")

BYD Company Limited (OTCPK:BYDDF) achieved something truly remarkable in the fourth quarter of FY 2023: the Chinese electric vehicle (“EV”) company managed to overtake Tesla, Inc. (TSLA) as the world’s leader in terms of electric vehicle sales. I suspected in my previous Seeking Alpha article, “BYD: Set To Overtake Tesla,” that this was a distinct short-term possibility given the trajectory of BYD sales. As a result, BYD is entering 2024 with solid momentum, which I believe could ultimately be reflected in a much higher market cap and share price.

Because BYD executed extremely well in FY 2023 and successfully challenged Tesla as the world’s preeminent EV company, I believe the valuation discrepancy between those two firms, even after application of a “China discount” for BYD, cannot really be justified anymore.

Since BYD also has a favorable gross profit development and is already profitable, I see BYD as possibly the lowest-risk, large-cap electric vehicle company that investors can invest in at the moment. The risk profile remains one of the most attractive that I have seen in the EV market, in the U.S. as well as abroad!

Previous rating

In my last work on BYD, I indicated that a good reason to buy BYD was the possibility for the Chinese electric vehicle company to actually overtake Tesla in terms of total sales and deliveries. Another reason to buy BYD was that the electric vehicle company was already profitable. With the EV company now achieving this feat and with its margins leading the industry as well as strong export momentum, I believe BYD now represents the best value in the large-cap EV category.

BYD just overtook Tesla as the world’s largest EV company

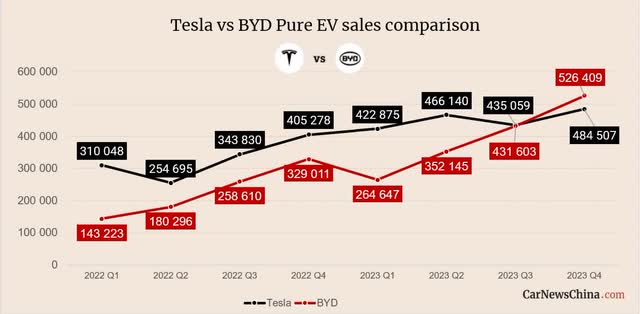

According to the most recent delivery reports made available by China’s electric vehicle companies earlier this month, a new king of the EV market has been crowned: BYD has officially taken over Tesla as the leading electric vehicle company in the world with record deliveries in the fourth quarter.

In the third quarter, BYD came within striking distance to Tesla and only sold 4 thousand fewer EVs than the American EV giant. Now, BYD reported that it sold 526,409 fully electric vehicles in the fourth-quarter, showing a stunning year-over-year growth rate of 60%. BYD does not only sell battery-powered electric vehicles (“BEVs”), however, but also plug-in hybrid electric vehicles which have both a gas-powered internal combustion engine (“ICE”) alongside a battery pack. BYD sold a total of 3.02M vehicles in FY 2023, including 1.4M plug-in hybrids.

Tesla, by comparison, sold 484,507 electric vehicles, which was about 42,000 EVs less than BYD. Tesla’s year-over-year growth rate in Q4 ’23 sales was only 20%, and BYD grew three times faster than Tesla. BYD’s growth becomes even more impressive considering that BYD is not a small startup: the company’s factories churn out an average of 130 thousand electric vehicles per-month.

CarNewsChina

What makes BYD compelling in FY 2024 is not only the absolute size of its sales in relation to those of Tesla, but also that the EV company has a strong product lineup, possibly the strongest it ever has had. Three out of the five best-selling electric vehicles in China in the third quarter rolled off of BYD’s factory belts. These included the BYD Yuan, the BYD Dolphin, and the BYD Seagull.

Related to BYD’s persistently ranking at the top of most popular EV lists in China, the company also is becoming a formidable EV player in markets outside of China as well. According to the company’s January 2024 update, export markets received 242,765 electric vehicles, showing a 334% Y/Y growth rate. The EV maker’s products are now available in 70 countries, and I expect export markets to drive BYD’s growth going forward. One such attractive market opportunity could be Indonesia, which has a population of 279M. Indonesia’s EV adoption rate is in the single digits, but the government is making an effort to develop a domestic EV infrastructure, which makes the country obviously attractive for BYD. The EV maker is set to enter the market in January, which could further spur BYD’s export growth numbers in the quarters ahead.

Counterpoint Research

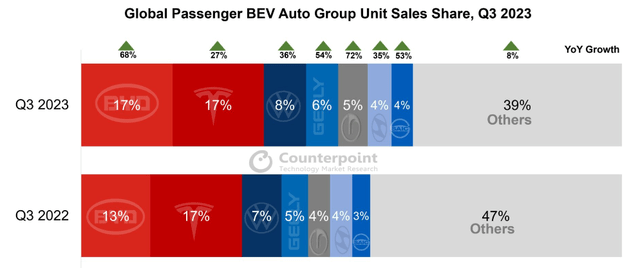

In the third quarter, BYD achieved a comparable unit sales share, on a global level, as Tesla. With the most recent numbers for the fourth-quarter now being reported, it is likely that BYD has seen a market share increase in the fourth quarter as well, which could further boost the company’s performance in FY 2024.

Counterpoint Research

While BYD is not a startup like NIO (NIO), Li Auto (LI), or XPeng (XPEV), which I have focused on more in the past, BYD is seeing a strong margin trend. In my work on Li Auto, in which I compared the company against the two other startups, NIO and XPeng, I said that Li Auto offered the best value in the startup EV segment due to its comparable high margins: “Decoupling From The EV Competition.”

One even better bet than Li Auto on the Chinese EV market, however, may be BYD… which I have not included in previous comparisons due to the company’s large size and because of differences in profitability profiles.

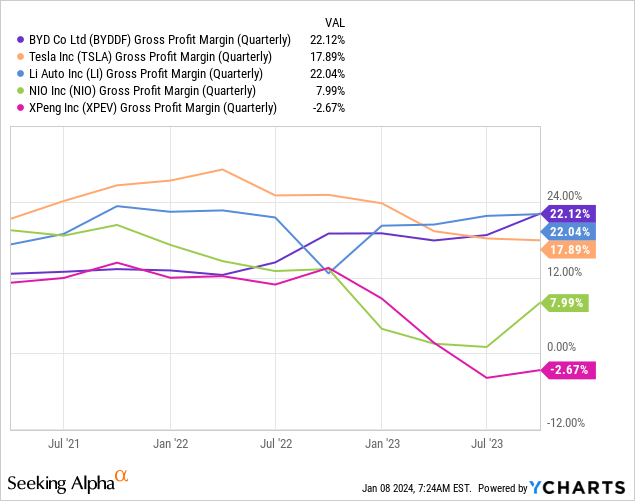

BYD achieved a 22.1% gross profit margin in Q3 ’23, and is seeing growing margins. It is the most profitable EV producer in the market. It beat out Li Auto as well as Tesla, the latter of which had a gross profit margin of 17.9%. Since BYD is also profitable on a net income basis, BYD may be the best bet in the large-cap EV market in FY 2024, especially if BYD manages to decouple from Tesla.

BYD’s Valuation And Estimate Revision Potential In FY 2024

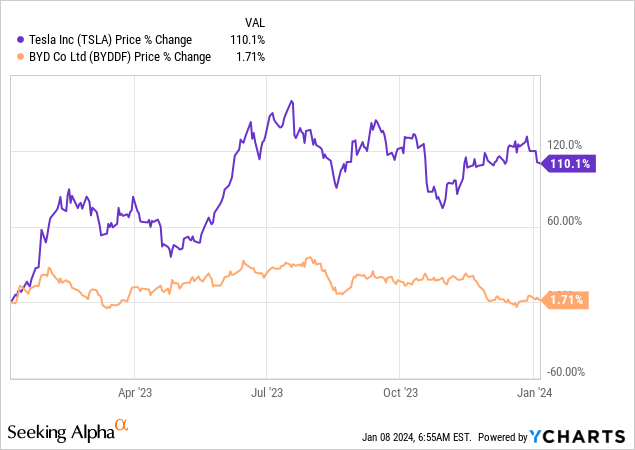

With BYD now being the largest EV company in the world based on Q4 sales, I find it striking how cheap the electric vehicle maker’s shares still are. Shares of BYD trade at 11.4X earnings compared to a P/E ratio of 44.4X for Tesla… and this despite BYD growing 3 times faster than Tesla in Q4 ’23. BYD, therefore, has considerable EPS upside revision potential, in my opinion, given its enormous momentum in sales growth in both China and abroad.

Since BYD is now selling more vehicles than Tesla, I believe there is no justifiable reason for this massive valuation discrepancy. If BYD continues to execute well in FY 2024, I can definitely see the valuation gap between BYD and Tesla narrow significantly. With BYD set to grow its EPS by more than 40% next year, I believe shares of BYD could be valued at a 20X P/E ratio very easily (still less than half of Tesla’s P/E), implying a fair value close to $47.

Seeking Alpha

China-Specific Risks

A big risk with BYD is that the company submits unaudited financial statements, which is not an entirely bad reason for investors to dismiss BYD as a potential investment completely. Additionally, BYD is a China-based EV maker, and the 2020 crackdown of the CCP on Chinese technology companies made clear that companies in China face higher regulatory risks than U.S. companies. A potential invasion of Taiwan may also be a risk factor that investors must consider. Despite the risks, which I believe are more political in nature than technological, I believe that BYD’s surging EV sales as well as the fact that the company is already profitable make an investment potentially attractive.

Final thoughts

The electric vehicle industry just crowned a new leader, as China-based BYD officially overtook Tesla as the leading EV company in the world based on global Q4’23 sales. What I believe makes the accomplishment even more worthy of respect is that BYD has grown its sales by a massive 60% Y/Y compared to the year-earlier period, which is a reflection of growing EV adoption in China as well as product strength: BYD’s EV products consistently rank at the top of China’s top-selling EVs.

What I like most about BYD, however, is that shares trade at a large discount to Tesla shares, which I don’t believe is really that warranted given its strong fourth quarter sales results. BYD is also posting stronger gross profit margins than all of its rivals, including Tesla, a trend I expect to continue in FY 2024!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here