")

Air Products and Chemicals (NYSE:APD) just came out with Q4 earnings. EPS reached $3.15, beating the Wall Street consensus estimate of $3.12 and compared to earnings of $2.89 per share achieved a year ago. Over the last four quarters, APD has surpassed consensus earnings per share estimates three times. On the other hand, Q4 top-line sales missed estimates by $160 million due to unfavorable FX impacts and lower fees for energy pass-through. The share of APD fell by 10% when we were writing this analysis, and we believe this is not justified. Our buy rating was supported by 1) a long story of DPS increase, 2) an impressive project backlog to drive the energy transition and hydrogen opportunity, and 3) a solid balance sheet allowing the company to expand CAPEX without limiting shareholders’ remuneration. On a negative note, last time, we also emphasized two ongoing debates: 1) APD’s succession plan and 2) business performance relative to peers. Also, in the Q3 results release, we were surprised about the adverse stock price reaction. In detail, as a reminder, at the Wall Street closing bell, APD shares declined by 5.85%.

In our last release, we forecasted:

The new projects should add $1.4 per share EPS growth over the next year, and we anticipated a 12% EPS growth in Fiscal Year 2024.

Looking back, our financial estimates were accurate, and ADP achieved an EPS growth higher than its previously Q4-guided EPS, which ranged between 7% and 10%.

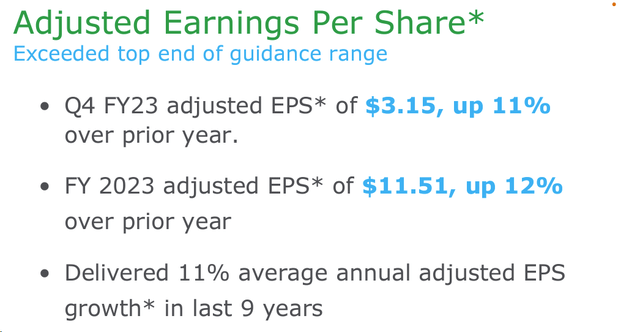

Air Products and Chemicals Q4 and FY EPS growth

Source: Air Products and Chemicals Q4 results presentation

Q4 Results and Future Guidance

Looking at the financials, Q4 top-line sales reached $3.2 billion and decreased 11% from the prior year. This was due to 2% higher pricing and 1% FX gain but was offset by a 14% decline in lower energy cost pass-through. APD adjusted EBITDA reached $1.3 billion and increased by 10% thanks to higher equity affiliates’ income. The company’s EBITDA margin was at 39.5%, signing a plus 740 basis points over the prior year but a minus 30 basis points on a quarterly basis. On an adjusted EPS basis, APD reached $3.15 with a plus 11%. Regarding the Fiscal Year 2023, despite a challenging environment, the company achieved solid results. The adjusted EPS reached $11.51 and was up 12% with an EBITDA at $4.7 billion, again up by 11% percent and a margin of 37.3%.

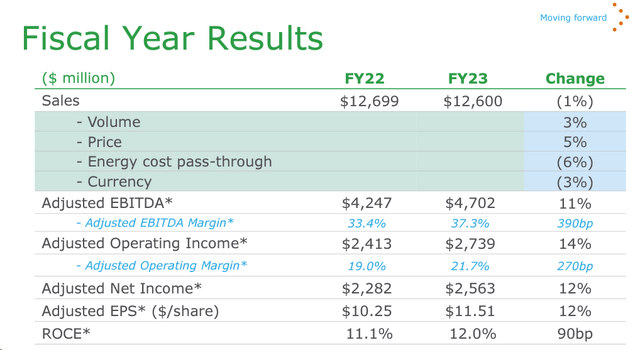

Air Products and Chemicals 2023 Financials in a Snap

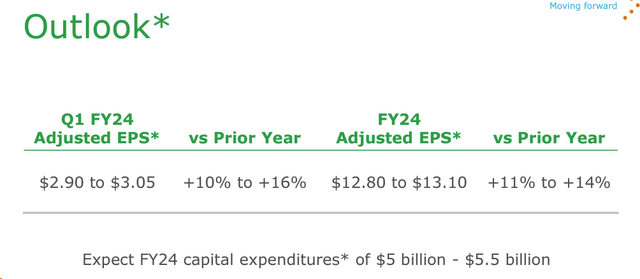

During the Q4 and FY results presentation, the company released its 2024 full-year EPS guidance. APD disclosed 2024 EPS between $12.80 and $13.10, with a 13% at the midpoint level compared to 2023. In addition, Q1 2024 EPS is set to accelerate further with an outlook between $2.90 and $3.05. The company’s CAPEX was left unchanged despite the higher commitment to the Louisiana project.

Air Products and Chemicals 2024 Guidance

Current Upside

Post Q4 results, here at the Lab, we believe the company is trading at an attractive valuation, given APD EPS acceleration. In detail, the company trades at a Fiscal Year 2024 EV/EBITDA of 12.5x, which is in the low range of its historical average. Indeed, in the last seven years, the APD EV/EBITDA range was between 12x and 16x.

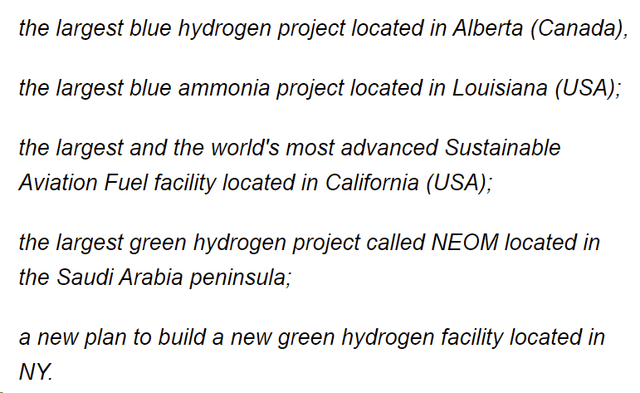

The company has a large project backlog of $19.4 billion, including approximately $15 billion worth of green energy/hydrogen transition projects. Out of the mega-cap project, APD’s pipeline consists of the following:

Mare Past Analysis

In detail, in 2024, we expect Jazan Phase II, Jutal, and UNG/Uzbekistan to come online. Alberta net-zero hydrogen in Canada and the World Energy Aviation Fuels is due in 2025, while NEOM and Louisiana blue H2 and NY green H2 will support APD EPS growth beyond the Fiscal Year 2026. In our estimates, we might anticipate an EPS acceleration of 20% in 2025, given the company’s backlog and production expansions within the existing facility.

Conclusion and Valuation

In the Q&A, the CEO reported positive news and confirmed APD’s long-earnings EPS growth trajectory. Here at the Lab, given the FCF estimates, we arrived at an end debt of $8 billion, and including our $1.4 EPS growth due to the project coming online, we increased our EPS to $13.2 for 2024. Applying an unchanged P/E multiple set at 25x, our target price remains unchanged at $330 per share. We forecast a slightly higher EPS growth due to confidence that APD can bring several new projects on stream and as already happened in 2023, this might represent approximately 2/3rds of the positive growth drivers in the upcoming fiscal year (Fig below).

APD Business Model

The company also has CAPEX optionality, a pass-through contract to mitigate inflation impact, and a first-mover advantages in hydrogen that cannot go unnoticed. On the downside, aside from the risk already discussed, APD’s mega project backlog can be delayed and project costs might vary given the persistent inflation. This could cause choppy EPS growth and expected IRR. APD might increase its financial debt to fund future growth opportunities, and interest expenses might be higher than anticipated.

Read the full article here