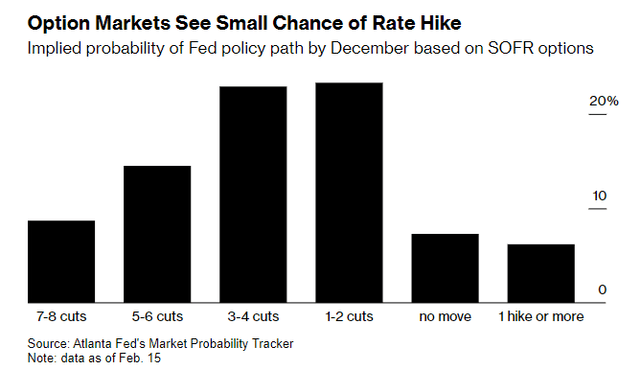

We needed consolidation for the major market averages after the parabolic move that took place during November and December of last year. Stocks were extended to the upside and extremely overbought, while bullish sentiment was equally stretched. I suggested then that the catalyst for selling would be increased uncertainty about the direction of monetary policy leading up to the Fed’s March meeting. The consensus view at that time was that the rate-cut cycle would begin in March. We have had uncertainty in spades since then, as rate-cut expectations continue to be pushed out, while some are now suggesting another rate hike is a possibility.

Finviz

I think that is an absurd assertion, but I am not surprised given the propensity of investors to push to extremes in both directions. Some market pundits, whose forecasts for a recession have fallen short over the past two years, are embracing this extreme forecast, which also comes as no surprise. Former US Treasury Secretary Lawrence Summers is at the top of that list, stating on Friday that “there’s a meaningful chance” the next move in short-term rates is higher. When I hear forecasts like this from influential economists and market observers, I immediately Google their forecasts over the past couple of years to see where they stood and when to understand whether I should place importance in what they say. Their resumes typically give them instant credibility with the consensus.

Bloomberg

In the case of Mr. Summers, he has been forecasting a recession since 2022. He stated repeatedly that unemployment would need to rise as high as 6%, forcing an economic contraction, to bring inflation under control. His persistent negativity has consistently been wrong. Therefore, I have a hard time taking his latest forecast seriously.

Granted, we saw a stronger-than-expected read on the Consumer Price Index and Producer Price Index for January, but neither disrupted the disinflationary trend. In fact, incoming economic data alongside those figures tell us that the rate of economic growth is slowing, as retail sales revealed, which is just the opposite of inflationary. It appears to me that it may be easier for economic and market pundits who got it wrong over the past two years to stick with the doomsday narrative on the basis that they will eventually be right and can claim that were just early. After all, it is a cycle. We will have another recession and bear market at some point, but I seriously doubt it will be in 2024.

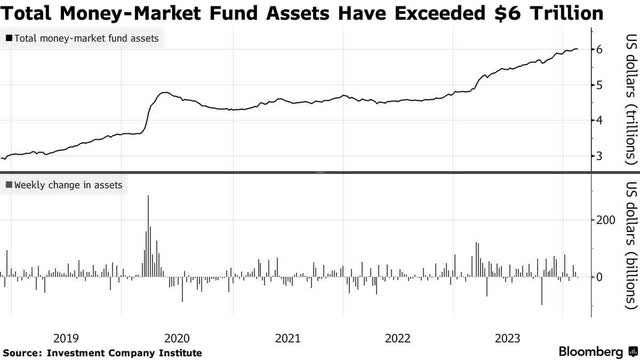

A new piece of data strengthening my resolve on that front comes from the Investment Company Institute. I spoke last year several times about the mountain of money market funds that would minimize any drawdown we saw in the stock market this year and fuel new highs at its start. Given the performance to date, I was certain that had been some reallocation by now. To the contrary, retail investors have added another $128 billion to money market funds since the beginning of the year.

Bloomberg

This is likely due to the expectation that the Fed will keep short-term rates higher for longer, extending the timeframe during which retail investors can earn a risk free rate north of 5%. Many are also likely more concerned that higher-for-longer rates increase recession risk. That’s a realistic concern if the Fed holds off till June or later. It is a near certainty if the Fed were to raise rates again. Yet I am still convinced the first rate cut comes in May at the latest with incoming inflation and economic data assuaging the concerns fueled by the recent CPI and PPI reports.

My critics have claimed that very little of this more than $6 trillion will move back in to markets, but approximately $2.4 trillion of the total is held by retail investors. That is a figure that has doubled over the past two years. I seriously doubt this lot will sit on their hands when money market rates start to fall, and stocks continue to grind to new all-time highs. This is a tremendous amount of dry powder for the second half of the year.

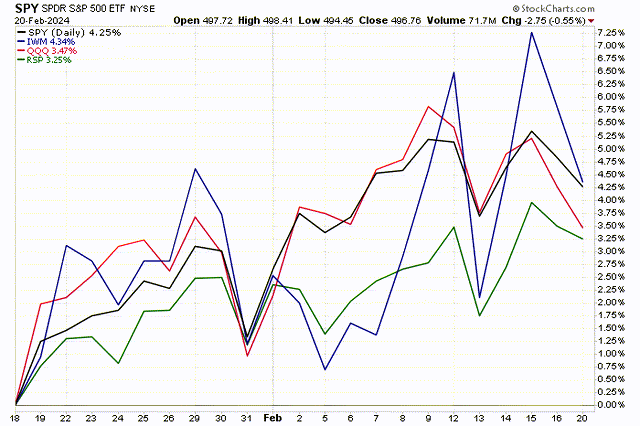

As for the ongoing period of consolidation in the stock market, it continues to develop, as the Magnificent 7 give way to the rest of the market. Over the past month, we have seen small-cap stocks (IWM) outperform the Nasdaq 100 (QQQ). This shows the early stages of rotation are happening. I think investors should expect more of the same as this year progresses. The bull market for the broad market is just beginning.

Stockcharts

Read the full article here