")

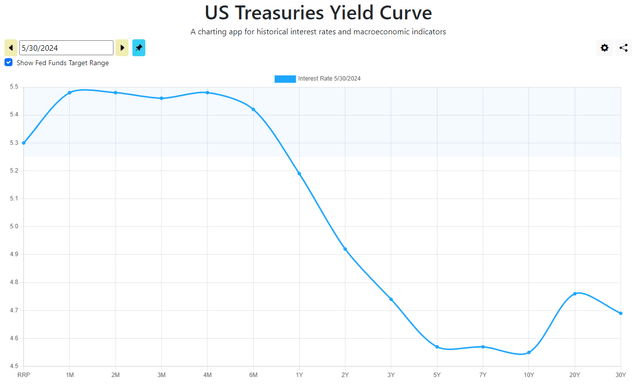

The Nuveen Variable Rate Preferred & Income Fund (NYSE:NPFD) is a closed-end fund (“CEF”) that can be employed by income-seeking investors as a way of achieving their goals. As the name of the fund suggests, this is a preferred stock fund, just like many others that we have discussed in this column. However, this fund invests in securities that make dividend payments to their owners that change based on interest rates. This is something that might be very appealing today, since the yield curve is inverted (and has been since July 2022):

USTreasuryYieldCurve.com

The reason why this is important is that it means that assets with a dividend or coupon that is based on short-term rates will have a much higher yield than assets whose dividends or coupons are based on long-term rates. As we will see in this article, the yield of variable-rate preferred stock depends on short-term interest rates instead of long-term interest rates like ordinary preferred stock. As such, we can expect that this fund will have a much higher yield than many other preferred stock funds.

Curiously, though, that is not the case as the Nuveen Variable Preferred & Income Fund currently yields 8.27%. This is not nearly as high as the 11%+ yields sported by variable-rate debt funds right now. However, it does compare very well with other preferred stock funds:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Nuveen Variable Preferred & Income Fund |

Fixed Income-Taxable-Preferreds |

8.27% |

|

Cohen & Steers Limited Duration Preferred & Income Fund (LDP) |

Fixed Income-Taxable-Preferreds |

7.92% |

|

First Trust Intermediate Duration Preferred & Income Fund (FPF) |

Fixed Income-Taxable-Preferreds |

9.41% |

|

Flaherty & Crumrine Preferred Securities Fund (FFC) |

Fixed Income-Taxable-Preferreds |

7.32% |

|

John Hancock Preferred Income Fund (HPI) |

Fixed Income-Taxable-Preferreds |

9.03% |

|

Nuveen Preferred & Income Opportunities Fund (JPC) |

Fixed Income-Taxable-Preferreds |

7.97% |

We can see that the Nuveen Variable Preferred & Income Fund does have a slightly higher yield than many of the funds on this list, but it is not the highest. However, it is notable that this fund actually increased its distribution in December 2023 and again in March 2024, so that sets it apart from many of these other funds that have seen their distributions either remain stable or decline over the past two years. That is something that anyone who is trying to use their portfolio to cover the rapidly rising cost of living might appreciate.

The Nuveen Variable Preferred & Income Fund has an inception date of December 15, 2021, so we cannot look at its performance over an extended period as we can with most other closed-end funds. However, the fund’s performance since its inception has been nothing short of disappointing. As we can see here, the fund’s shares have declined by 30.64% since the fund started trading:

Seeking Alpha

It is worth noting though that this fund had perhaps the worst possible inception date. Long-term yields started rising in November 2021 as the market realized that interest rates would not remain at 0% indefinitely. At the March 2022 meeting of the Federal Open Market Committee, the Federal Reserve proved that the market was correct and started to raise interest rates and embark on monetary tightening. These two activities pummeled fixed-income prices, and we can see that the ICE Exchange-Linked Preferred & Hybrid Securities Index (PFF) also declined by 18.75% over the period. Most other preferred stock closed-end funds also experienced price declines over the period, but as we can see here, there was only one of the fund’s peers that performed as badly as this one did:

Seeking Alpha

The worst-performing fund was the Flaherty & Crumrine Preferred Securities Fund, which makes sense because of the incredibly high level of leverage that that fund employs. The remaining peer funds outperformed the Nuveen Variable Preferred & Income Fund over the period. That is something that might be a turn-off for any potential investor.

However, in a recent article, I stated:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

When we include the distributions that the Nuveen Variable Preferred & Income Fund paid out since its inception, it still underperformed all but one of its peers:

Seeking Alpha

As we can see here, investors in every one of these funds has lost money overall since mid-December 2021. However, the John Hancock Preferred Income Fund has since managed to get very close to making its investors even. It is the best-performing fund in the category over the period, and the only one of these funds to get anywhere close to fully erasing the losses suffered from the implementation of the Federal Reserve’s monetary tightening regime. The Nuveen Variable Preferred & Income Fund continues to be a laggard, as it has only managed to outperform the Flaherty & Crumrine Preferred Securities Fund since its inception.

That is actually rather surprising, since we would ordinarily expect variable-rate securities to outperform fixed-rate securities during periods of rising interest rates. After all, the star performers of the closed-end fund world since late 2021 have been leveraged loan funds that invest in variable-rate debt. A possible explanation can be found in the fact that the net asset value of the Nuveen Variable Preferred & Income Fund only declined by 19.92% since inception. Thus, at least part of the fund’s disappointing performance was driven by the market selling off its shares far more than was justified by the actual performance of the portfolio. However, this situation still bears investigation, since we would normally expect a fund that invests in variable-rate securities to have a lot less interest rate risk than we are actually seeing in its performance.

About The Fund

According to the fund’s website, the Nuveen Variable Preferred & Income Fund has the primary objective of providing its investors with a high level of current income and total return. The current income objective, at least, makes a lot of sense given the fund’s strategy. As is usually the case for Nuveen closed-end funds, the strategy is explained in great detail on the website:

The Fund seeks to provide a high level of current income and total return by investing in primarily investment grade, variable rate preferred securities and other variable rate income-producing securities from high quality, highly regulated companies such as banks, utilities and insurance companies. All, or almost all, of the Fund’s distributions are expected to be treated as qualified dividend income which is ordinarily taxed at a lower rate than interest and ordinary dividend income, assuming holding period and certain other requirements are met.

The Fund may invest up to 20% of Managed Assets in contingent capital securities or contingent convertible securities and up to 15% in companies located in emerging market countries but will only invest in U.S. dollar denominated securities. More than 25% of Managed Assets will be invested in securities of companies in the financial services sector.

The Fund uses leverage and has a 12-year term with the potential to convert to perpetual.

This quote outright states that the majority of the fund’s assets will be invested in variable-rate preferred securities. This certainly matches up with the fund’s name. The fund’s semi-annual report states that the fund’s asset allocation on January 31, 2024, was this:

|

Asset Type |

% of Total Investments |

|

Institutional Preferreds |

66.8% |

|

Contingent Capital Securities |

16.7% |

|

Retail Preferreds |

15.6% |

|

Corporate Bonds |

0.9% |

|

Repurchase Agreements |

0.0% |

That is a bit different from what we might expect from the fund’s name due to the significant allocation to contingent capital securities. These are securities that might not be familiar to many American investors, but thankfully Nuveen offers a helpful primer on its website. Here is a brief description from Nuveen’s site:

CoCos are hybrid securities created by regulators after the 2007-2008 global financial crisis as a way to reduce the likelihood of government-orchestrated bailouts. Issued primarily by non-U.S. banks, CoCos are designed to automatically absorb losses, thereby helping the issuing bank satisfy Additional Tier 1 and Tier 2 regulatory capital requirements.

…

But why are CoCos “contingent”? Because of a feature that automatically imposes a loss on the investor should an issuer’s capital fall below a predetermined threshold – typically 7% of its total risk-weighted assets in a “high trigger” structure and 5.125% in a “low trigger” structure.

As is the case with preferred stocks, contingent capital securities are a hybrid of both common stock and bonds. European banks frequently issue these securities, while American banks issue preferred stock. Thus, many preferred stock funds will include these securities unless it is a domestic-only closed-end fund (and most preferred stock closed-end funds are global funds).

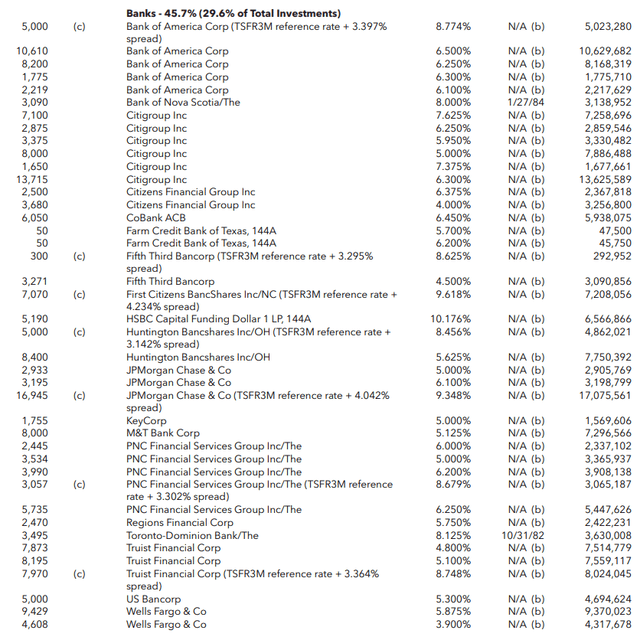

The most surprising thing that I noticed when looking through the fund’s Schedule of Investments is that the overwhelming majority of its assets are in fixed-rate securities, not variable-rate securities. For example, take a look at the institutional preferred stock issued by banks that this fund held on January 31, 2024:

Fund Semi-Annual Report

Along with these two preferred stock issues:

Fund Semi-Annual Report

Only seven of the issues on this list are variable-rate preferred stock. Anything that lists a reference rate is a variable-rate security. This is a huge departure from the fund’s claim that it invests primarily in variable-rate securities. In fact, a look at the whole portfolio reveals that the handful of variable-rate issues that we see in the screenshots above constitute nearly all the variable-rate securities that this fund currently holds. This explains why the fund’s performance has resembled that of a regular fixed-rate preferred stock closed-end fund over the past few years. In short, do not let the fund’s description mislead you. The majority of this fund’s assets look to be fixed-rate securities, and as such the fund has more interest-rate risk than most investors would expect.

It does not appear likely that the fund will alter its portfolio to favor variable-rate preferred stock anytime soon. It only has a 17.00% annual turnover, which is largely in line with its peers:

|

Fund Name |

Portfolio Turnover |

|

Nuveen Variable Preferred & Income Fund |

17.00% |

|

Cohen & Steers Limited Duration Preferred & Income Fund |

49.00% |

|

First Trust Intermediate Duration Preferred & Income Fund |

39.00% |

|

Flaherty & Crumrine Preferred Securities Fund |

9.00% |

|

John Hancock Preferred Income Fund |

29.00% |

|

Nuveen Preferred & Income Opportunities Fund |

15.00% |

(All figures from the most recent annual report for each fund.)

As we can clearly see, the fund’s annual turnover is lower than the peer median of 23.00%, which implies that this fund is not doing a lot of trading or making frequent changes to its portfolio. It is also not running up high trading expenses. However, the fund did have a 4.46% expense ratio in its most recent fiscal year, so that will undoubtedly seem very high to anyone who is used to the sub-1.0% ratios possessed by most index exchange-traded funds. The majority of those expenses were due to high-interest expenses from the fund’s leverage, though. Excluding the leverage, the fund had a 1.58% expense ratio. This is a bit high when compared to the fund’s peers:

|

Fund Name |

Expense Ratio (excluding leverage) |

|

Nuveen Variable Preferred & Income Fund |

1.58% |

|

Cohen & Steers Limited Duration Preferred & Income Fund |

1.38% |

|

First Trust Intermediate Duration Preferred & Income Fund |

1.42% |

|

Flaherty & Crumrine Preferred Securities Fund |

0.98% |

|

John Hancock Preferred Income Fund |

1.30% |

|

Nuveen Preferred & Income Opportunities Fund |

1.58% |

(All figures as of the most recent fiscal year for each fund.)

As we can see, the only fund whose expense ratio comes anywhere close to that of the Nuveen Variable Preferred & Income Fund is the other Nuveen fund. The fund’s peers from other fund houses all have much lower baseline expense ratios. We might be able to excuse this if the fund were outperforming its peers, but as we saw earlier in the article, that is not the case. Thus, the expenses seem rather high and unjustified here.

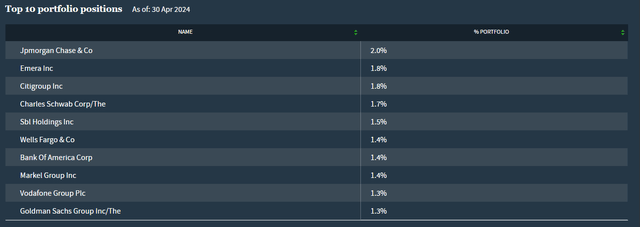

The strategy description that the Nuveen Variable Preferred & Income Fund provides on its website specifically states that it invests in both American and foreign companies, and the large allocation to contingent capital securities reinforces that statement as these securities are not often issued by domestic companies. However, nearly all the largest positions in the fund are American firms. Here are the largest issuers whose securities are represented in this fund as of April 30, 2024:

Nuveen Investments

Emera (OTCPK:EMRAF) is Canadian and Vodafone Group (VOD) is from the United Kingdom, but the rest of the companies shown here are all domestic firms. Thus, we see a marked preference for American companies here. This extends across the remainder of the fund, as only 30.6% of the fund’s assets are currently invested in foreign companies:

Nuveen Investments

In a few recent articles, such as this one, I discussed the importance of diversifying your assets away from the United States. The Nuveen Variable Preferred & Income Fund does not appear to be a great way to do that, given that it is heavily weighted to domestic entities. The fund also explicitly states that it does not invest in non-U.S. dollar-denominated securities, so we do not get the benefits of holding foreign assets from our long-term thesis regarding a declining dollar. This is not necessarily the end of the world as we still do want to have some exposure to the U.S. dollar as well as the domestic economy, but this fund by itself does not appear to offer much foreign exposure. As such, that needs to be considered when constructing your overall income portfolio.

Leverage

As is the case with most closed-end funds, the Nuveen Variable Preferred & Income Fund employs leverage as a method of boosting the effective yield that it earns from its portfolio. I explained how this works in a number of previous articles on other closed-end funds. To paraphrase myself:

Basically, the fund borrows money and then uses that borrowed money to purchase preferred stock and other income-producing assets. As long as the yield that the fund receives from the purchased assets is higher than the interest rate that it has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, it is important to note that this strategy is less effective at boosting effective portfolio yields today than it was a few years ago. This is because the difference between the rate at which the fund borrows money and the yield that it receives from the purchased assets is narrower than it was back when interest rates were essentially zero.

Unfortunately, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally prefer that a closed-end fund’s leverage remain below a third as a percentage of its assets for this reason.

As of the time of writing, the Nuveen Variable Preferred & Income Fund has leveraged assets comprising 36.94% of its portfolio. Obviously, this is a bit above the one-third of assets levels that we would normally prefer a closed-end fund to possess. However, many funds that invest in either debt or preferred stock have higher leverage than the one-third of assets preferred level.

Let us compare this fund to its peers in an attempt to determine whether its leverage is too high for its strategy:

|

Fund Name |

Leverage Ratio |

|

Nuveen Variable Preferred & Income Fund |

36.94% |

|

Cohen & Steers Limited Duration Preferred & Income Fund |

33.70% |

|

First Trust Intermediate Duration Preferred & Income Fund |

33.88% |

|

Flaherty & Crumrine Preferred Securities Fund |

39.50% |

|

John Hancock Preferred Income Fund |

37.98% |

|

Nuveen Preferred & Income Opportunities Fund |

38.83% |

(All figures from CEF Data.)

As we can immediately see, the Nuveen Variable Preferred & Income Fund has a higher level of leverage than a few of its peers. In particular, the fund’s leverage is higher than both the Cohen & Steers Limited Duration Preferred & Income Fund and the First Trust Intermediate Duration Preferred & Income Fund. However, it is not completely out of line with all of them, and there are several peer funds that have higher levels of leverage. In particular, the top-performing John Hancock Preferred Income Fund is using more leverage.

Overall, this tells us that the leverage currently being used by the Nuveen Variable Preferred & Income Fund is not excessive for its particular strategy. Risk-averse investors probably do not need to lose much sleep here, at least not when it comes to the fund’s use of leverage.

Distribution Analysis

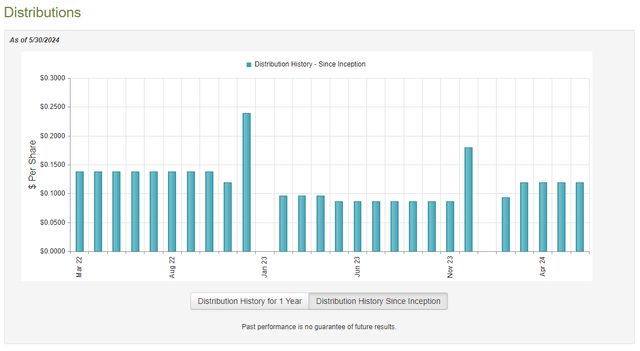

The primary objective of the Nuveen Variable Preferred & Income Fund is to provide its investors with a high level of current income. Accordingly, it pays a monthly distribution of $0.1195 per share ($1.434 per share annually) to its shareholders. Despite the fund’s short history, the distribution has exhibited some variation:

CEF Connect

We can see that the fund cut its distribution in November 2022 and twice more in 2023. This was almost certainly due to the difficult market for fixed-income securities and bank preferred stock that were caused by tighter monetary policy. However, the fund has since started to raise its distributions, with increases in both December 2023 and February 2024. This might be due to the gains that the fund was able to realize in late 2023 as the market pushed up the price of pretty much everything.

Of course, the fund’s ability to sustain its distribution going forward is likely to be the most important thing for prospective buyers today. So, let us take a look at the fund’s finances.

As of the time of writing, the most recent financial report for the Nuveen Variable Preferred & Income Fund is the semi-annual report that corresponds to the six-month period that ended on January 31, 2024. A link to this report was provided earlier in this article. This is a pretty new report, so the information provided in it should give us a good idea of where the fund’s finances stand today.

For the six-month period that ended on January 31, 2024, the Nuveen Variable Preferred & Income Fund received $4,732,758 in dividends and $15,728,020 in interest from the assets in its portfolio. From this amount, we need to subtract the money that the fund paid in foreign withholding taxes. This gives the fund a total investment income of $20,443,514 for the period. It paid its expenses out of this amount, which left it with $8,548,713 for the period. That was not enough to cover the $12,879,487 that the fund paid out in distributions over the six-month period.

The fund was able to make up the difference via capital gains. For the six-month period, the Nuveen Variable Preferred & Income Fund reported net realized losses of $6,114,526, but these were more than offset by net unrealized gains of $34,871,518. Overall, the fund’s net assets increased by $24,426,218 after accounting for all inflows and outflows during the period.

Thus, the fund did technically manage to cover its distributions fully during the most recent period. However, we can see that it was only able to do so because of net unrealized gains. Net unrealized gains can be erased by any market correction, so we should keep an eye on this fund. As I discussed in a previous article, interest rates might remain higher for longer than is currently priced into the market, so it is possible that we will see a correction reduce the value of the assets held by this fund decline and erase some of the buffer that it currently has regarding distribution coverage.

Valuation

Shares of the Nuveen Variable Preferred & Income Fund currently trade at a 12.89% discount to net asset value. This is not as attractive as the 14.05% discount that the shares have averaged over the past month, but it is still a reasonable discount.

Conclusion

In conclusion, the Nuveen Variable Preferred & Income Fund appears to have a lot more interest-rate risk than it should be, based on the fund’s claimed strategy. The fund does not have nearly as much exposure to variable-rate securities as one would expect, given the name and the strategy description on its website. It has also been one of the worst-performing preferred stock closed-end funds since its inception, and its yield is only average compared to peers. The fund does have a reasonable discount on its shares and appears to be fully covering the distribution, but honestly, I cannot see a good reason to purchase this fund over one of the better-performing ones in the same category.

Read the full article here