")

Introduction

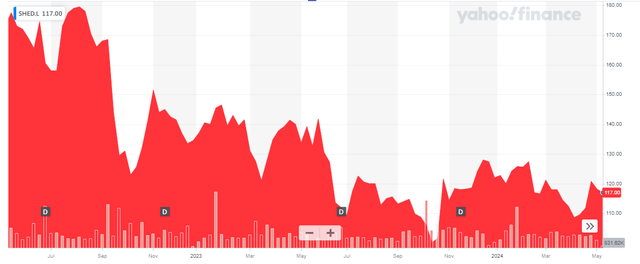

I’m seeing plenty of opportunities in the real estate sector, which has been really beaten down in the past 18 months. Some share price decreases were well deserved, while other REITs were just dragged down with the souring sentiment. The share price of Urban Logistics REIT (OTCPK:PCILF) also went down, but that was somewhat expected given the sharp increase in interest rates on the financial markets.

Yahoo Finance

Urban Logistics has its primary listing in London, where it’s trading with SHED as its ticker symbol. The average daily volume is approximately 1.1 million shares, and this makes it the best market to trade in the REIT’s shares. The current market cap is approximately 550M GBP. I will use the GBP as the base currency throughout this article.

The results are holding up well, but the dividend should have been cut a while ago

When looking at a REIT, I mainly focus on three elements. How are the earnings in relation to the distribution rhythm, how strong is the balance sheet when it comes to LTV ratios and how reliable are the earnings in this era of higher interest rates.

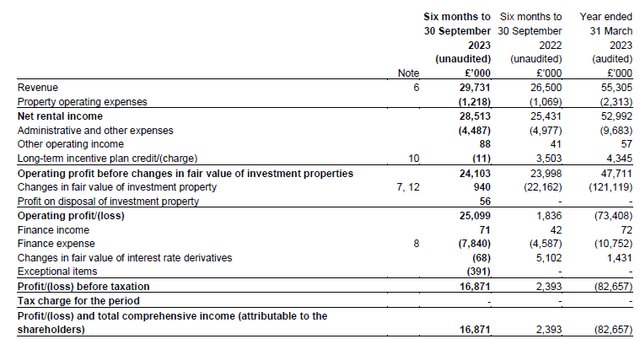

In Urban Logistics’ case, the answer to the first question is pretty straightforward. As shown below, the REIT reported a total revenue of 29.7M GBP (of which 29.3M GBP effectively was the rental income) resulting in a pretty high net rental income of 28.5M GBP. The total G&A expenses decreased (and will likely continue to decrease as a new management agreement with reduced fees is kicking in during the current calendar year) but the total finance expenses increased to 7.8M GBP on the back of higher interest rates as the average cost of debt increased by 88 bp in the first semester of the financial year.

Urban Logistics Investor Relations

While this still resulted in a net profit of 16.9M GBP, the net income (or net loss) is relatively irrelevant for a REIT and the EPRA earnings (comparable to the FFO in North America) provide a better overview of how a REIT actually is performing as it for instance excludes the changes in the assumed fair value of real estate properties.

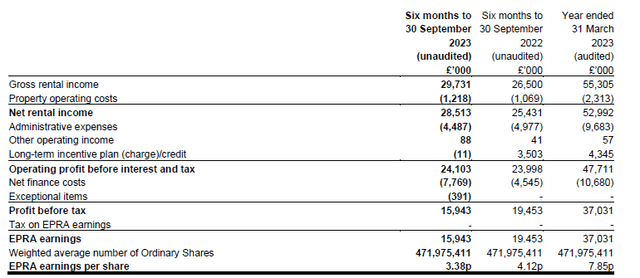

In Urban Logistics’ case, the total EPRA earnings came in at 15.9M GBP, which represents an EPRA earnings of 3.38p per share.

Urban Logistics Investor Relations

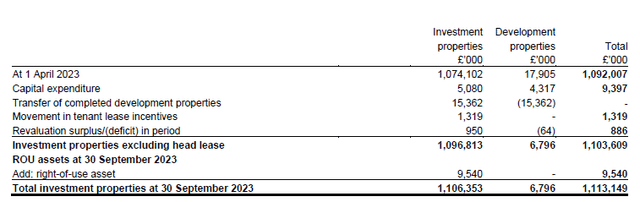

Keep in mind, these earnings still exclude the capital expenditures on the assets. We know the REIT spent in excess of 9M GBP in capex in the first half of the year, but the capex breakdown also shows that in excess of 4.3M GBP of the total capex was related to development assets.

Urban Logistics Investor Relations

This means the pure capex on investment properties was approximately 5.1M GBP. The problem now, of course, is that if we would deduct the 5.1M GBP in property capex from the EPRA earnings, we’d be left behind with just under 11M GBP or 2.3 pence per share in adjusted EPRA earnings.

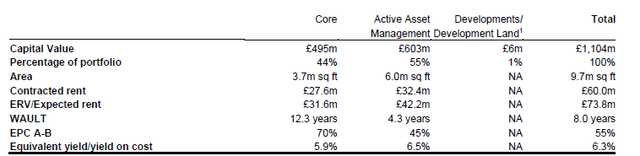

That’s disappointing, but there’s a mitigating factor as the REIT’s earnings will increase sharply as leases expire, and existing leases are up for renewal. As you can see below, while the current contracted rent is just 60M GBP, the Expected Rental Value (‘ERV’) based on current market conditions is almost 74M GBP, 13.8M GBP higher.

Urban Logistics Investor Relations

This means that if I would assume the total capex to remain stable at 5M GBP per semester, the increasing rental income would more than cover the capex and even add about 0.40 pence in EPRA earnings at which point the EPRA earnings after non-development capex would come in at around 7.6-7.8 pence per share.

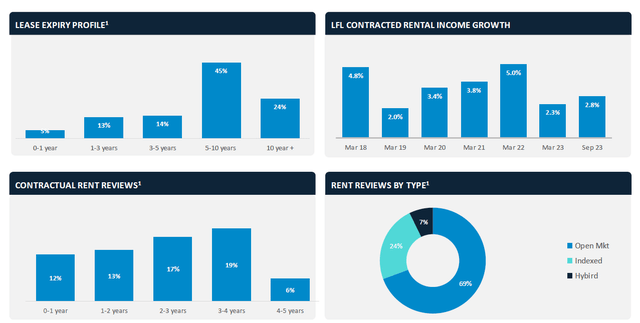

There’s one caveat here. It will take time for the REIT to push through the rent hikes. As you can see below, only 25% of the rents are up for contractual rent reviews in the next two years, while the long WAULT also works against the REIT as less than 20% of the leases are expiring in the next three years.

Urban Logistics Investor Relations

So, while I am very confident the rental income will increase, it will take a while to see the full effect. And while the EPRA earnings will likely continue to cover the current dividend of 7.6 pence per share per year, the payout ratio is uncomfortably high as it will hover around 100% of the EPRA earnings and about 105-110% of the adjusted earnings.

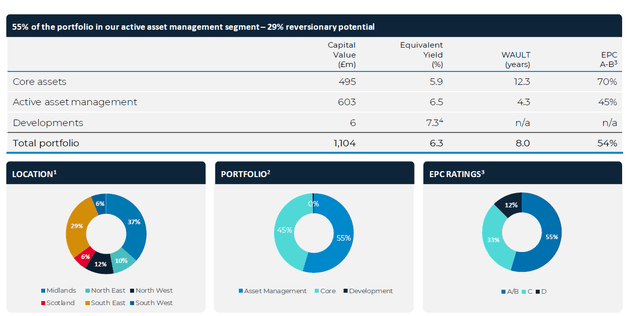

Fortunately, the balance sheet can handle this as the LTV ratio remains below 30% as the REIT borrowed a total of 354M GBP but has almost 31M GBP in cash on its balance sheet. This results in a pro forma net debt position of 323M GBP which, compared to the 1.11B GBP real estate portfolio, represents an LTV ratio of just over 29%. Excluding the 9.5M GBP in lease assets, the LTV ratio is approximately 29.2-29.3%.

Urban Logistics Investor Relations

It obviously is an important question to see the capitalization rate used by Urban Logistics to value the assets at 1.11B GBP. The image below shows the annualized net rental income right now is approximately 57M GBP, resulting in a 4.9% net initial yield and a 5% topped-up yield.

Urban Logistics Investor Relations

While that’s pretty low in an environment where the five-year UK GILT is yielding 4.1%, using the current market rent offset by the current appraisal value of the real estate portfolio indicates the book value of the assets implies a 6.25% capitalization rate on the market rent of the properties, and that’s acceptable for logistics assets. This appears to be fair as subsequent to the end of the final quarter of its financial year, Urban Logistics sold another asset at a 1.9% premium to its net book value.

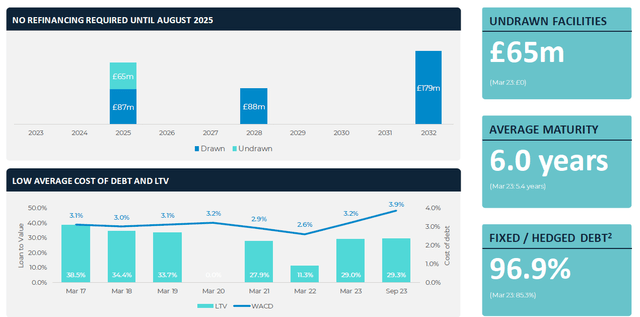

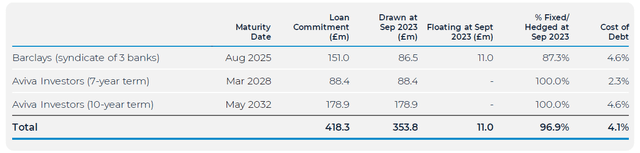

I don’t expect to see any negative surprises to the earnings results, as I think the average cost of debt will at least remain stable in the foreseeable future. The REIT used the proceeds of the sale of some smaller assets to pay down the variable component of its debt, and as you can see below, 267M GBP of the debt has been locked in at 2.3% for the 2028 term loan and an average of 4.6% for the 2032 term loan. This means the interest expense visibility is excellent all the way up to 2028.

Urban Logistics Investor Relations

The 2025 Barclays loan will have to be refinanced in August 2025, but as the average cost of that facility is currently 4.6%, I don’t expect a massive negative impact. Even if the refinancing rate would be 150 bp higher, the total impact would be just 1.3M GBP (and this will likely be offset by rent hikes between now and the summer of 2025).

Investment thesis

I’m between a rock and a hard place when it comes to Urban Logistics Properties. I like the robust balance sheet with a low LTV ratio, and although the current capitalization rate is pretty low, applying the market rent to the portfolio results in an acceptable capitalization rate which means the NTA per share of 161.69 pence is reliable. The current dividend yield of 6.5% (subject to the 20% UK dividend withholding tax on distributions from REITs) is attractive, but investors are warned the payout ratio currently (slightly) exceeds 100%.

That being said, the stock is trading at about 15 times its EPRA earnings, and although the EPRA earnings will likely increase by approximately 40%-45% based on the current market rents. While that sounds great, let’s not forget the EPRA earnings don’t include capex, so the net underlying result including capex will be a bit lower.

I currently have no position in Urban Logistics Properties. It’s a well-managed REIT, but I hope the stock may get a bit cheaper in the near future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here