")

Overview

My recommendation for Air France-KLM (OTCPK:AFLYY) is a buy rating (small position), as I find the risk-reward situation attractive enough to warrant a small position in the stock. Management has been executing really well on the cost side, and while revenue uncertainty remains, it does not mean that it is impossible. With management explicitly saying that the first three weeks of October saw no change in the yield environment, there is a good chance for things to remain steady. Note that I previously rated a hold rating for AFLYY until there is more clarity into FY23 performance.

Recent results & updates

Overall, AFLYY reported positive results. While total revenue saw EUR8.66 billion, missing consensus estimates by 4%, the key focus was down the P&L, where fuel costs saw EUR1.91 billion, an 18% decrease vs. last year. This combination led to a 31% growth in underlying EBIT. From a unit economics perspective, AFLYY also demonstrated positive traction. The total number of net work passengers grew by 5%, and Transavia grew by 14%. This, combined with lesser fuel costs, led to an underlying EBIT per ASK (available seat miles) growth of 24%.

While I see the results as positive, which certainly helps in forecasting FY23 performance, I can’t help but continue to feel uncertain due to the lack of a concrete EBIT guide for 2023. We are already 9 months into the year, and management did the 3Q23 earnings call with almost a full month worth of October data, but they are still not able to guide for FY23. I could be reading too much into this, but it certainly gives off a lot of uncertainty vibes that do not work in favor of the stock. Furthermore, upon examining presentation slide number 16, it becomes evident that the booking load factor is exhibiting a decline in comparison to previous years. This phenomenon introduces additional ambiguity regarding the ability of yields to sustain their heightened levels throughout the remainder of the quarter. On the other hand, management’s remarks on yield for the fourth quarter of 2023 have remained consistent, which is positive considering that passenger revenue per revenue passenger kilometer [RPK] has reached its highest level (EUR 10.20) since the fiscal year 2019. During the call, management explicitly stated that there had been no alteration in the yield environment during the initial three weeks of October. In aggregate, it is challenging to assert with certainty the trajectory of the remaining duration of the year. In addition, the management team chose to postpone the discussion of most inquiries regarding plans for 2024 until the forthcoming CMD scheduled for December, which coincides with the conclusion of the current year.

“It’s difficult to tell what the yields will do in the coming period. We have seen, if you look at the bookings, we see — we didn’t see a big impact actually in the last weeks. But we don’t know, of course, what’s all happening in the Middle East.” From: 3Q2023 earnings call

However, it should be noted that the management effectively implemented cost-cutting measures. The unit cost, excluding fuel expenses, aligned with the guidance provided by management. The primary source of cost escalation arises from the salary increments for the CLA, which were initiated in the latter part of the previous year. As a result, the fourth quarter of 2023 is expected to experience a relatively muted effect (relative to 1-3Q23), followed by a more accurate year-on-year comparison commencing from the fiscal year 2024 onwards. Management has also decided to maintain the full-year outlook without any changes, suggesting a reduced expense growth rate for the fourth quarter of 2023.=.

Valuation and risk

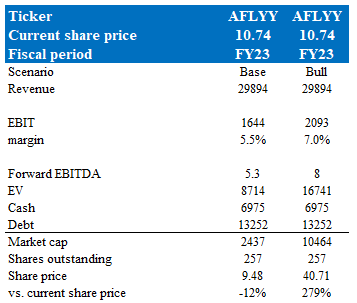

Author’s valuation model

Following my previous model, where my focus was whether AFLLY could achieve 7% EBIT margins in FY23, My outlook remains murky, but certainly more positive than in 2Q23, given the execution on managing costs in 3Q23. I have laid out scenarios in my model above, both using consensus revenue estimates as a base and different EBIT margin assumptions to show what the market is pricing today.

- In my base case, I expected a deterioration in EBIT margin from LTM figures to 5.5% and the stock to trade at 5.3x EBITDA (which is where it is trading today). My price target implies a modest decline from the current share price.

- In my bull case, the stock has tremendous upside. As I mentioned previously, if AF does hit 7%, valuation should rerate positively almost immediately as consensus will pull forward their modeled numbers, resulting in massive earnings revisions. Note that consensus is not projecting an EBIT margin to hit 7% at least until mid-FY25. As such, any earnings revision will be massive.

Viewed from this lens, the risk/reward situation is quite attractive, and hence, I recommend buying a small position in AFLYY to take advantage of this situation.

Some risks to take note of are that execution on further cost restructuring might not be as successful as I might have hoped, leading to lower margins. AFLYY’s market position on APAC routes might become uncompetitive due to the closure of Russian Airspace to European carriers compared to APAC carriers.

Summary

I upgraded my rating to buy for AFLYY as the risk-reward scenario appears favorable. While the company’s recent results showed some discrepancies in revenue but significant improvements in underlying EBIT, management’s cost-cutting measures have been effective. From a valuation perspective, my outlook remains positive but somewhat uncertain, with various scenarios outlined in my model. The risk-reward situation looks attractive, especially in a bull case where reaching a 7% EBIT margin could lead to substantial earnings revisions and positive valuation rerating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here