")

April 22nd was a rather interesting day for shareholders of Albertsons Companies (NYSE:ACI). The grocery store, which is in the process of being acquired by The Kroger Co. (KR), announced financial results covering the final quarter of the 2023 fiscal year. Management reported revenue that fell short of expectations. On the other hand, earnings per share, while worse than it was a year earlier, came in higher than expected. Furthermore, the company announced, in conjunction with Kroger, that an agreement has been made with C&S Wholesale Grocers whereby C&S will end up acquiring some additional stores as part of its deal to purchase hundreds of locations in order to appease regulators.

At this time, the management teams of both Albertsons and Kroger appear to be confident that the merger between the companies will go through. It’s also worth noting that, since I last reiterated my ‘strong buy’ rating on the company earlier this year, shares are down 5.6% compared to the 3.1% rise seen by the S&P 500 over the same window of time. So it does look as though the market is even more pessimistic than it was previously. With this move lower, the implied upside between the current price of the stock and the acquisition price is a hefty 34.7%. Some of this weakness is almost certainly due to the lawsuit filed last month by the FTC, not to mention other parties, aimed at blocking the deal.

All things considered, I view the matter differently than most investors. I would prefer for the company to ultimately be acquired by Kroger and I do believe that this recent announcement of additional store sales will help increase that probability (though not by enough to make me think it’s likely to go through). But given how cheap the stock currently is, I think that it’s undervalued even at the buyout price. Because of this and in spite of the recent downside that shares have experienced, I would argue that the stock still makes for a very good ‘strong buy’ candidate at this time.

A look at recent developments

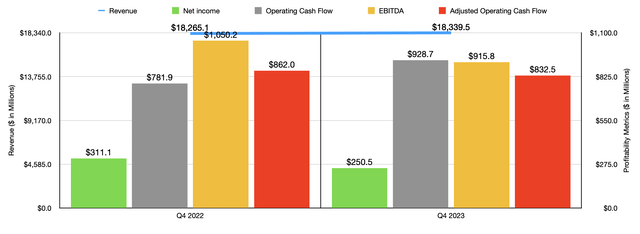

To start things off, we should probably touch on how Albertsons performed for the latest quarter for which data is available. This is the final quarter of the 2023 fiscal year that management just reported on April 22nd. All things considered, the picture was relatively decent. Revenue, for instance, came in at $18.34 billion. That’s 0.4% higher than the $18.27 billion generated one year earlier. Although it is nice to see sales increase, revenue did fall short of expectations to the tune of $140 million. According to management, the increase was driven by a 1% rise in identical sales. This was offset to some extent by lower fuel sales and a reduction in wholesale revenue. There were some really impressive spots. For instance, management described pharmacy sales as strong. And digital sales jumped 24% year over year. One thing that proved to be a slight drag on the business was a reduction in store count. At the end of the quarter, the firm had 2,269 locations in operation. This was down from the 2,271 that it had at the end of the final quarter of 2022.

Author – SEC EDGAR Data

Even though Albertsons fell short of expectations when it came to sales, the company exceeded forecasts when it came to profits. Earnings per share came in at $0.43. While that is down from the $0.54 per share reported one year ago, it actually was $0.02 per share higher than what analysts anticipated. And the adjusted earnings per share of $0.54 was also $0.02 per share greater than what was forecasted. This translated to net profits falling from $311.1 million down to $250.5 million. But that’s not terribly surprising. For the year as a whole, the company had been suffering from a profitability perspective. Other profitability metrics were mixed. For instance, operating cash flow jumped from $781.9 million to $928.7 million. But if we adjust for changes in working capital, we get a decline from $862 million to $832.5 million. Lastly, EBITDA for the company fell from $1.05 billion to $915.8 million.

Author – SEC EDGAR Data

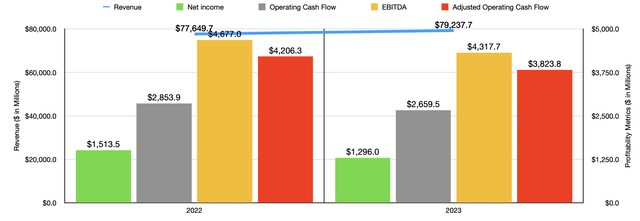

In the chart above, you can see financial performance for 2023 relative to 2022 as a whole. Just like what we saw in the final quarter of the year, revenue increased from one year to the next. However, profits and cash flows were down without exception. This was driven by three primary factors. First, the company’s gross profit margin contracted from 28% of sales to 27.8%. While that may not seem like a huge disparity, when applied to the revenue the company generated in 2023, it amounted to $158.5 million in pre-tax profits that were missed out on. That decline was associated with higher shrinkage costs, operating issues with its pharmacies, and a rise in picking and delivery expenses as the company focused more on digital sales. On the pharmacy side, it was because of higher pharmacy revenue and a lower margin rate on COVID-19 vaccines. The picture would have been worse had it not been for certain productivity initiatives that the company implemented during the year that allowed it to increase prices to some extent. In addition to this, the company saw a swing from a $147.5 million gain on property sales and impairments to a loss of $43.9 million this year. And finally, interest expense jumped from $404.6 million to $492.1 million, which was largely because of a higher debt balance and a slight increase in the weighted average cost of debt from 5.3% to 5.6%. As the chart shows, other profitability metrics followed net income down year over year.

Author – SEC EDGAR Data Author – SEC EDGAR Data

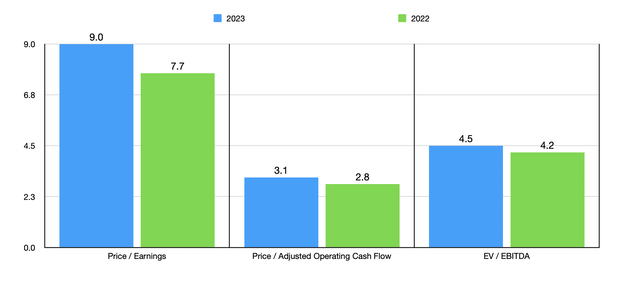

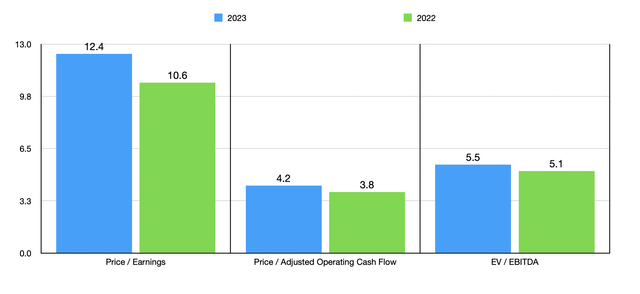

At this point, I am still leaning in the direction of saying that the transaction will fall through. However, even if it does, shares will look very attractive. Using the historical results from 2022 and 2023, I valued the company as shown in the chart above. In the second chart above, I then valued the firm again based on the price that Kroger is paying for it. I then compared the firm’s implied buyout price to five similar enterprises in the table below. On a price to earnings basis, even with profitability shrinking year over year, Albertsons ended up being the cheapest of the five firms. And when it comes to the other two profitability metrics, only one of the five companies was cheaper than it.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Albertsons Companies | 12.4 | 4.2 | 5.5 |

| The Kroger Co. | 19.2 | 6.1 | 6.8 |

| Metro Inc. (OTCPK:MTRAF) | 15.7 | 10.4 | 9.3 |

| Casey’s General Stores (CASY) | 24.9 | 13.8 | 12.9 |

| J Sainsbury (OTCQX:JSAIY) | 74.6 | 3.3 | 3.0 |

| Sprouts Farmers Market (SFM) | 26.1 | 14.5 | 10.5 |

On the regulatory side, a lot has happened since I last wrote about the firm. Last month, news broke that the FTC, as well as eight different states and Washington DC, all decided to file a lawsuit in order to block the merger between these companies because of concerns that such a combination will prove anticompetitive. Almost something changes moving forward, it looks as though that trial is expected to start on August 26th of this year. And in all likelihood, it’s going to last two to three weeks. The concern centers around the prospect of lower wages for workers and higher prices for consumers. It is worth noting, however, that Kroger has pushed back on this. They claimed that, since 2018, they have invested $2.4 billion to raise wages and benefits. And as part of this deal, they claimed that they are committed to investing $1 billion to raise them further. On top of this, Kroger made the argument that they are investing $500 million to lower prices, starting day one of the acquisition being completed. And this is on top of another $1.3 billion that would be allocated toward improving the Albertsons locations that they purchase.

Also, to increase the probability that the deal will ultimately be approved, the company announced on April 22nd that it has revised its deal with C&S. Previously, C&S agreed to acquire 413 stores in certain areas. But that number has now been increased by 166 to 579. This would be done at a $2.9 billion purchase price, with most of those stores being between Washington, Colorado, Arizona, and California. As part of the revised agreement, C&S will license the Albertsons name in California and Wyoming, as well as the Safeway name in Arizona and Colorado. For the stores that still remain in those states that will belong to Kroger, Kroger will change those names, likely to Kroger while keeping the Albertsons and Safeway names in states that these transactions are not occurring in. There are some other developments as well, such as office infrastructure that will be provided to C&S by Kroger, and the fact that any fuel centers and pharmacies that will be divested will remain in those stores that are sold off and will continue to operate. But these are fairly minor aspects of the overall deal.

Takeaway

As things stand, I must say that I am not terribly optimistic of this transaction going through. If it does, there will be significant short term upside for shareholders. If it doesn’t, I still believe that shares of Albertsons are incredibly cheap. Given these factors, I am very comfortable with the ‘strong buy’ rating I previously assigned Albertsons.

Read the full article here