Introduction

Those of you who follow me know I’m a big fan of Business Development Companies. They are great for income investors like me who plan to supplement their dividend income in retirement. BDCs are some of the best vehicles for income. But many investors choose to stay away from these as they are often considered risky. And while I understand that theory to a degree, I don’t view them as being riskier than investing into well-known companies like Walmart (WMT) or Tesla (TSLA).

Reason being is it’s important to do your due diligence before investing into any company. BDCs typically loan to smaller, unknown companies that are sometimes distressed, which does make them riskier in the eyes of many. But like any stock, solid management is key and there are several BDCs with great ones. Dividend track records and how well they’ve navigated economic downturns are also important factors. I’ve recently covered three of the five listed below in the last month but was asked by a reader if I could compile a list of some BDCs using the metrics below.

There are several high-quality BDCs and in this article I rank 5 from best to worst. I discuss some metrics including dividend consistency, first-lien focus, balance sheet, and risks they face such as non-accrual loans. I also mention their portfolio diversification, track records, and management. All of these metrics play an important role when it comes to navigating economic downturns.

#1 ARCC

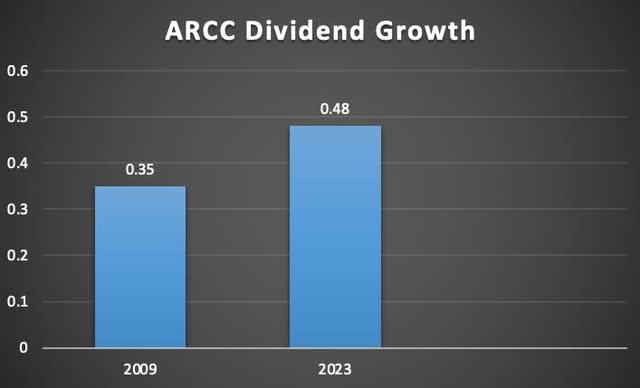

The first BDC on the list is Ares Capital (ARCC), the largest BDC by market cap. When it comes to surviving an economic downturn, I think ARCC deserves the top spot. Now some may say: ARCC cut its dividend during the Great Financial Crisis, so how can they make the top spot?

That is true. The company IPO’d in 2004 but in 2009 was forced to cut their dividend by nearly 17% from $0.42 to $0.35. Before then, ARCC had a pretty short record of raising the dividend. They raised the dividend from $0.30 to $0.42 for 5 years before being forced to cut. Since then, they have not cut the dividend and raised it from $0.35 to the current $0.48. Additionally, they have paid out specials and supplementals along the way, giving them an uninterrupted dividend streak of 14 years. In 2020 during the pandemic, the BDC showed their resilience by holding the dividend steady at $0.40.

Author

Some may disagree but the reason I list ARCC as #1 is that they are more financially conservative. BDCs have been thriving in the current macro environment and many investors who have held these investments have been rewarded handsomely over the last year. In 2022, ARCC paid out a supplemental dividend of $0.03 while raising the regular dividend 14.3% from $0.42 to $0.48. This year management has elected to keep the dividend steady at $0.48 while other BDCs have elected to raise theirs along with paying specials & supplementals.

Instead, I like the fact that management prefers to roll-over spillover income. Coming into 2023, the BDC had $643 million in extra income from 2022 and I expect 2024 to be a similar amount or more. It seems as though ARCC has elected to keep the dividend steady to prepare for a recession or an economic downturn. During the last FED meeting, starting around the 13:00 minute mark, the FED chair stated that a recession was all but dead due to the recent activity they’ve seen. My rebuttal to that is do you really think they would know that we are in a recession? Or would that be after the fact, similar to what happened when they kept saying inflation was transitory?

Portfolio Quality & Diversification

Another reason they earn the top spot is they have more experience during economic downturns. Although they were forced to cut the dividend during the ’07 to ’09 recession, one thing they gained from that was experience. It’s one reason why I think they prefer to be a bit more conservative. I’d rather have management retain more cash flow than pay out all their extra income from their predominantly floating rate portfolios. Because if the economy falls into a recession, they may be forced to cut the dividend if they had offloaded their extra income to shareholders.

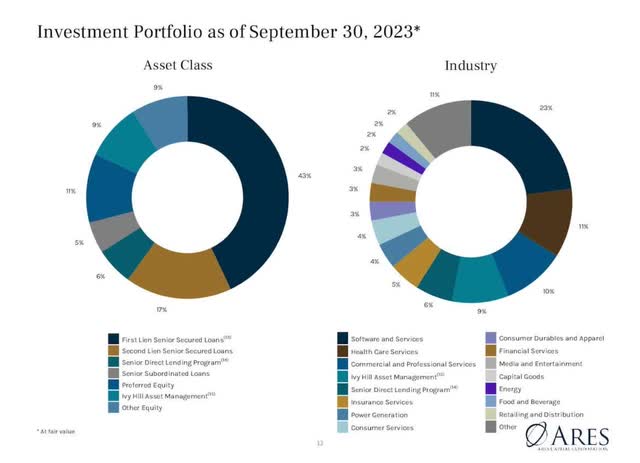

Most know that ARCC is externally-managed so the BDC is obligated to pay management fees that internally managed BDCs do not. At the end of last quarter, their portfolio consisting of 490 companies across 25 industries’ value stood at $21.9 billion. One thing investors may have a gripe about ARCC is their lower level of investments in first-lien loans. Out of all the BDCs in this article, they have the lowest percentage at 43.1%. Some could argue that because of this, they are less defensively positioned for possible downturns. Second-lien investments account for 17.2%. ARCC’s portfolio diversification and longer track record provide a buffer for their low first-lien focus.

ARCC investor presentation

Software & Services make up 23% of the portfolio while Health Care Services and Commercial & Professional Services make up 11% and 10% respectively. As you can see, ARCC’s portfolio is well-diversified. Another metric to look at when looking into BDCs, which pose a risk in a high interest rate environment, is their non-accrual percentages. In Q3, the company managed to decrease this from 2.3% in Q2 to just 1.2%. They also decreased leverage from 1.07x to 1.03x quarter-over-quarter.

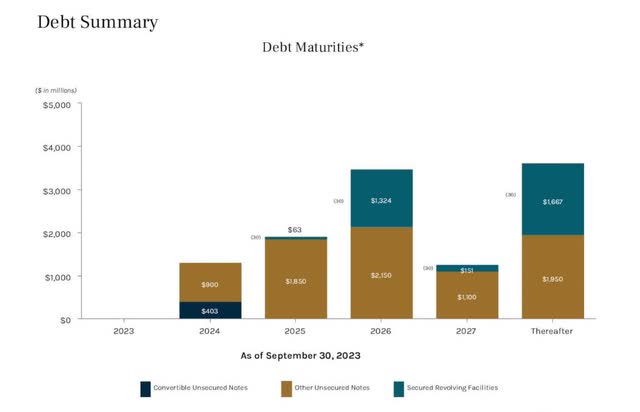

Something else that has investors worried are companies’ debt loads. At the end of the quarter ARCC had $311.8 million in cash and total liquidity of $5.3 billion. Furthermore, they had $1.3 billion in debt due next year. $400 million due in March and $900 million due in June. This debt had average interest rates of 4.625% and 4.2% respectively. So, the company will most likely have to refinance at a higher rate. But they have been working on decreasing their overall debt. This decreased from $12.2 billion to $11.5 billion year-over-year.

ARCC investor presentation

Although the company has a decent amount of debt due next year and will likely have to refinance this at a higher rate, the company’s overall balance sheet health is in great condition. Additionally, ARCC is investment grade rated and considered a blue-chip BDC with one of the longest track records in the sector. Because of this and their fiscally responsible nature, I rank them #1 when it comes to surviving an economic downturn. Their portfolio is also larger than 3 of the next 4 BDCs listed combined and they have a higher IG rating from Fitch. Additionally, I naturally gravitate towards ARCC as they align more with my investment principles.

#2 MAIN

Main Street Capital (MAIN) has the second longest track record on this list, IPO’ing 3 years after ARCC in 2007. Some could argue MAIN deserves to be #1 seeing they went public during the recession and did not cut their dividend like ARCC. That’s a fair point. But like I previously mentioned, I prefer businesses that are more conservative but understand MAIN being numero uno on someone’s list. They’re also a favorite amongst dividend investors because of their monthly dividend. Since going public the BDC has never reduced its dividend and since switching to a monthly payer, has raised the dividend 92% from $0.1250 to $0.24. Recently they raised it by 2.1% at the beginning of the month.

Author

Another difference between ARCC and MAIN besides their payment schedule is Main Street Capital is internally-managed while ARCC is not. Lots of investors prefer internally-managed BDCs because they’re usually more aligned with shareholders. Which means investors are more likely to receive special and supplemental dividends. MAIN recently announced a supplemental cash dividend of $0.275 payable in December.

Traditionally, internally-managed BDCs sometimes pay an end of year special dividend but since the start of rate hikes, many have been extra generous to their shareholders. Since 2022, MAIN has paid out several specials along with raising the regular dividend nearly 12% from $0.2150 to its current of $0.24.

Portfolio Quality & Diversification

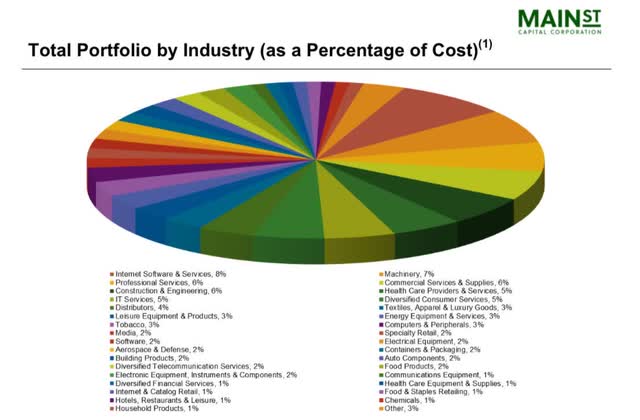

MAIN’s portfolio is much smaller with 195 companies compared to ARCC’s almost 500. They also have a much smaller market cap at $3.36 billion. But the latter is more diversified across 50 industries compared to 25 for ARCC. Similar to its peer, MAIN also has most of its portfolio invested in Internet Software & Services, although a smaller percentage of 8%. Professional services make up 6% while Construction & Engineering make up 6% as well. ARCC has a higher concentration because MAIN has double the amount when it comes to different industries.

MAIN investor presentation

They also have a higher concentration in first-lien loans with 99%. First-lien loan concentration is an important metric to look at when investing in BDCs. Especially if a downturn is expected. Reason being is because those that have a higher concentration in first-liens are likely to have less financial stress as they are the first ones to get paid when portfolio companies are distressed. In short they have head of the line privileges when it comes to the lenders that the company owes money. During the quarter the company reported non-accruals accounted for just 1% of their total investment portfolio.

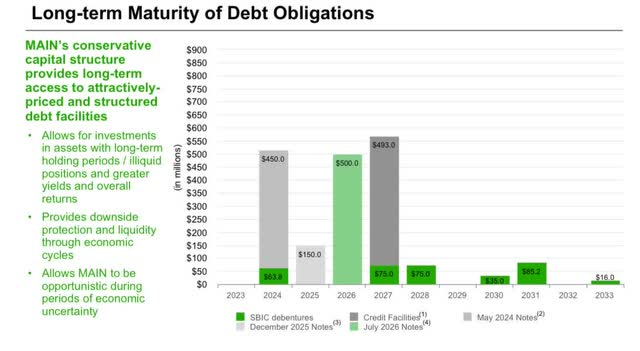

MAIN also has less total debt at just $1.9 billion compared to $11.5 for ARCC, and less maturing next year with just $450 million of notes due in May. This has an interest rate of 5.2%. Additionally, they also managed to decrease their overall debt from over $2 billion year-over-year. And like ARCC, they are also investment grade rated from both Fitch and the S&P.

MAIN investor presentation

When it comes to balance sheet health, MAIN is in a much better position than its largest peer. But a larger debt load is expected for a company that is much bigger.

#3 BXSL

Blackstone Secured Lending (BXSL) is a newcomer in the BDC space having IPO’d in 2018. They have quickly became a rising star in the sector and a favorite amongst dividend investors, and in this article you’ll clearly see why. But because of their short track record, I can’t justify putting them higher on the list. As you can see BXSL’s dividend growth in just three years is a reason why dividend investors love them.

Since IPO, the BDC has raised the dividend over 45% from $0.53 to the current dividend of $0.77. Since the start of rate hikes they paid out several special dividends in 2022 and raised the dividend by 10% earlier this year from $0.70. Like ARCC they are also externally managed by Blackstone (BX), the largest alternative asset manager with over $1 trillion in AUM. They also have a larger market cap than MAIN at 4.80 billion.

Author

Portfolio Quality & Diversification

Another difference in BXSL that I really like is they prefer to invest in larger companies compared to their peers. Most BDCs invest in companies with an EBITDA anywhere from $3 million to $20 million. BXSL prefers to invest in companies with an average EBITDA of $183 million. Reason being is because larger companies typically provide better risk-adjusted returns. Furthermore, companies with an EBITDA of $100+ million grew 7x the rate of those with an EBITDA of $50 million or less according to the BDC.

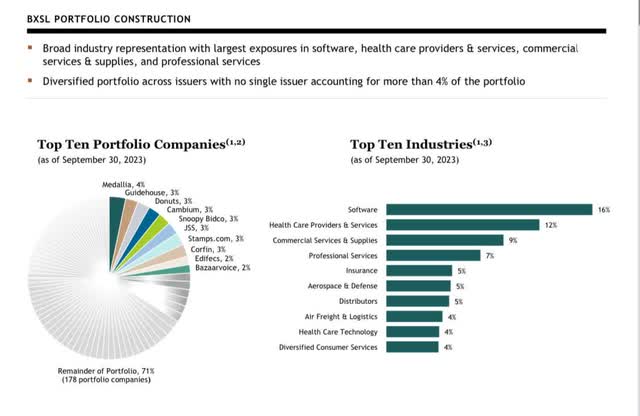

Another thing to like is their first-lien focus and diversification. At the end of the quarter they had 188 companies across 35 industries. Like ARCC they are invested in similar industries with Software & Services, HealthCare, and Commercial Services being the top 3. BXSL has a total portfolio value of $9.5 billion with 98.4% in first-lien, senior secured debt. Second-lien accounts for 0.4% of the portfolio.

BXSL investor presentation

The BDC also has a strong balance sheet with a total debt amount of $4.9 billion. BXSL had $1.5 billion in liquidity and undrawn debt at the end of the quarter. Unlike its peers ARCC & MAIN, BXSL has no debt maturities until May 2025 for $223 million. This has an interest rate of 2.525%. So in comparison, BXSL is in a better position balance sheet wise considering the macro environment. I suspect interest rates will be lower by then, but likely higher than 2.5%. Either way the amount is not substantial and the BDC has more than enough liquidity to cover it.

BXSL investor presentation

#4 CSWC

Coming in at number four is a long-time favorite of mine Capital Southwest (CSWC). They also happen to be one of my largest portfolio holdings along with ARCC. CSWC has been around for a while having been founded in 1961 and electing to be regulated as a BDC in 1988. They completed a spin-off of their industrial investments into a separate company in 2015. Since then the BDC has performed exceptionally well. They are also the smallest BDC on this list with a market cap of less than $1 billion.

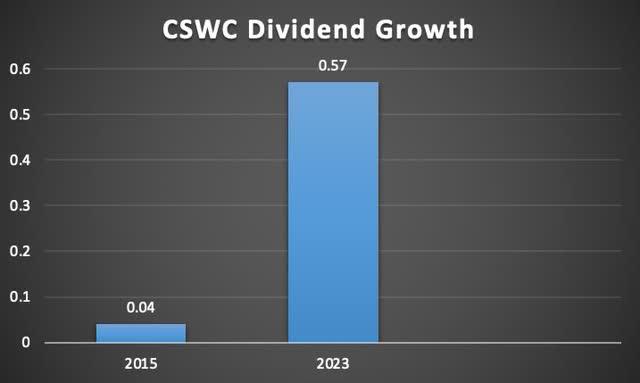

Since 2015, the BDC has raised the dividend over 1000% from $0.04 to the current $0.57 where they raised it by 1.8% from $0.56 last month. CSWC seems to be a bit more shareholder friendly than other BDCs. Excluding the current high interest rate environment, the BDC has paid out special dividends nearly every year to shareholders with the exception of 2016. One reason for this is CSWC is an internally-managed BDC similar to MAIN.

Author

Portfolio Quality & Diversification

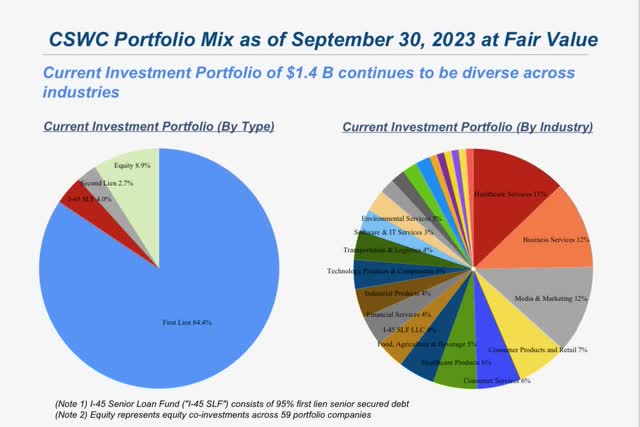

When it comes to rewarding shareholders, I think CSWC is probably number one. But just because they are shareholder friendly and investors love the extra income, that doesn’t mean they’re the better BDC. Out of all its peers, they also have the smaller portfolio at just $1.4 billion. This consists of 94 companies in total across 26 industries. Like ARCC and BXSL, they also have a good amount of their portfolio invested in HealthCare Services. However, they differ slightly as they have 12% invested in the Media & Marketing Industry compared to the other BDCs, who have a small percentage in this industry.

CSWC investor presentation

Another reason why they may be a favorite among dividend investors besides the friendly payouts are their first-lien focus. Similar to BXSL & MAIN, CSWC focuses on first-lien loans as well with 84.4% invested. This is a lower amount than the other two, but this nearly double ARCC’s. They also prefer to take a higher percentage in equity investments at 8.9% compared to the others. One thing of note is CSWC has the higher percentage of non-accrual loans at 2%, but this is still well-below the KBW BDC average of 3.8%

CSWC also has one of the best balance sheets in the sector which also makes them a favorite of mine. The BDC also received an investment grade rating of BBB- from Fitch earlier this year and has an IG rating from Moody’s of Baa3 as well. Furthermore, they have one of the lowest leverage ratios at just 0.92x compared to its peers. And no debt maturities until January & March of 2026! This has an interest rate of 4.5% and 2.41% respectively. So when it comes to well-laddered debt maturities, CSWC beats all of its peers.

CSWC investor presentation

#5 OBDC

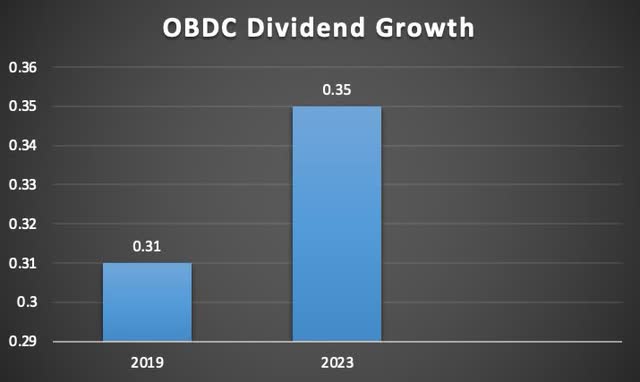

Last on the list we have another newcomer with Blue Owl Capital (OBDC). Similarly to ARCC and BXSL, they are also externally-managed. I put them last on the list because they have their shortest track record of all those listed having formed just four years ago.

They also have the least impressive dividend growth amongst their peers as well with a near 13% increase in the regular dividend in a four year period. They recently reported Q3 earnings and increased the regular dividend by $0.02 and declared a supplemental of $0.08. BXSL having went public one year prior triples OBDC’s dividend growth when you compare the two. OBDC has however paid out special dividends every year since going public with the exception of 2021.

Author

Portfolio Quality & Diversification

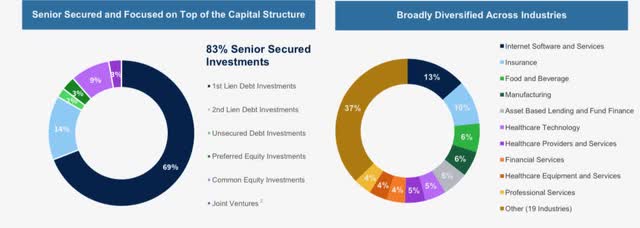

At the end of Q3, OBDC’s total portfolio value stood at $12.9 billion. They also had 187 companies across 30 industries. This consisted of 69% invested in first-lien loans and second-lien at 14%. They also have a market cap of 5.4 billion, making them the second largest BDC on the list, only behind ARCC. One thing I like about OBDC is that similarly to Blackstone Secured Lending, they also place an emphasis on larger companies. These have an weighted average EBITDA of $196 million. With the exception of CSWC, they also have most of their portfolio invested in the Software & Services industry at 13%. Additionally, they have less in HealthCare Services and more concentration in Insurance and the Food & Beverage sectors at 10% and 6% respectively.

OBDC investor presentation

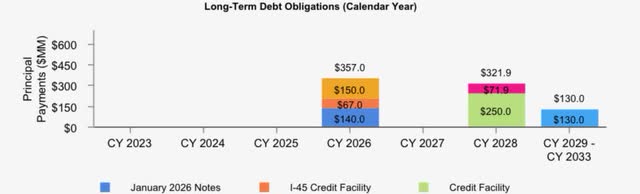

Although they’re the newest BDC on the list, I was impressed by the company’s balance sheet. They only have $400 million due in April of next year. This has an interest rate of 5.25%. It is possible that the BDC may have to refinance at a higher rate, especially with the FED leaving the door open for more rate hikes. But the company’s debt is very manageable and they also had $1.8 billion in liquidity in cash and undrawn debt. Another thing of note is OBDC did see a rise in non-accrual loans this year, similar to its peers. In Q2 this was 0.9%, a rise from 0.3% in Q1.

Risk Factors

BDCs have enjoyed the current macro environment over the last year and so have shareholders. But despite the extra income due to their predominantly floating rate portfolios, high interest rates continue to be a headwind for their portfolio companies. Most have seen a rise in non-accruals although they are all well-below the KBW BDC average. With inflation still lingering, BDCs still face a rise in these in the coming quarters.

I do think we are closer to the end of the rate hike cycle but it is still worth a mention. I still suspect the first rate cut to come sometime next year so investing in higher-quality BDCs such as those listed in this article is important. Also due to higher interest rates, all of the BDCs listed are now trading at premiums well-above their NAV prices, with the exception of OBDC.

At the time of writing they still trade at a 9% discount to its NAV of $15.40 at $14.12. One reason for this could also be that the BDC is newer and could take a few more years to jump on investors radar. For those looking to add or start positions in those listed, I would wait for any share price weakness to get a margin of safety. Specifically, I like ARCC and CSWC in the $16-$18 range, which both traded near here in the 1st quarter of the year. I prefer BXSL in the $25 range and MAIN near the $35 level. The BDC typically trades at/or around $40 due to the monthly dividend. Investors may not get any good entry levels until rates are cut, or an unexpected downturn occurs.

Investor Takeaway

As I mentioned previously, BDCs have enjoyed the current macro environment due to their business models. This has caused many of their prices up over the last year. Just to be transparent I hold a position in four of the five with the exception of MAIN. Due to their BDC price appreciation over the last year, I have not added to any of my holdings besides OBDC. The newcomer still trades at a discount to its NAV.

Many investors who focus on dividend income look to invest into this sector due to their shareholder friendly payouts. And although many investors consider the sector to be risky, I always tell my followers and readers quality over quantity is an important factor, same as investing into any business or sector. There are several other high-quality BDCs that offer investors income, but these five I consider to be fundamentally sound and popular amongst investors.

Read the full article here