")

Talks of a potential recession should be concerning for Wall Street, but it seems the market is unfazed, judging by the November rally that’s so far carried into December. It’s time to be cautious when the market is being greedy, and one of the best places to park cash in a recession is triple net lease REITs.

That’s because triple net lease REITs come with high margins, since the tenant pays for property maintenance, insurance, and taxes, and one of the names with a long track record of outperformance is Agree Realty (NYSE:ADC).

I last covered ADC here with a ‘Buy’ rating back in July, highlighting its attractive valuation and high exposure to investment grade tenants. Despite the recent uptick in price, ADC is still down by 8.5% since my last piece and down 14% over the past 12 months. In this article, I discuss why now remains a potentially good time to pick up ADC and its preferred issue (NYSE:ADC.PR.A), so let’s get started!

Why ADC?

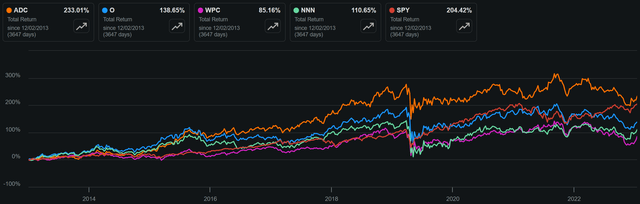

Agree Realty is a self-managed net lease REIT with a diversified portfolio of 2,084 properties that are located in 49 U.S. States. While its much larger peer, Realty Income Corp. (O), captures much of the attention in the net lease space, it’s worth noting that ADC has outperformed O and its net lease peers from a total return standpoint over the past 10 years.

As shown below, ADC has produced a 233% total return over the past decade, surpassing that of Realty Income Corp., W. P. Carey (WPC), NNN REIT (NNN), and the S&P 500 (SPY).

ADC vs. Peers Total Return (Seeking Alpha)

One of the growth advantages for ADC stems from its relatively smaller size compared to its larger peers, which means that it doesn’t take as many deals to move the needle. ADC also has a demonstrated track record of developing properties, making it less reliant on having to source deals from existing properties.

Importantly, ADC hasn’t had to sacrifice growth for quality, as it has one of the highest exposures to investment grade tenants in the net lease space, with 69% of its annual base rent coming from IG tenants. Moreover, 87% of ADC’s ABR comes from nationally-recognized tenants, such as Lowe’s (LOW), McDonald’s (MCD), Starbucks (SBUX), Amazon (AMZN), and TJ Maxx (TJX).

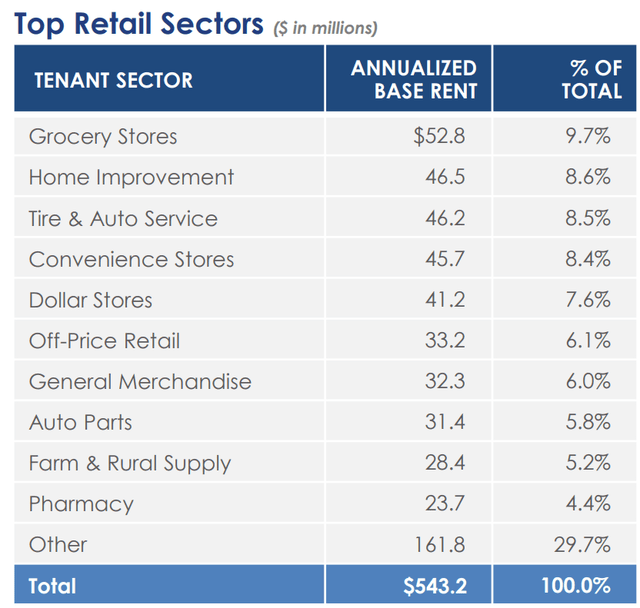

ADC enjoys 99.7% occupancy at present, and as shown below, the majority of ADC’s tenants provide necessity based goods and services that are not easily replaceable by e-commerce, with Grocery, Home Improvement, Auto Service, Convenience and Dollar Stores representing the top 5 sectors, comprising 43% of ABR.

ADC Top Tenant Sectors (Investor Presentation)

Meanwhile, ADC has continued to increase its bottom line despite higher interest rates. This is reflected by AFFO per share growing by 2.3% for the first nine months of this year and encouragingly, this includes an acceleration of Core FFO/share growth to 4.2% YoY during the third quarter to $0.96. Importantly for income investors ADC is returning its gains to shareholders, as true to its form, its continued to raise its dividend, by 3.8%. The dividend is also well covered by a 73% AFFO payout ratio.

While the common refrain for the real estate industry is that high interest rates are bad, well-capitalized players like ADC actually stand to benefit due to higher leveraged competitors in the public and private markets being priced out of the market. This is reflected by ADC investing $411 million in 98 high-quality retail net lease properties during the last reported quarter in sectors including farm and rural supply, auto parts, convenience stores, off-price retail, home improvement, and warehouse clubs, at an attractive weighted average cap rate of 6.9%.

Since the start of the year ADC has invested over $1 billion in 265 retail net lease properties, of which 73% of ABR stems from leading investment grade operators. True to its form, ADC also has 14 development projects underway with a cost of $56 million that are expected to be accretive to the bottom line.

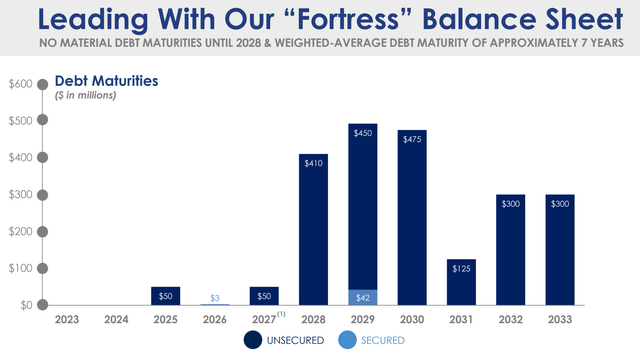

This is supported by ADC’s liquidity of $957 million, and an industry leading balance sheet with a net debt to EBITDA ratio of just 4.5x, sitting below the 5.5x of industry giant, Realty Income Corp. ADC also carries BBB/Baa1 investment grade credit ratings from S&P and Moody’s, and has a strong fixed charge coverage ratio of 5.1x. As shown below, ADC has insignificant debt maturities between now and the end of 2027, thereby shielding it from higher interest rates at present.

ADC Debt Maturities (Investor Presentation)

Risks to ADC include higher interest rates. While ADC’s strong balance sheet helps to blunt the impact from higher rates, its share prices still may take a hit from higher rates, as it has over the past 12+ months. That’s because the investment community is keenly aware of opportunity cost, and 4.9% yielding ADC with 4% dividend growth (this year) may not be appealing to some investors as a “risk-free” Treasury Bond yielding over 5%. As such, ADC could see share price declines due to higher interest rates, and that raises its cost of equity capital that can be used for external growth. Other risks include potential for a recession, but I’m not as concerned about that, considering the strong positioning of ADC’s tenant base and its track record of having navigated previous recessions.

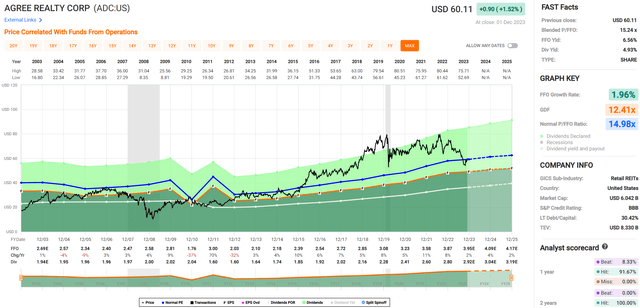

Lastly, I see value in ADC at the current price of $60.11 with a forward P/FFO of 15.2. While this sits higher than the 13.3 of O, 12.3 of WPC, and 12.9 of NNN, I believe this premium is warranted considering its strong balance sheet, mostly investment-grade tenant base, and development prospects. As shown below, ADC currently trades at around its normal P/FFO of 15.0 after being expensive over much of its past several years.

FAST Graphs

Meanwhile, more conservative investors ought to consider ADC’s preferred stock, ADC.PR.A. At its current price of $18.21, this preferred issue currently sits 27% below its par value of $25, and can’t be called until 9/17/2026. Should interest rates remain at elevated levels, this preferred issue potentially won’t be called on that date. This is considering the fact that BBB rated bonds currently yield 5.9%, which sits above the 4.25% yield of this preferred stock at par value. As such, buying ADC.PR.A currently nets the investor a 5.8% yield with the comfort of knowing that it trades below the $25 liquidation preference.

Investor Takeaway

ADC is a strong player in the net lease space, with a proven track record of generating consistent growth with high quality properties. With its focus on investment grade tenants and necessity-based goods and services, ADC has been able to maintain a near-perfect occupancy rate and continue increasing its bottom line despite higher interest rates.

Furthermore, ADC’s well-capitalized balance sheet allows it to take advantage of opportunities in the market, such as investing in high-quality properties at attractive cap rates and developing new projects that are expected to be accretive to the bottom line. With the market seemingly oblivious to risks around a recession, now may be a good time to park cash into ADC and/or its preferred stock for reliable income and long-term value. Maintain ‘Buy’ rating on ADC stock and ADC.PR.A.

Read the full article here