")

Investment Thesis

Fortive Corporation (NYSE:FTV) should continue to deliver good revenue and margin growth moving forward. The company’s revenue growth should benefit from continued strength in its Intelligent Operating Solutions and Advanced Healthcare Solutions segments. While the Precision Technologies segment has seen some weakness over the last few quarters, some green shoots like stabilizing orders indicate a potential for recovery in the back half of 2024. In addition, the company has a strong balance sheet and a high cash-generative profile, which positions it well to continue supplementing organic growth with accretive M&As.

On the margin front, the company should benefit from operating leverage on higher volumes, cost reduction actions, and productivity initiatives. The stock is trading at a discount to its historical averages. This coupled with good growth prospects makes FTV stock a good buy.

Revenue Analysis and Outlook

I last covered FTV in December where I discussed the company’s revenue growth benefitting from strength in its Intelligent Operating Solutions segment, channel transition completion in the Advanced Healthcare Solutions segment, and accretive M&As. The company recently reported its Q1 2024 results and similar dynamics were seen.

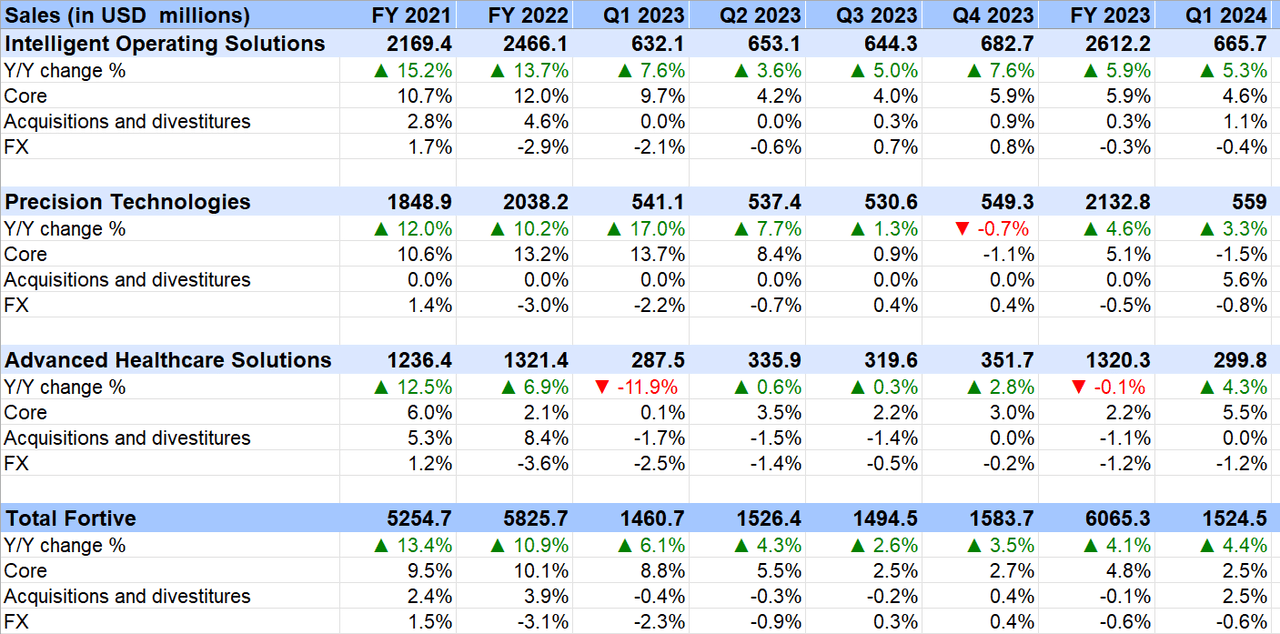

In the first quarter of 2024, the company’s sales increased 4.4% Y/Y to 1.524 billion. Excluding a 2.5% benefit from acquisitions and a 0.6% unfavorable impact from FX translation, core sales grew 2.5% Y/Y in the quarter. Favorable pricing contributed 2.3% to the core sales growth and increased volumes contributed 0.2%.

On a segment basis, the Intelligent Operating Solutions (IOS) segment’s sales rose 5.3% Y/Y with 4.6% core sales growth driven by pricing increases and mid-single-digit core growth across its Connected Reliability (CR), Facility and Asset Lifecycle (FAL), and Environmental, Health and Safety (EHS) businesses.

The Precision Technologies (PT) segment’s sales benefitted from price increases, volume increases in energetic materials, and contributions from the acquisition of EA Elektro-Automatik Holding GmbH (EA). However, these positives were partially offset by the impact of normalizing demand at Tektronix and Sensing businesses and product line divestments at Invetech. As a result, the segment’s sales increased by 3.3% Y/Y while the core sales declined by 1.5% Y/Y.

Lastly, the Advanced Healthcare Solutions (AHS) segment’s sales grew by 4.3% Y/Y and 5.5% Y/Y organically, driven by price increases across the segment and higher volumes in the Advanced Sterilization Products (ASP) business.

FTV’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, I am optimistic about the company’s growth prospects and expect strength in the Advanced Healthcare Solutions (AHS) segment and Intelligent Operating Solutions (IOS) segment to continue and Precision Technologies (PT) segment to see organic growth recovery as well in the coming quarters. Further, the company has strong balance sheet and excellent FCF generation potential which should enable it to pursue inorganic growth which should add to organic growth.

In my previous article, I discussed how a transition from distributor to direct sales model in the U.S. Advanced Sterilization Products (ASP) business was impacting the company’s AHS segment sales. The headwind from transition is now behind and the company has started seeing benefits from its new direct sales model, which I expect to continue driving good growth in the AHS segment in the coming quarters. The IOS segment is also seeing strong growth driven by good demand in the Facility and Asset Lifecycle (FAL) business, especially the company’s SaaS offering, and the segment is also benefiting from the pricing actions.

The only pain point that is worrying investors has been the organic growth in the PT segment. However, I believe the situation is not that bad here, and we should see a recovery in the back half of 2024 and in 2025 in this segment. On the organic revenue basis probably Q2 would mark the bottom, but orders have already started stabilizing and management noted that the total PT segment book-to-bill was ~1x in Q1 and should be around similar levels in Q2. I believe this ~1x book-to-bill for the segment indicates we are close to the bottom.

Management has also noted some green shoots in the segment on the company’s last quarter earnings call. Below are a couple of relevant excerpts.

So we’ve seen some green shoots in some places. I can talk more about that. Things like Tektronix, where our Keithley business, which has tended to lead the effort on the return and was the first to go down, is now going to be high single-digit revenue growth in the first half. So we’re starting to see the things that would certainly point to that trajectory change.”

I would tell you, I was with the China team a week ago. And they’re feeling better about where they were versus, call it, 8 weeks ago when I was with them the first time in the year. They were much more optimistic. We would talk to some of the quality productive forces, investments that China is talking about. So we still have — we still sit right now in our guide, embedded in our guide is China being down. But at the same time, there’s probably some opportunity of some of the Chinese government active investments occur because those are in places that are very subsequent important to us.”

Management also noted that some of the orders that started getting delayed should show up later this year, setting the stage for a recovery of PT segment’s organic revenue in the back half of the year.

I believe a recovery in PT segment sales in the second half should improve investor sentiment around the stock.

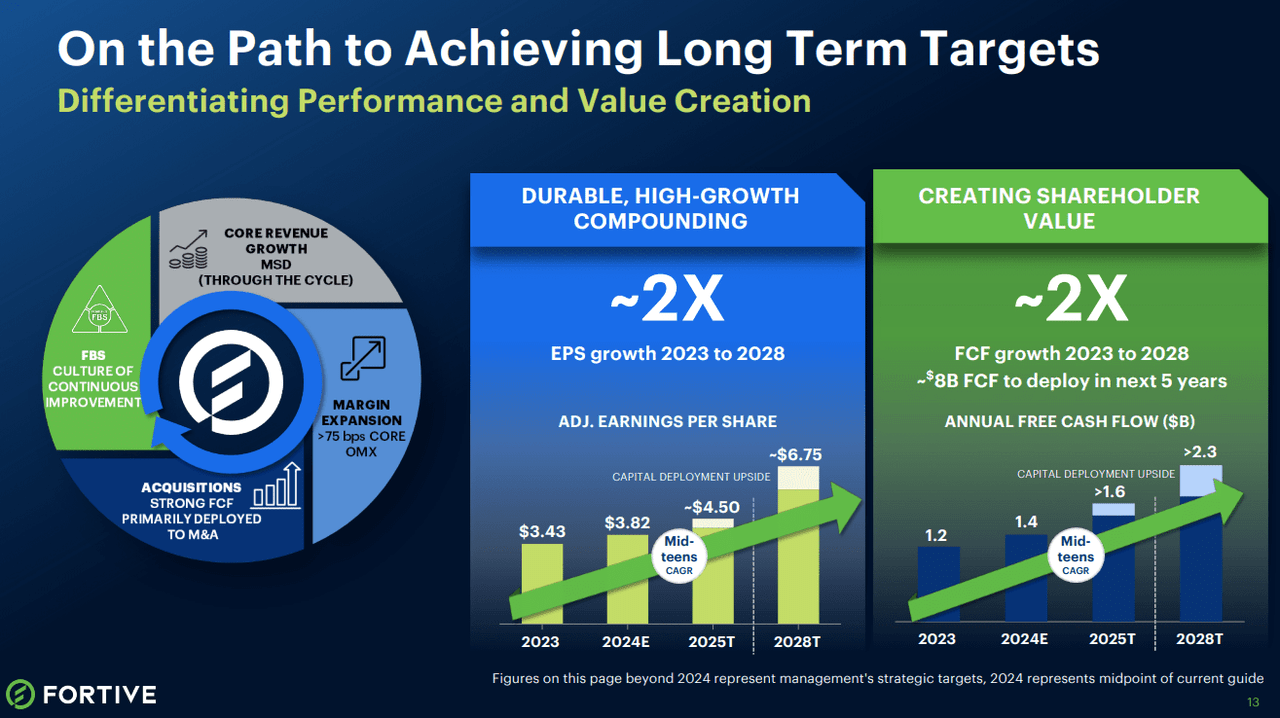

In addition to good organic growth prospects, the company should also benefit from inorganic growth. The company has a strong balance sheet, with net debt to EBITDA as of last quarter end at ~2x. The company also has an excellent cash flow generation profile and management expects $8 bn in FCF in the next 5 years (see chart below).

FTV’s 5-Year Growth Targets (Company’s Q124 Earnings Presentation)

The company has a good history of tuck-in as well as transformative M&As and I expect acquisitions to complement the company’s organic growth. Overall, I am optimistic about the company’s growth prospects.

Margin Analysis and Outlook

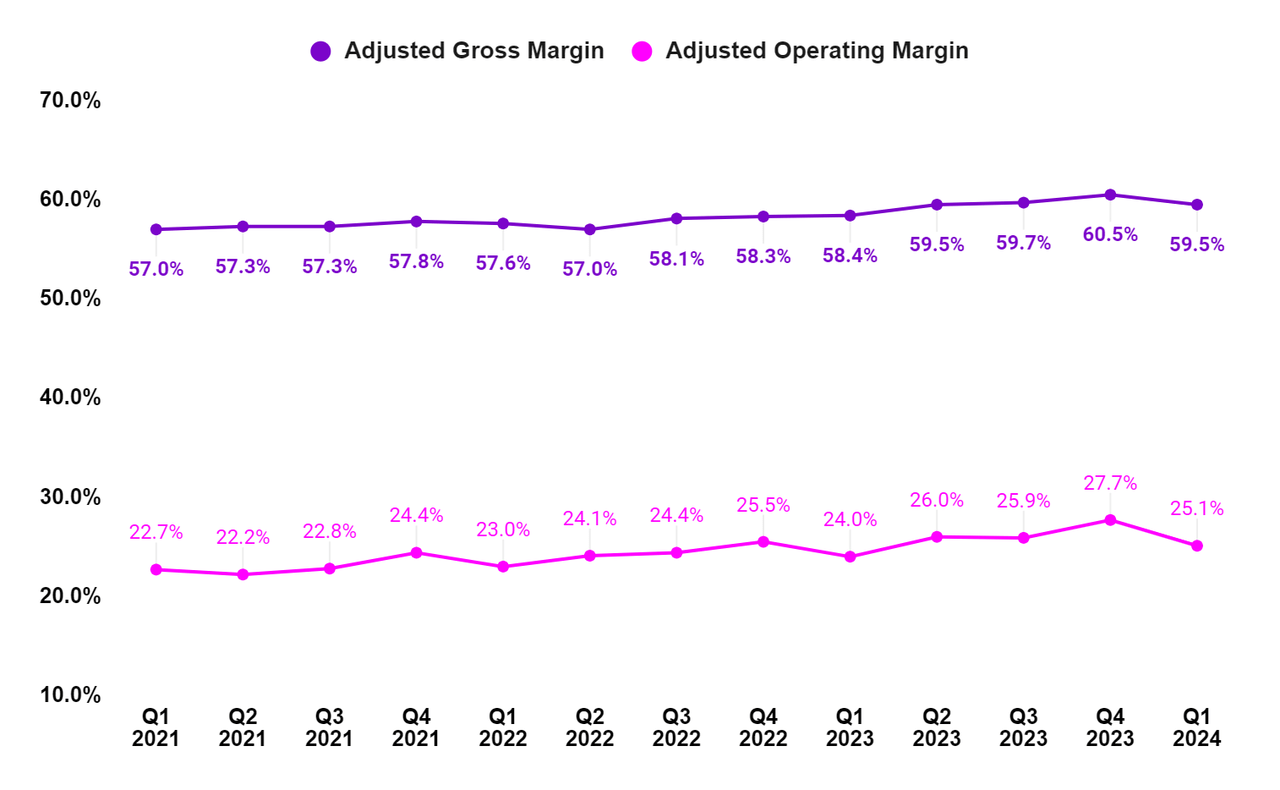

In Q1 2024, the company’s margins benefited from favorable price realization, productivity measures, and Fortive Business System (FBS) initiatives. As a result, the adjusted gross margin expanded by 110 bps Y/Y to 59.5% and the adjusted operating margin expanded by 110 bps Y/Y to 25.1%.

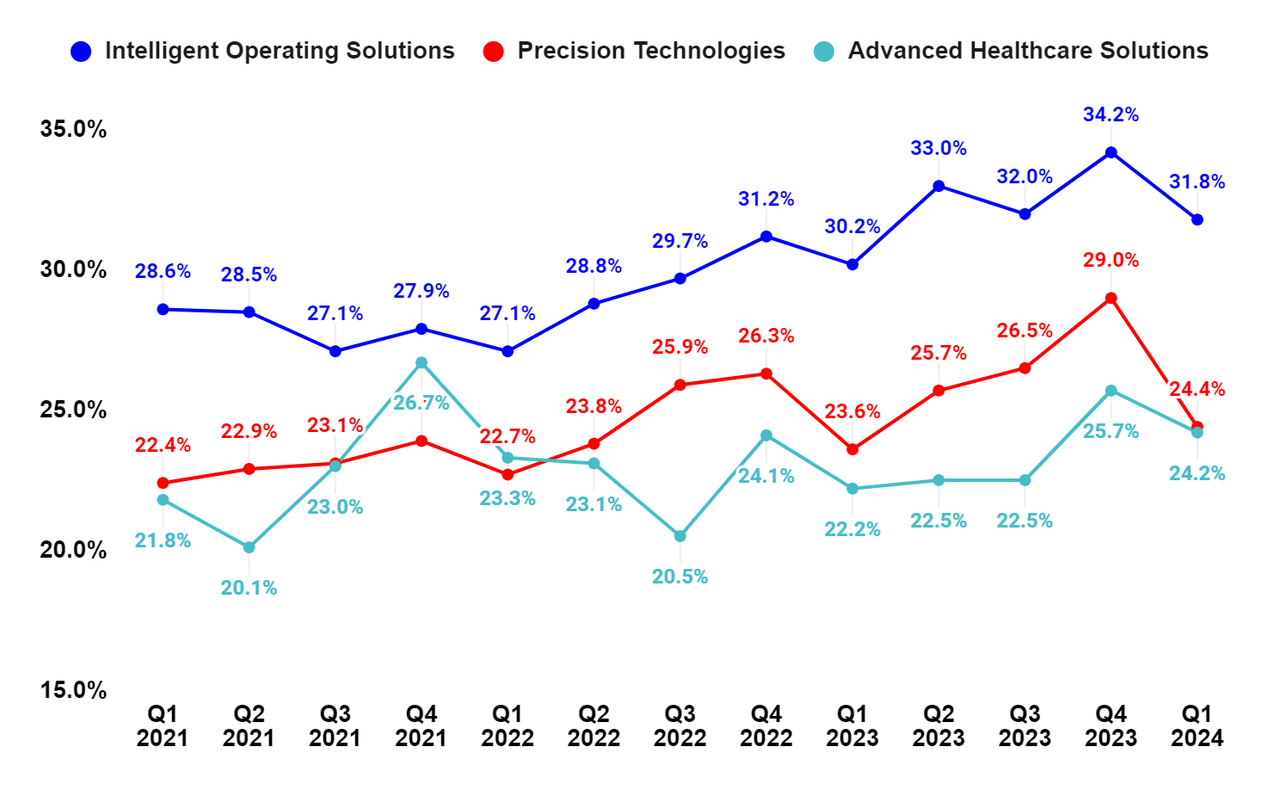

Segment-wise, the adjusted operating margin expanded by 160 bps Y/Y in the Intelligent Operating Solutions, 80 bps Y/Y in the Precision Technologies, and 200 bps Y/Y in the Advanced Healthcare Solutions segments.

FTV’s Adjusted Gross Margin and Adjusted Operating Margin (Company Data, GS Analytics Research)

FTV’s Segment-Wise Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking forward, I expect the company to benefit from operating leverage as sales of the AHS segment and IOS segment continue to remain strong, and PT segment sales also start recovering. In addition to volume growth, management is also seeing benefits from pricing, which should help margin. The company is also doing a good job in terms of productivity initiatives, which is evident from the 80 bps Y/Y improvement in the operating margin it posted in the PT segment despite lower organic sales. The company’s continuous improvement philosophy and focus on cost reduction and productivity initiatives should help drive long-term margin growth.

Valuation and Conclusion

FTV is currently trading at a 19.96x FY24 consensus EPS estimate of $3.81 and an 18.24x FY 25 consensus EPS estimate of $4.17, which is at a discount versus the Company’s 5-year average forward P/E of 22.34x.

One should also note that the current consensus estimates for FY25 do not build in much benefits from accretive M&As. Management has given a target of $4.50 in EPS for FY25 (including acquisitions) and given the company’s strong balance sheet, I expect an upward revision in EPS estimates driven by potential bolt-on M&As.

Overall, the company has good revenue and margin growth prospects. Revenues should continue to increase, driven by strength in the IOS and AHS segments. Further, a potential recovery in the PT segment in 2H 2024 and inorganic growth opportunities from M&As should help the company drive revenue growth in the coming quarters. Margins should also expand with the help of operating leverage, cost reduction, and productivity initiatives. This, coupled with a lower-than-historical valuation, makes FTV stock a good buy.

Risks

I am expecting a recovery in the PT segment. However, if it continues to get delayed, it may negatively impact investor sentiments.

M&As are a key component of the company’s growth strategy. However, inorganic growth is relatively riskier compared to organic growth and there are always risks related to integration missteps, overpaying for an acquisition, and the leverage a company takes to make an acquisition. In case any future acquisition goes wrong, it may negatively impact stock price.

Read the full article here