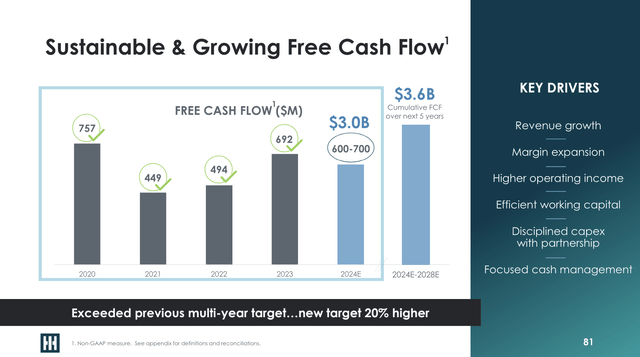

A favorable growth outlook comes with a good outlook for free cash flow.

In the 2020-2024 period, the company is expected to generate $3.0 billion in cumulative free cash flow.

In the 2024-2028 period, free cash flow is expected to be roughly 20% higher at $3.6 billion. This translates to roughly 32% of its current market cap over the entire period and 6.5% per year on average.

Huntington Ingalls Industries

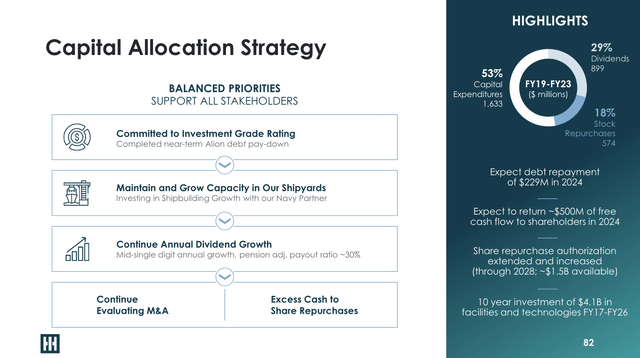

As we can see below, this bodes well for shareholders, as the dividend is a top-three capital spending priority – after maintaining a healthy balance sheet and growing the business.

Huntington Ingalls Industries

Speaking of its balance sheet, in 2021, the company had $3.3 billion in net debt and a 3.3x leverage ratio. It entered this year with $2.5 billion in net debt and a 1.9x leverage ratio.

It also has $430 million in cash (part of net debt) and $1.9 billion in liquidity if we include its revolving credit facility.

Standard & Poor’s rates the company BBB-, which is an investment-grade rating that I expect to be boosted to BBB in the next two years.

Going back to its dividend, investors now face a favorable mix of lower debt, improving growth, and stronger secular tailwinds.

As such, the dividend outlook is good.

Since 2013, we provided an annual dividend, and we’ve increased that dividend each year since then. We guide to mid-single digit annual dividend growth rate with a net pension adjusted income payout ratio of approximately 30%. We’ve increased the dividend in the last 2 years at 5.1% and 4.8%, respectively. – HII 2024 Investor Day (emphasis added).

In other words, 4-7% annual dividend growth should be expected to last on a long-term basis.

Currently, HII pays $1.30 per share per quarter. This translates to a yield of 1.8%.

If we assume that the company generates an average annual free cash flow yield of 6.5%, we’re dealing with a highly favorable sub-30% cash payout ratio.

While HII may not be a high-yielding stock, its free cash flow power is impressive, which also bodes well for buybacks.

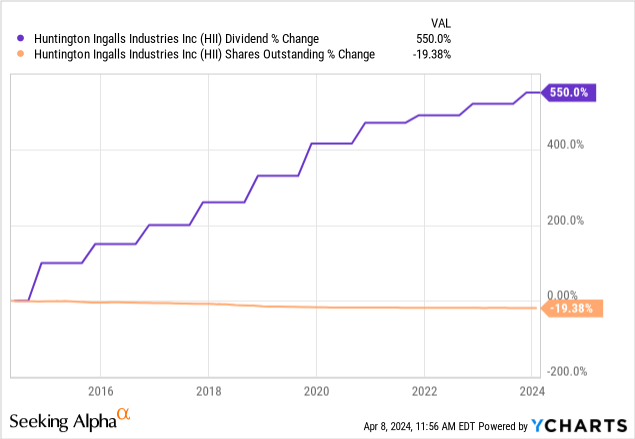

Over the past ten years, HII has bought back 19% of its shares. Going forward, I expect that number to accelerate, as it now has a healthier balance sheet and a more favorable growth outlook.

Valuation

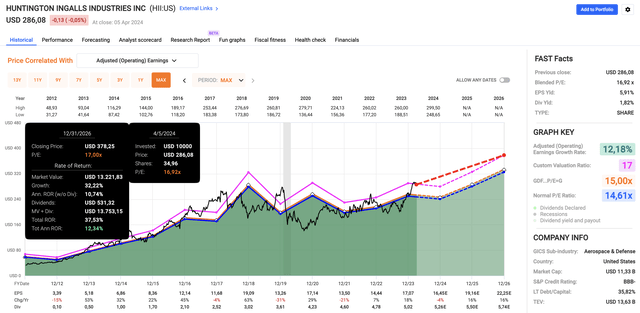

After its recent rally, HII currently trades at a blended P/E ratio of 17x. This is well above its post-spin-off normalized P/E ratio of 14.6x.

However, as I wrote in my prior article, I believe a 17x multiple is fair, as the company has a stronger growth profile. While 2024 is expected to see flattish EPS, both 2025 and 2026 are expected to see 16% EPS growth.

FAST Graphs

When adding its 1.8% dividend, the company has a fair shot at a 12% annual return through 2026 (and likely beyond).

Since 2012, HII has returned 20.6% per year.

However, please note that this is a theoretical annual return. I cannot promise that it will return 12% every single year.

My point is that on a longer-term basis, I expect the annual return to average 12%. This includes some potential corrections and stronger rallies.

The only reason why I do not own HII is that I have close to 25% defense exposure already. Most of my holdings supply technology that is installed in these ships, so HII being upbeat about its future is bullish for most major defense constructors as well.

Takeaway

Investing in Huntington Ingalls offers a compelling opportunity in an often-overlooked niche of the defense industry.

With a track record of resilience and growth, HII stands out as a key player in shaping America’s naval strength.

The company’s focus on innovation, boosted by its strong backlog and strategic investments, sets the stage for sustained shareholder value.

Despite recent gains, HII remains attractively valued, poised to deliver double-digit annual returns.

As geopolitical tensions rise and global security demands escalate, HII’s role in advancing naval capabilities provides for a promising future.

For investors seeking stability, growth, and dividend potential, HII is a standout choice in the defense industry.

Pros & Cons

Pros:

- Steady Growth Potential: Despite temporary setbacks, HII has shown strong growth potential, supported by accelerating demand and a solid backlog.

- Favorable Outlook: With a focus on naval construction and emerging technologies, HII is positioned to capitalize on evolving defense needs.

- Shareholder Returns: A commitment to dividends and buybacks underscores management’s dedication to shareholder value.

- Strategic Positioning: As a key player in naval defense, HII enjoys a huge moat.

Cons:

- Sector Dependency: HII’s success is tied to the defense sector, making it prone to government spending and geopolitical tensions.

- Limited Yield: With a relatively low dividend yield, HII may not appeal to income-focused investors seeking higher yields.

- Operational Risks: HII is very material and labor-intensive. During the pandemic, this was a huge headwind.

Read the full article here