")

Elevator Pitch

I assign a Hold investment rating to Tuniu Corporation (NASDAQ:TOUR). My view of TOUR as a potential investment is mixed. On one hand, Tuniu has recorded its maiden quarter of GAAP profitability in Q1 2024 and its potential buyback yield is at a high-single digit percentage level. On the other hand, TOUR’s actual Q2 and full-year top line might fall short of expectations due to multiple factors like a high base last year and a decline in per-capita travel spending.

Company Description

On its investor relations website, Tuniu calls itself an “online leisure travel company in China” which provides “packaged tours” and “travel-related services.”

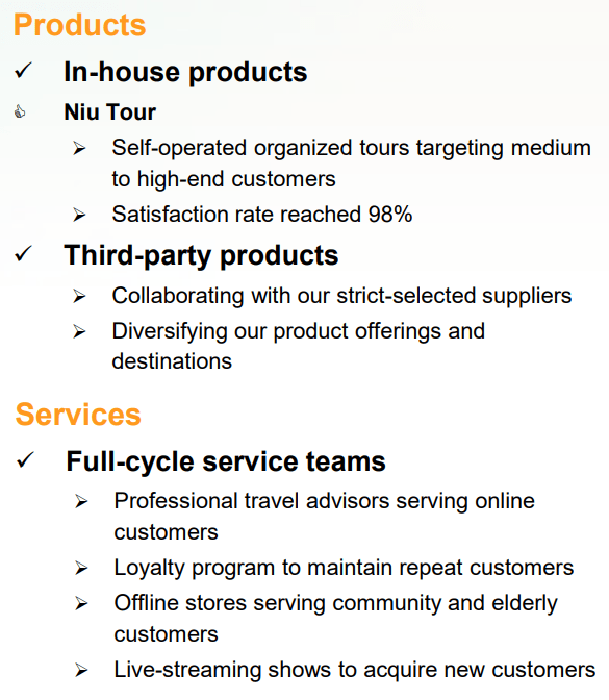

TOUR’s Offerings At A Glance

Tuniu’s Corporate Factsheet

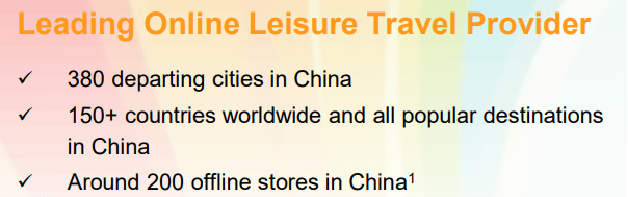

An Overview Of Tuniu’s Travel Coverage And Network

Tuniu’s Corporate Factsheet

In the most recent fiscal year or FY 2023, TOUR derived 76% and 24% of its top line from packaged tours and other travel offerings, respectively as disclosed in its 20-F filing. The company also generated its entire revenue from its home market, China, in the previous year.

Reaching Profitability Inflection Point And Executing Well On Buybacks Are Positives

I am impressed with TOUR’s bottom-line performance and shareholder capital return for the latest quarter.

Tuniu delivered positive GAAP net profit attributable to shareholders and non-GAAP net income attributable to shareholders of RMB13.9 million and RMB19.7 million, respectively for Q1 2024. In contrast, TOUR suffered from headline net losses and normalized net losses of -RMB7.0 million and -RMB5.4 million, respectively in the recent quarter. These numbers were obtained from the company’s first quarter results press release. In its results release, Tuniu mentioned that its non-GAAP earnings are adjusted for “share-based compensation expenses, amortization of acquired intangible assets, impairment of goodwill and impairment of property and equipment.”

TOUR achieved positive normalized or non-GAAP adjusted net income for four straight quarters running between Q2 2023 and Q1 2024. More significantly, Q1 2024 was the maiden quarter of positive GAAP or headline net profit for Tuniu. It would be fair to say that TOUR has reached an inflection point with respect to its profitability.

At its Q1 2024 results briefing, Tuniu indicated that it has placed a greater emphasis on “more profitable products, like our in-house packaged tour products” and utilized “automation systems” to “improve operational efficiency.” In other words, TOUR has managed to boost its profitability by optimizing its revenue mix and relying on technology to generate cost savings.

While TOUR didn’t provide bottom-line guidance, the company stressed at its most recent quarterly earnings call that it will “try our best to achieve continuous profitability.” Also, the current consensus financial forecasts sourced from S&P Capital IQ point to Tuniu registering positive headline and normalized earnings of RMB9.4 million and RMB11.3 million, respectively for full-year FY 2024.

Separately, Tuniu’s improved bottom-line performance has given the company confidence to return excess capital via share repurchases. The company doesn’t pay a dividend.

In mid-March, TOUR initiated a new $10 million buyback plan, which doesn’t have an expiry date. In the two and a half months between mid-March and end-May, Tuniu spent $2.9 million on share buybacks.

Assuming that Tuniu continues to buy back its own shares at a similar pace or more than $2.5 million every quarter, TOUR will likely be able to complete its existing share repurchase program within a year. This implies that the stock’s potential forward one-year share buyback yield is an enticing 7.6% based on my calculations.

To sum things up, TOUR recorded positive GAAP earnings for the first time in the company’s history, and it made a good start with the execution of its buyback program.

But Guidance Points To A Slow Pace Of Revenue Growth In Q2

On the flip side, Tuniu’s Q2 2024 top-line growth outlook is less favorable than its actual first quarter revenue expansion.

Revenue for TOUR jumped by +71% YoY to RMB108.0 million in the first quarter of this year. But the company anticipates that its top line will expand by a relatively more modest +17% YoY to RMB117.4 million, as per the mid-point of its guidance.

I am concerned about Tuniu’s actual Q2 2024 and full-year 2024 top-line performance, taking into consideration a number of factors.

The first factor is that a high base could affect TOUR’s top-line performance for the subsequent quarters of the year. The company’s revenue in RMB or local currency terms increased by +52% YoY in Q1 2023. But Tuniu’s revenue surged by +171%, +129%, and +266%, in Q2 2023, Q3 2023, and Q4 2023, respectively on a YoY basis.

The second factor is that Tuniu’s non-core or non-packaged tours travel-related business has been growing at a slower pace than its core packaged tours business. In Q1 2024, TOUR’s revenue derived from packaged tours and other travel services expanded by +107% YoY and +9% YoY, respectively.

Looking ahead, Tuniu guided at its first quarter earnings call that “revenues from our core business, packaged tours, will have a higher growth rate than total revenue” in Q2 2024. This in turn suggests that its other and non-core travel-related business might continue to perform modestly for the second quarter of the year and beyond.

In its 20-F filing, TOUR highlighted that its non-core travel offerings include “sales of tourist attraction tickets, visa application services, hotel booking services, air ticketing services, train ticketing services, car rental services and insurance services.” Although more recent data isn’t available, Tuniu was the leader in the Mainland Chinese packaged tour market boasting a “20% market share” a decade ago. It is reasonable to think that TOUR will find it harder to compete in other non-core travel segments, which explains why its other travel-related offerings revenue is growing much slower than its core packaged tours business.

The third factor is that an increasing number of Chinese travelers might opt to travel on their own rather than sign up for packaged tours to save costs, which will be negative for Tuniu. A May 6, 2024, Reuters article indicated that travel spending on a per-capita basis during China’s Labor Day holiday in the first week of May this year was 11.5% below pre-pandemic levels. This suggests that Chinese travelers’ travel budgets might have shrunk, which might translate into lower demand for packaged tours.

Closing Thoughts

A Hold rating for TOUR is warranted in my opinion, after considering its profitability improvement, shareholder capital return, and revenue growth outlook. Tuniu’s valuations are also roughly at the same level as its peers and this provides support for a Hold rating as well. The market currently values TOUR at 13.9 times (source: S&P Capital IQ) consensus forward FY 2024 P/E. In comparison, its peers Tongcheng Travel (OTCPK:TNGCF) [780:HK] and Tripadvisor (TRIP) are now trading at consensus forward P/E ratios of 13.4 times and 13.5 times, respectively as per S&P Capital IQ data.

Read the full article here