")

Alcoa Corp. (NYSE:AA) is a major producer of bauxite and aluminum products, and it is headquartered in Pennsylvania. Major U.S. banks typically kick off the earnings season, and Alcoa is one of the first non-bank companies to release earnings. This company is set to report Q1 earnings on April 17, 2024, after the market closes. The consensus estimate is for a loss of $0.50, with revenues coming in at $2.52 billion. However, Earningswhispers.com is calling for a loss of just around $0.19 per share for the quarter, which would be a beat over the current consensus estimates. Let’s take a closer look:

My Previous Alcoa Coverage

I wrote a bullish article on Alcoa in 2012, and a bearish article in 2014. However, the analysis of Alcoa has completely changed because these articles were written many years ago and also because Alcoa did a spinoff of Arconic, Inc., in 2016. In addition to these major factors, Alcoa did a 1-for-3 reverse stock split in 2016.

The Chart

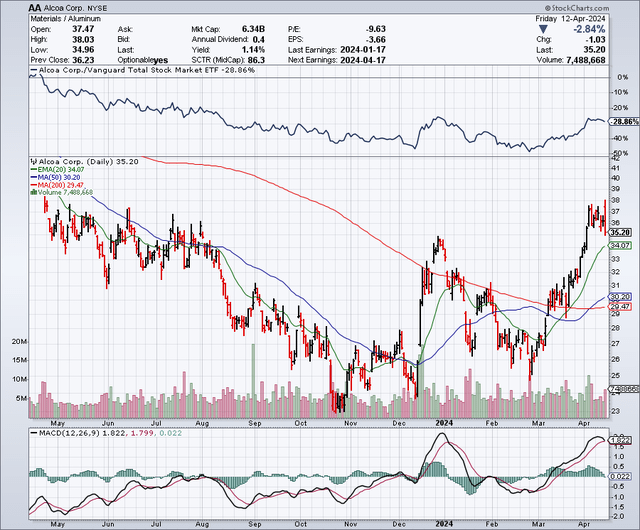

As the chart below shows, Alcoa shares have had a very nice run lately. The stock traded for just around $23 in October, 2023, and it recently touched the $38 level. The 50-day moving average is $30.20, and a “Golden Cross” formation is showing on the chart, since the 50-day is above the 200-day moving average of $29.47. Going into earnings, with this stock now trading significantly above these key support levels, I feel it could be vulnerable to a selloff, even if results are better than expected.

Alcoa.com

The Setup Into Earnings

The market lost about 500 points on April 12th, and last week wasn’t great for stocks overall, but even with a rough week, the stock market has been in rally mode for months now. I expect earnings will be solid to strong for most companies this earnings season. However, it seems that these high expectations might not be enough to keep some stocks from selling off after earnings are reported. For example, Delta Airlines (DAL) reported earnings on April 10, and it beat on both earnings and revenues. The stock rose briefly after this positive earnings report was released, but it dropped and closed down on the day.

In another example, JP Morgan Chase (JPM) released earnings on April 12, and it also beat on both earnings and revenues, yet the stock tanked and closed down about 6.5% for the day. Of course, it did not help that the market dropped by nearly 500 points on that same day (Friday), but I think the bigger issue is that both Delta Airlines and JP Morgan Chase were both overbought and at the top of the recent trading range going into earnings. This created a set up for these stocks to fall when earnings were released, even though the earnings reports were stronger than expected. Alcoa seems to be in the very same situation whereby it might post better than expected earnings, and yet I believe the stock could pullback because it is over-extended after a big run.

On January 17, 2024, Alcoa shares closed at $27.18 and after the market closed, it released fourth quarter results for 2023, which showed a better than expected loss and a beat on revenues. In the next couple of days, the stock traded a bit lower. I think this pattern is likely to repeat when Alcoa releases earnings for Q1, especially with the stock having run up significantly into earnings.

Why Alcoa Shares Jumped In After Hours Trading On April 12th

After the market closed on Friday, April 12th, Alcoa shares jumped by about 5% in the after market hours trading session. This was due to news that the United States and the United Kingdom implemented new rules that prevent top metal exchanges from accepting new supplies of aluminum and other metals, if they are produced by Russia. Furthermore, the United States is banning the importation of aluminum, copper, and nickel from Russia. The stock market reaction suggests this appears to be mildly good news in the short term for Alcoa as well as for other producers in this sector, but it might not have that much impact in the medium to long run. Aluminum (like oil) is a fungible global commodity and Russia is likely to keep selling aluminum on the global markets to some countries just as they have done with oil. So even if Russia sells less to U.S. and U.K based metal exchanges, other countries are likely to pick up the slack such as India and China, which could keep a lid on aluminum prices. This news pushed Alcoa shares up to $37 in the after hours trading session, and might be setting the bar even higher for the stock to maintain this level after earnings are released.

I believe some market participants knew that these restrictions were likely to be announced sooner or later since these had been considered previously. That would explain (at least partially) the big rally the stocks in this sector have enjoyed over the last several weeks. However, as I mentioned before, I don’t think this will translate into a large sustainable price increase for aluminum globally. We might even see a sell on the news reaction, after the initial knee jerk rally to the upside.

The Competition

Alcoa has a number of competitors globally, and some of them are based in United States, including these companies below:

Kaiser Aluminum (KALU) shares are trading for about $89 and have had a huge run in the past several weeks because this stock was trading in the low $60 range in February. Kaiser is a much smaller company when compared to Alcoa, but it is solidly profitable now. Analysts expect this company to earn $3.67 per share in 2024, on revenues of $3.12 billion. For 2025, earnings are expected to rise to $5.75 per share, with earnings coming in at $3.33 billion. As for the balance sheet, Kaiser has about $82.4 million in cash and around $1.09 billion in debt.

Century Aluminum (CENX) shares were trading for about $5 in October 2023. Since then, the stock has more than tripled in value and it now trades for about $17, and even made a new 52-week high on Friday April 12, 2024. Analysts expect Century to earn $0.18 for 2024, on revenues of $1.94 billion. For 2025, earnings are expected to jump to $1.05 per share, with revenues coming in at $2.23 billion.

On the balance sheet this company has $88.8 million in cash and around $481.5 million in debt.

Alcoa Earnings Estimates And The Balance Sheet

Analysts expect Alcoa to post a slight profit for 2024, with earnings estimates at $0.25 on revenues of $10.7 billion. For 2025, earnings estimates are at $2.68 per share, on revenues of $11.15 billion. In 2026, things are expected to get a little more interesting with earnings estimates at $3.45, and revenues coming in at $11.59 billion. This suggests a price to earnings multiple of about 14 times for 2025 earnings, and around 12 times 2026 earnings. This is not a high multiple, but to get to this, you have to go out a year or two and basically ignore 2024 results. Furthermore, a lot can happen in the next year or two; the biggest concern is the potential for a recession or “hard landing” as the Fed tries to maneuver the balance between inflation and interest rate policies. Right now, the soft landing crowd seems confident, but historically the Fed has botched past attempts for a soft landing.

As for the balance sheet, Alcoa has $944 million in cash and $2 billion in debt.

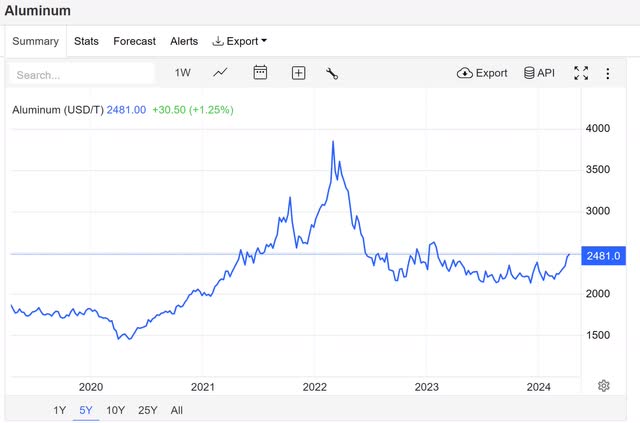

Rising Aluminum Prices Have Made Investors Hopeful

Aluminum prices have been rising over the past few weeks, although pricing is still not much higher than where it was at the start of 2024. Furthermore, as can be seen in the chart below, the price of aluminum is now at a point that could provide resistance. If it can decisively break through the $2,500 per ton, that could fuel upside for Alcoa and the other players.

Alcoa.com

Potential Downside Risks

Weaker than expected economic conditions in China could keep pressure on aluminum prices. In addition, China accounts for about 60% of global aluminum output and Russia is the world’s third largest producer. So, these countries can impact global pricing and create potential downside risks. Alcoa shares are very cyclical, and tend to go higher than anyone expects when demand is strong, and yet also plunge to lows that few expect when recessions occur. A hard landing could send Alcoa shares sharply lower.

In Summary

As discussed above, the stocks in this sector have seen a huge rally over the past several weeks and months. Part of this rally seems to be based on the recent rise in aluminum prices, and I also think market participants were investing on the belief that restrictions would be placed on Russia, which was just confirmed. A significant amount of good news seems to be priced into Alcoa and the other aluminum stocks. While I think Alcoa shares offer intriguing upside in the next economic upcycle, I think there is still a significant risk of subdued economic growth, and even a potential recession. But mostly for now, I am concerned with the fact that this whole sector appears overbought. I also feel that investors have to be cautious with the current set up into earnings. As we saw from Delta and JP Morgan Chase, an earnings beat is not always enough to keep the shares from declining. It is also worth noting that Alcoa beat on earnings January 17, and the stock fell anyhow and at that time it was trading for much less at about $27 per share.

If I was a long term investor in Alcoa, and comfortable with pullbacks, I might hold my position here as long as it was not too large. This sector has momentum and perhaps aluminum prices can continue rising, in the event of a soft landing. But, for more tactical and short term investors, I think this recent rally in the aluminum sector might be an ideal chance to take profits and then buy a dip that could be 10% or even more.

Read the full article here