")

As we entered 2024, I wrote an article on Sixth Street Specialty Lending, Inc. (NYSE:TSLX) and Main Street Capital (MAIN) comparing both BDCs from the fundamental and valuation perspective. The conclusion was clear to me that TSLX had a better risk to reward ratio than MAIN simply because the valuation discount between these two names was roughly ~40% (driven by MAIN’s extraordinary multiple), while the underlying fundamentals were not that different. More specifically, these were the main drivers that motivated me to label TSLX as an attractive investment play:

- The lion’s share of TSLX’s external debt proceeds is subject to rather back-end loaded maturities, which help keep the investment spreads attractive, given that most of these borrowings were attracted at lower interest rates than what can be currently obtained in the market.

- TSLX’s portfolio yield is close to 14.5%, which is not that typical for BDCs that have a huge focus on the first lien structures that are underpinned by rather defensive companies with a favorable track-record in terms of keeping the non-accrual events rare.

- The bulk of portfolio investments are connected to the SOFR component, which enables TSLX to directly capture the benefits of very favorable market conditions.

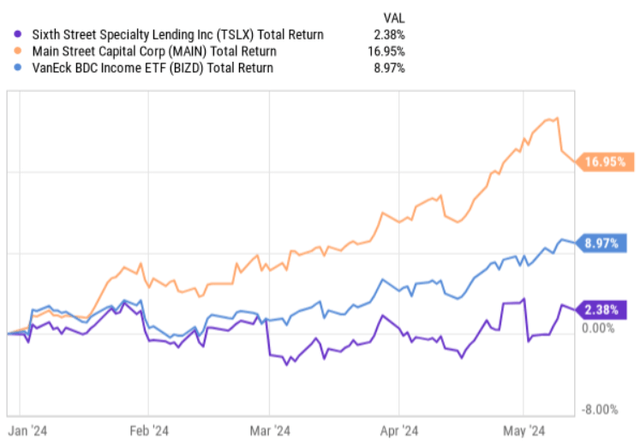

However, if we look at the total return performance so far (on a YTD basis), we will notice that TSLX has significantly lagged behind not only MAIN but also the overall BDC index.

YCharts

Now, earlier in May TSLX issued its Q1, 2024 earnings report, which did not send the stock price higher or lower, hence keeping TSLX’s YTD performance below the index.

Let’s now dissect the earnings report and understand whether there have been some fundamental changes that we have to take into account in the context of the current bull thesis.

Thesis review

If I had to summarize TSLX’s Q1, 2024 earnings report with one word I would go with – stability. In other words, the main metrics measuring the core performance of TSLX came in at stable levels and depending on which comparison we choose (either Q1, 2023 or the previous quarter) there was also some clear signs of growth. For example, the adjusted net investment income per share result landed at $0.58, which is $0.03 per share above the registered level back in Q1, 2023. Yet, compared to Q4, 2023, the adjusted net investment income component declined a bit, mostly due to idiosyncratic factors. However, before we dissect the idiosyncratic factors, I would like to underscore a somewhat negative dynamic that is associated with one important systematic factor.

Q1, 2024 Earnings Report

And by a systematic factor, I mean mostly the general spread compression that is currently taking place across the board in the BDC space. Since the FED brought the interest rates into a restrictive territory, the BDC (private credit) investment yields went up accordingly, which, in turn, triggered a massive interest from the asset managers to consider this specific asset class. As a result of increased flows and thus competition through the formation of fresh BDCs and private credit vehicles, there are just more bidders on the supply that stems from the companies, which seek non-banking credit.

We can observe this also by looking at TSLX’s weighted average total yield on debt and income producing securities metric, which has gone down from 14.3% in Q3, 2023 to exactly 14% this quarter. A decrease of 30 basis points might seem nothing meaningful, but for BDCs, which fund the operations through the use of notable amounts of external leverage, this makes a huge difference.

Now, turning back to a more specific TSLX driver that explained the majority of the registered decline in the net investment income generation this quarter. Here TSLX was forced to recognize a new non-accrual marking down the investment value (and also not recording the corresponding cash flows) in the investment in Astra Acquisition Corp. Besides this non-accrual position, the quality of TSLX portfolio remained unchanged.

What is important to appreciate in the context of TSLX’s investment thesis, is the continued stability at the net investment funding end, which has come in at positive figures for already four quarters in a row. This is not something that is standard in the BDC space as many players have been recently struggling with gaining traction in the market due to a slowdown in the M&A and capital markets activities.

However, during the quarter, TSLX managed to sign new commitments of $264 million from which $164 million were already successfully deployed. This was sufficient to offset the organic quarterly repayments of the existing investments that landed at $109 million this quarter. Furthermore, another important takeaway here is that from these new fundings, 95% were made at the top of the capital structure, focusing on first lien instruments, which implies that TSLX is not deviating from its core strategy just to get the volumes in.

Also, the portfolio metrics still remain robust, where the performance rating of the underlying investments continues to be strong with a rating of 1.15 on a scale of 1 to 5, with 1 being the strongest.

Q1, 2024 Earnings Report

Finally, according to the commentary by Joshua Easterly – CEO & Chairman – in the recent earnings call, the outlook for new fundings is also decent, which is critical for supporting the net investment income generation (i.e., offsetting the margin compression through higher volumes):

I would expect activity levels generally to be up. So I don’t think we saw a little bit of that in Q1, when you look at Alteryx, for example, which was a take private you saw [indiscernible] Co, which was an — M&A, which was a portfolio company, which was a strategic investor owned by a sponsor buying an another strategic asset. So you saw a little bit of that this quarter. I think as volatility in the rates markets subside, and as rates come down a little bit, I think you’ll see more activity.

The bottom line

The key reason why TSLX’s share price has remained flat, while the BDC index has surged higher so far this year is because TSLX has failed to deliver materially stronger results relative to the levels which were achieved in the previous quarter. In fact, during Q1, 2024 TSLX suffered a bit from the general margin compression, where on top of this it was forced to put a notable position under non-accrual (~1.1% of FV).

However, as the portfolio quality remains robust, and the new fundings signed are still in line with TSLX’s conservative strategy, we should expect a gradual growth going forward – especially against the backdrop of expanding portfolio size due to high net investment funding activity. The increase in size through additional first lien exposures should boost the adjusted net investment income generation, helping offset the declining portfolio yields.

So, as a result of these dynamics, I continue to be optimistic about Sixth Street Specialty Lending, Inc’s ability to accommodate the existing dividend yield of ~ 9.7% (including the special distributions). It is a buy for me.

Read the full article here