")

Couple spills popcorn when they see the 14% yield on preferred shares.

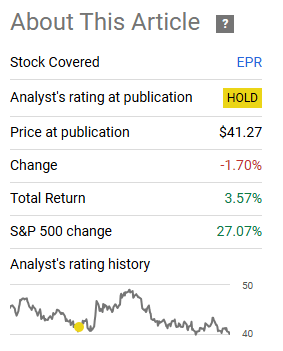

In our previous coverage of EPR Properties (NYSE:EPR) we looked at the valuations and risk of this triple-net REIT. While there was much to like and the valuations were relatively compelling, we went with a Hold rating and stayed out of buying this. That worked out well as it could in this market where absolutely nothing goes down except the morale of remaining bears. EPR managed to track the risk-free total returns over this timeframe and did not make us regret staying out.

Seeking Alpha

We look at how things are evolving for this REIT and tell you why we did step off the sidelines for this one and made it one of our larger positions.

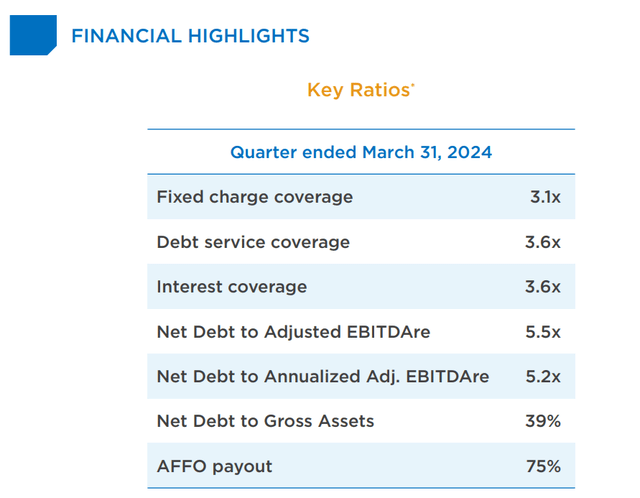

Q1-2024

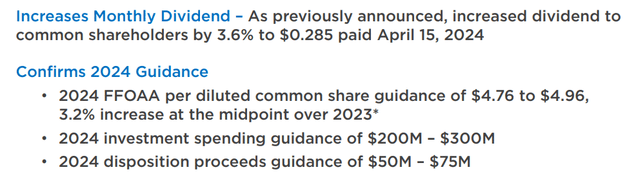

Things were steady in the first quarter of 2024. EPR guided for its funds from operations guidance to come in at $4.86 (midpoint) a share. A 3.6% increase over 2023 is a fine result for a REIT trading this cheap. The net acquisition guidance was not too shabby either and suggested that the REIT is finding opportunities even within its higher cost of capital setting.

EPR Q1-2024 Presentation

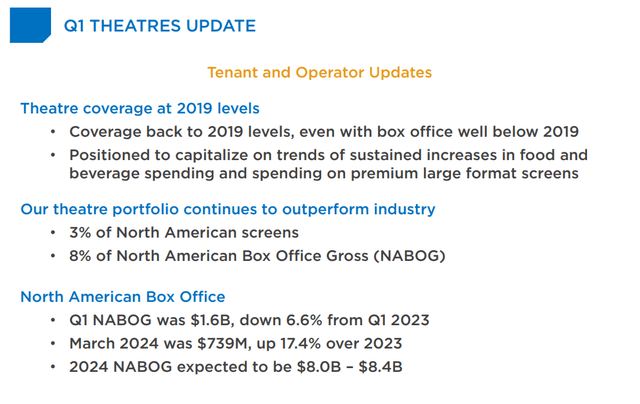

The key question every quarter is always about theaters and that is why this slide is found fairly early on in their lengthy presentation. Rent coverage has been improving for EPR’s theaters, though at the moment, that is not enough to assuage concerns about a potential downturn in this sector.

EPR Q1-2024 Presentation

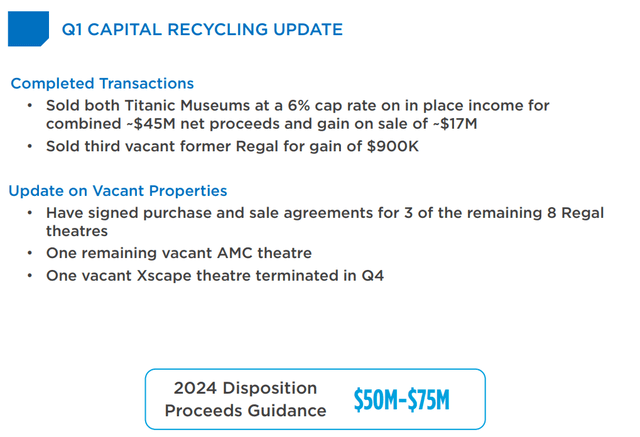

EPR’s dispositions are also theater focused as it tries to improve the quality of its portfolio.

EPR Q1-2024 Presentation

Outlook

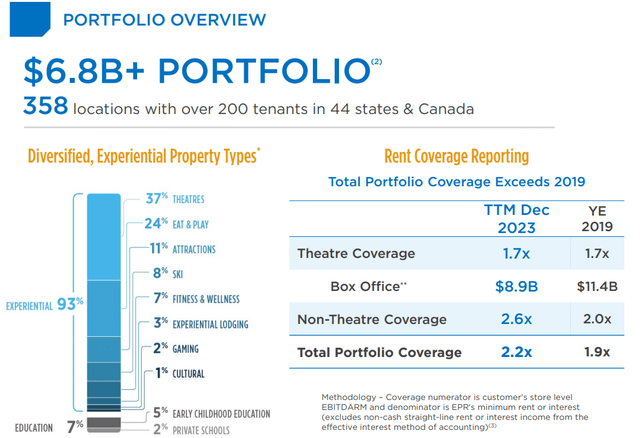

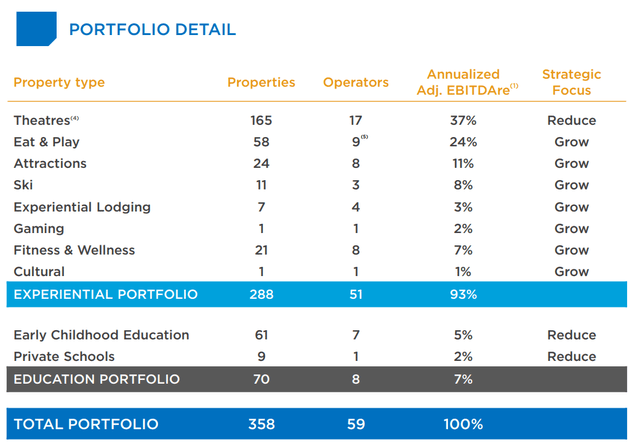

With an 8.4% yield, and a 70% payout ratio, you would think this REIT would have a legion of fans. Well it does, but that is not helping the multiple. It still trades at 8.5X FFO. The reason is, of course, that theaters form a third of its $6.8 billion portfolio. The other reason is that the rest of its portfolio is also more economically sensitive, relative to grocery or pharmacy, focused triple-nets. That said, rent coverage looks fairly solid at this point.

EPR Q1-2024 Presentation

EPR is slowly increasing the non-theater entertainment portion of its portfolio, but it is a slow process. With the current cost of capital, it will take many years.

EPR Q1-2024 Presentation

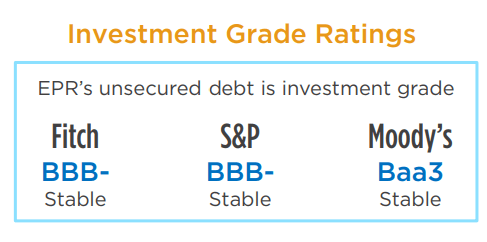

But the rational investor should not have any fear of a problem here for a few reasons. The first being that the credit agencies have sliced and diced this from every angle. EPR’s turbulence during the pandemic was the highest amongst triple net REITs, and they have dissected the current situation quite well. EPR still maintains investment grade ratings.

EPR Q1-2024 Presentation

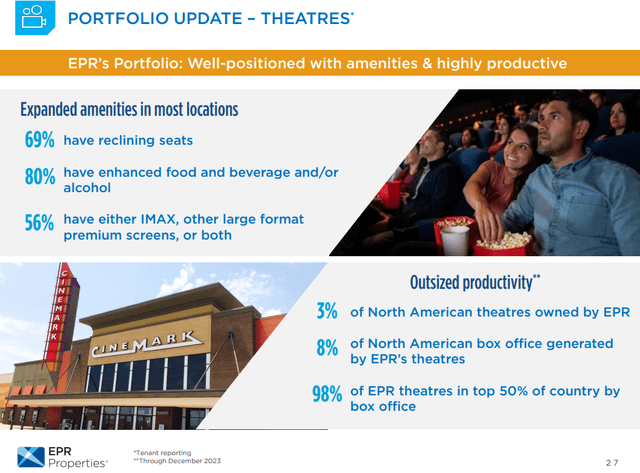

One of the key reasons is that EPR has the best theaters and any whittling down of screens is not going to be in their portfolio. You can see that in the slide below.

EPR Q1-2024 Presentation

You can also see that from Fitch’s commentary on the situation.

Headroom to Withstand Cinema Turmoil: Despite uncertainty around the industry, Fitch believes EPR has capably managed its exposure. As Regal’s largest landlord and owner of a substantial portion of its best performing theatres, EPR was able to negotiate a favorable master lease with Regal which went into effect as it emerged from bankruptcy.

Given these favorable negotiations as well as EPR’s proactive negotiation with AMC resulting in a master lease modification during the pandemic, Fitch believes that the company is well positioned going forward despite the larger industry picture. Additionally, the company’s meaningful headroom under its leverage sensitivities provides a buffer in the event of any unforeseen operating shocks.

Source: Fitch

The other mitigating factor is that EPR’s interest coverage ratios remain fairly high for this stage of the cycle.

EPR Q1-2024 Presentation

While the bankruptcy of AMC Entertainment Holdings, Inc. (AMC) is certain in our view, the impact to EPR’s rents is likely to be fairly modest in a worst-case scenario. We don’t see it as enough to even require a dividend cut.

How We Played It

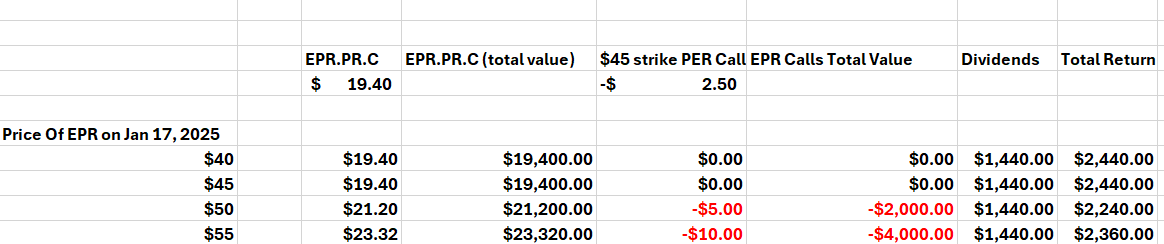

While EPR has a lot of the characteristics of a good investment, we did not still take a position in the common shares. We did, however, create a unique long position in the preferred shares on February 8, 2024. At that time, EPR was trading at $42.75 and EPR Properties PFD C CV 5.75% (NYSE:EPR.PR.C) was at $19.39. We are showing the prices below that were visible for the EPR options.

IBKR Feb 8 2024

The trade we did was as follows.

1) We added 1,000 shares of EPR.PR.C at a price of $19.40.

2) We sold 4 Calls on EPR (the common shares) for the January 2025 $45 strikes at $2.50 each ($250 per contract, $1,000 total).

EPR.PR.C’s are convertible into 0.424 common shares of EPR. So at the price limit of $19.40 we had an embedded option on EPR at around $45.75.

Since we got $2.50 for each of these calls, our effective sale price for EPR is $45+2.50=$47.50. So while the calls appear naked, they were indirectly covered via the convertibility of EPR.PR.C. We sold 4 calls for 1000 EPR.PR.C as every 236 shares of EPR.PR.C essentially covers 100 shares of EPR. We really needed just 944 shares to do this trade, but we think EPR.PR.C is modestly attractive even without the calls, so we went with the round number of 1,000 shares. Below is the return profile at different prices of EPR on January, 17, 2025. We have assumed in case EPR goes lower, EPR.PR.C should be fairly valued exactly like (EPR.PR.G) which is a non-convertible preferred trading at almost the exact same price.

Author’s Calculations

In essence, we are aiming to make about a 14.2% annualized yield on preferred shares. This fits with how we trade these things opportunistically without getting married to a long-term holding. So far, this has worked out better than expected. EPR price is about 4% lower and the calls have decayed by 70% (last trade 75 cents). We will update this trade in about 7 months and tell you how it went.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Read the full article here