")

Athabasca Oil (OTCPK:ATHOF) has long had a presence in thermal oil production. That production may well benefit from the operations of the Mountain Valley Pipeline because the pipeline could decrease the discount from light oil, at least temporarily and hopefully longer. However, many heavy oil and thermal producers survive long-term by having light oil production or even condensate production because that discount has a tendency to expand during times of weak commodity prices, which wipes out the thermal cash flow. The light oil production provides badly needed cash flow during such times. Athabasca now has a partnership with Cenovus Energy (CVE, CVE:CA) that may well fit their long-term needs for lighter oil production. This would decrease the earnings and cash flow volatility when compared to many competitors in the industry.

The last article noted that the company reached a net cash position. What was unexpected since then is that the company has stopped repaying debt while returning 100% of defined free cash flow to shareholders in the form of stock repurchases. This raises the risk of this company somewhat because thermal oil is a discounted product compared to light oil. Sometimes that discount expands during cyclical downturns to necessitate a shut-in of production to stop negative cash flow. But then this company would have no cash flow until prices recover.

Obviously, the large cash position would help the company get through such a period. But repayment of the debt would make things a little less risky during a cyclical downturn.

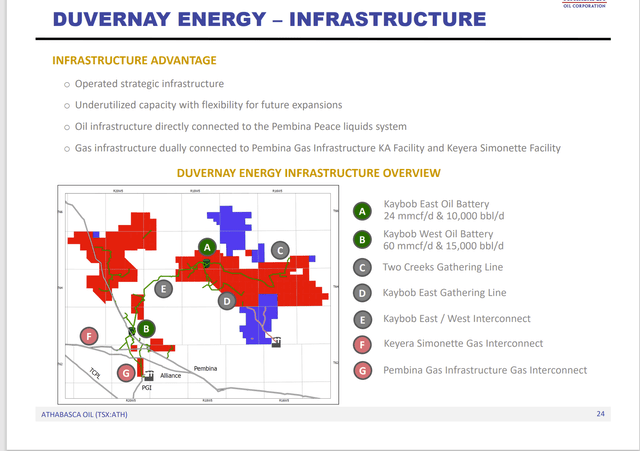

Cenovus Joint Venture

The joint venture has a lot going for it. At least some of the advantage is due to infrastructure. This joint venture would also provide needed cash flow during a cyclical downturn as light oil and other products would likely have a positive cash flow.

Athabasca Oil Summary Of Joint Venture Advantages (Athabasca Oil Corporate Presentation June 2024)

Having midstream capabilities already built reduces the time and money needed to get initial cash flow from the production of the first few wells. Therefore, this joint venture will be producing cash flow from the start without the need for intensive capital at the very beginning.

The area itself is the beneficiary of technology advances that have brought new life to acreage that has been producing for a long time. This is one of the reasons that the midstream structure is already in place in relation to the acreage.

Obviously, management is early enough to this particular opportunity to take advantage of the fact that the midstream structure in place has excess capacity. Some later arrivals may well have to wait for an expansion program to complete.

This opportunity has the ability to potentially provide that needed cash flow from a desired (light oil or even condensate) product that would help the company get through cyclical downturns.

The only warning sign is another slide that demonstrates that the partnership with Murphy Oil (MUR) did not work out. Murphy had been active in this area for some years. But that partnership sold some acreage and really has not been active (by drilling) in the area for about 2 1/2 years.

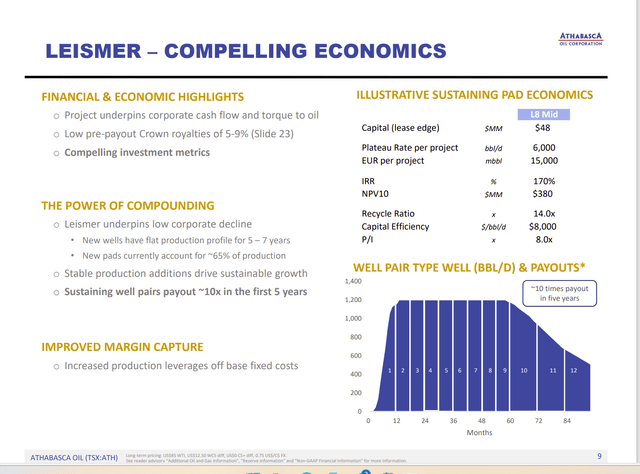

Thermal Oil

The company is planning to expand the thermal oil production. There is some risk to this, as the cash flow probably should be directed towards repaying debt. Thermal oil (and heavy oil) is often very profitable when commodity prices are in the range they are in right now.

However, downturns tend to expand the discount from light oil and eliminate the cash flow. This often necessitates shutting in production to prevent negative cash flow from production.

Having debt to service during a cyclical industry downturn can be a very financially stressful situation for a company like this.

(Note: This is a Canadian company that reports using Canadian Dollars unless otherwise stated.)

Athabasca Oil Leismer Thermal Oil Growth Guidance (Athabasca Oil Corporate Presentation June 2024)

Despite the warning, the economics in the current commodity price environment for expanding production are often compelling for the reasons shown above. To some extent, management can do some hedging to protect the cash flow during a cyclical downturn. Oftentimes though, that hedging is based upon the light oil price. So, the expansion of the discount from light oil can reduce the effectiveness of a hedging program.

Management has some other thermal oil projects underway as well. This one is the largest and most significant production for the company at the current time.

The biggest item to note is that costs are coming down over time. This is extremely important for a discounted product like thermal oil.

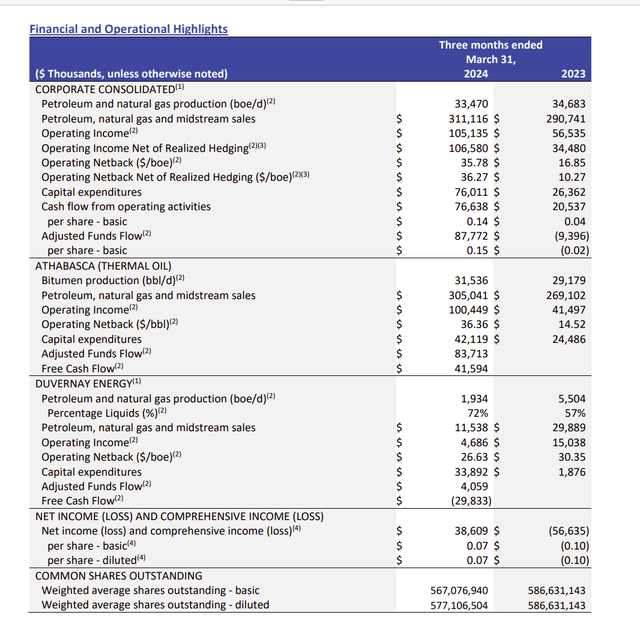

First Quarter Results Summary

The cash flow is tremendous for the first quarter. But the previous first quarter demonstrates what can happen to cash flow. Because cash flow is so volatile with thermal oil, the cash flow in the good quarters is not valued as much as cash flow from light oil producers.

Mr. Market has from time to time gotten carried away with optimism on these type producers. But the stocks have inevitably crashed during downturns when cash flow worries predominate.

(Note: This is a Canadian company that reports using Canadian Dollars unless otherwise stated.)

Athabasca Oil Summary Of First Quarter ResultsAthabasca Oil Summary Of First Quarter Results (Athabasca Oil First Quarter 2024, Earnings Press Release)

The company does have a net cash position. But management insists on keeping a large amount of cash for contingencies, and therefore maintains a fair amount of debt as well.

The aggressive stance comes from returning all free cash flow to shareholders through share repurchases. It would probably increase the safety of the investment to use at least some of that free cash flow to reduce debt.

This management has been known to buy and sell subsidiaries for the right price. Therefore, a large cash balance, as is currently the case, could signify that management will go shopping when conditions are right.

Still, the current balance sheet strategy is not for conservative investors.

Summary

The company has a net cash position of very roughly C$90 million. That is definitely an improvement over at least some of the past years. However, this management would probably be well served to reduce the debt and increase the net cash position more.

This is a management that has successfully bought and sold assets. So, there is likely to be more of that in the future. This sometimes affects the valuation of the stock price because the market is aware that there will be a startup period in the future after the next deal.

The company is likely a hold at this point because the stock price is as likely to go up from the current value as it is down. The management purchases of stock does help to support the stock price. But it does not eliminate the risk of no cash flow during a cyclical industry downturn.

The large cash balance does help the company get through downturns. But that is also the time when management often buys something.

The risk is elevated not only because the company is small, but also because management keeps a fair amount of debt while producing a discounted product. Therefore, this stock is only for those investors capable of dealing with that elevated risk.

Cash flow for thermal producers is far more volatile than it is for light oil producers. Therefore, the good times tend to not be as highly valued because the cyclical downturns carry worse consequences for this group.

Risks

Any upstream producer is exposed to the volatility and low future visibility of commodity prices. Thermal producers carry the additional risk that the discount from light oil can widen at any time to adversely affect cash flow. The Mountain Valley Pipeline could lead to a reduction in that discount because it increases the ability of Canada to export its heavy and thermal oil. Whether that reduction lasts a few years or is permanent remains to be seen.

The partnership with Murphy Oil was not as productive has hoped. That serves as a warning that the partnership with Cenovus Energy may fail to meet investor expectations as well.

The loss of key personnel (especially in a smaller producer) could set back the company plans or even prove fatal to the company.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here