")

Alcoa Corporation (NYSE:AA) faces a challenging, yet transformative FY24 as the firm positions itself as the leading, global vertically integrated aluminum supplier. As the firm is realizing headwinds in restarting their Alumar facility, the sales process for the unviable San Ciprian complex, and shifting macroeconomic headwinds, I believe AA shares to be overvalued at 17.69x EV/aEBITDA. I provide AA shares with a SELL recommendation with a price target of $31.77/share at 7x eFY25 EV/aEBITDA.

Macroeconomics

The very next day after Alcoa announced their Q1’24 earnings results, the Biden administration threw the company a nudge that may pull forward their journey towards returning to profitability. As the US appears to be deepening its trade war with China, the administration pitched increasing trade tariffs on Chinese steel and aluminum 3x from 7.5% to 25%. According to the Wall Street Journal report, these tariffs would be in addition to a separate 25% tariff on steel and a 10% duty on aluminum imposed under the Trump administration.

Alcoa is currently in the process of restructuring operations and is positioning the firm to capture growth in the expanding market for aluminum. The World Economic Forum forecasts aluminum demand to rise 40% by 2030. Much of this growth will be driven by renewable energy, electric vehicle adoption, and electrification of the grid, amongst other things. Given how energy-intensive the aluminum refining and smelting process is, management is actively taking steps towards decarbonization, whether it is through the use of renewable power sources for their smelters or utilizing scrap and recycled aluminum. In fact, management mentioned that they will not bring on a new smelter if it is not powered by renewable energy. Management also mentioned in their Q1’24 earnings call that renewable green power is getting harder to define globally as supply becomes more limited. They mentioned that data centers leveraging green energy may make sourcing renewable energy scarcer, which in turn may suppress supply of aluminum as a result, assuming the firm opts to not utilize another power source. This may also be management’s way of limiting production as the market price for aluminum turns around. According to data provided by CME Group, aluminum futures for April are priced at $2,601, and are expected to appreciate to $2,670 by April 2025. Aluminum spot is more appealing at $2,643, according to pricing information provided by TradingView.

TradingView

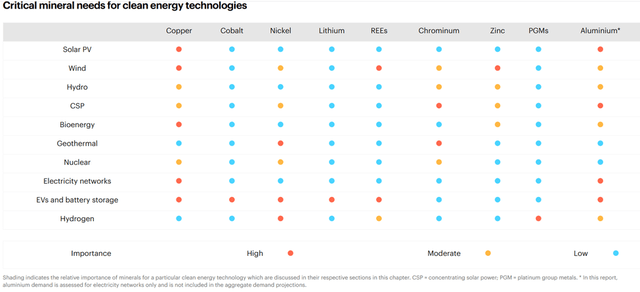

In terms of aluminum demand, I expect some headwinds in the renewable energy space as the industry faces pricing and financing headwinds. According to Deloitte, renewable energy projects are facing dual paths. In 2023, utility-scale solar capacity in the US grew to 9GW, up 36% y/y, while small-scale solar generation grew by 20%. During the same period, wind capacity lagged significantly with only 2.8GW of capacity being brought online, a 57% decline from the previous year. As for 2024, the EIA forecasts renewable capacity deployment to grow by just 17% to 42GW. This comes in at the lower end of the National Renewable Energy Laboratory’s forecast as a result of the IRA and Infrastructure Bill’s funding allocation for renewables deployment.

Looking at the case for Alcoa, the slowdown in wind turbine deployment shouldn’t affect the firm to a great extent as aluminum makes up only 0-2% of the turbine. Solar, on the other hand, has a much larger requirement for aluminum, making up roughly 85% of the panels. Accordingly, solar PVs could take up nearly half of the world’s demand for aluminum by 2050.

IEA

Looking to electric vehicles, aluminum will be necessary to provide for a lighter frame in order to accommodate the added weight from the battery components. According to a 2023 survey of the auto OEMs and Tier 1 suppliers, demand for aluminum is expected to increase by nearly 100 net pounds per light vehicle from 2020 to 2030. Growth areas for aluminum in the vehicles include body-in-white, battery housing, motors and drives, doors, and rockers. For reference, the Ford Motor Company (F) F150 Lightning is expected to average over 644lbs of aluminum content. Given aluminum’s lighter profile when compared to steel, this can provide a significant advantage for improving vehicle mileage as battery technology pushes the limitations of efficiency. Though the usage of aluminum in EVs is necessary, the automotive industry has recently downshifted to a slower pace of EV manufacturing as consumers favor hybrids and ICE vehicles over EVs.

Case for Alcoa

Alcoa recently announced their intent to acquire the entirety of their JV for Alumina Limited to become a more vertically integrated, upstream aluminum company. I believe that this will provide Alcoa more control over production of alumina and aluminum as the global leader and should allow the firm to further curtail production to bolster aluminum prices. Alumina Limited will be brought in at $2.2b in an all-equity deal at a conversion rate of 0.02854 AA shares for each Alumina Limited (OTCQX:AWCMF) share. Management anticipates the deal to receive government and regulatory approvals in Q2/Q3’24 with shareholder approvals in Q3’24. This deal will further expand Alcoa’s control over the bauxite and alumina market and may allow the firm to regain a profitable position. This will also give Alcoa greater access to low carbon and recycled content as the firm develops carbon-reducing technologies for the aluminum smelting process.

In Q1’24, management made some significant announcements that may impact operations going forward. Though much of the insights into the organization had a relatively negative spin, I believe that management is taking the right steps to turn the firm around. For starters, Alcoa is in the process of sourcing potential suitors for their San Ciprian complex as it has been found to be nonviable. Management mentioned that the facility is a major cash burn and expects cash to run out in 2H24 for the facility without government support or easing energy prices. Many of the analysts’ questions centered around the facility included shutdown costs and the rationale behind competitors buying the facility if it is unviable. Given the operational challenges faced within the facility, I anticipate Alcoa to resort to an impairment or a significantly discounted sale as a successful sale depends on the very same challenges Alcoa faces, government support and union flexibility.

The firm is also facing challenges with their Alumar restart as the facility had been curtailed for eight years. This has resulted in a decay of the condition of the equipment within the facility, making refurbishments that much more challenging. In addition to this, Alcoa curtailed production at their Kwinana Alumina Refinery to 80% of the 2.2mm metric tons of capacity. This curtailment is expected to improve operations by $70mm in Q3’24.

Looking to the financials, management anticipates a $20mm unfavorable impact to aEBITDA resulting from higher seasonal maintenance and other mining costs for their Australia operations. Management also expects unfavorable costs resulting from higher energy that will offset the favorable alumina pricing. As a result, I anticipate some margin compression paired with slightly increased production across their segments throughout the duration of eFY24. Given the macroeconomic backdrop, I am modeling slightly lower revenue when compared to the consensus estimates as provided by Seeking Alpha.

Corporate Reports

Valuation & Shareholder Value

Corporate Reports

AA shares currently trade at 17.69x EV/aEBITDA. I believe this is a very rich premium on the company’s stock as it works through the operational challenges faced in FY24. I believe that the market is optimistic about the firm’s ability to sell the San Ciprian complex and I believe that the firm may realize an impairment charge if the facility remains unviable. With the expectations of the operational challenges leading to tighter margins for FY24 and FY25, I anticipate shares to better reflect the company’s hurdles. I provide AA shares with a SELL recommendation with a price target of $31.77/share at 7x eFY25 aEBITDA.

Corporate Reports

Read the full article here