Asset managers are in a much better spot today compared to 18 months ago. Domestic stock prices are of course higher, but with interest rates steadying out a bit and foreign equity returns looking solid, diversified allocations have produced impressive performances. It comes as private-market investing has also been in demand, particularly in the credit space. Not surprisingly, we have seen strong earnings results from several banks and asset management firms.

I reiterate a buy rating on AllianceBernstein (AB). The stock continues to look cheap, while its high dividend yield is icing on the cake for income-focused investors. AB’s momentum has also improved, which I will highlight at the end.

ETF Performance Heat Map: Solid Stock & Bond Returns In the Last Month

Finviz

According to Bank of America Global Research, AllianceBernstein is a financial services firm with a large asset management business in addition to a captive private wealth platform and a sellside research business. AB is controlled by Equitable Holdings and is organized as a publicly traded partnership.

Back in April, AB reported an in-line Q1 earnings report. Q1 non-GAAP EPS verified at $0.73 while revenue of $1.1 billion, up nearly 8% from year-ago levels, was a sizable $200 million beat. The firm issued a cash distribution of $0.73, a slight decrease from the previous dividend of $0.77. But big picture, it was a solid quarterly report with improved net flows and better operating margins. Its fixed income and alternative investments segments performed well while traditional stock and bond returns in Q1 was an obvious tailwind, though its equities segment was actually to the soft side.

Then, more recently, the April AUM update fell 2.9%, but that was largely the result of a temporary pullback in equities and fixed income. The firm reported positive flows once again to begin the second quarter.

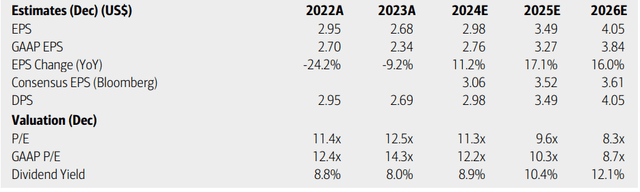

On valuation, analysts at BofA see earnings rising at an impressive pace over the years ahead. FY 2024 EPS is expected to jump 11% while out-year operating per-unit profits are forecast to jump another 17%. The Seeking Alpha consensus numbers are about in-line with what BofA projects, with 2026 non-GAAP EPS potentially rising to the $3.50 to $4 range. Revenue growth is seen accelerating over the next two years as well.

Currently, yielding north of 8%, annual dividends are forecast to increase substantially over the quarters ahead. Finally, with a low earnings multiple, AB remains a compelling fundamental value.

AllianceBernstein: Earnings, Dividend, Valuation Outlooks

BofA Global Research

If we assume next-12-month non-GAAP EPS of $3.25 and apply the stock’s 5-year average operating P/E of 12.25, then the stock should trade just shy of $40, that is up from my previous valuation in the mid-$30s back in October last year. Also consider AB’s very favorable 0.77 forward non-GAAP PEG ratio, given that the firm’s profit growth is so healthy.

AB: A Very Attractive PEG Ratio, > 8% Yield

Seeking Alpha

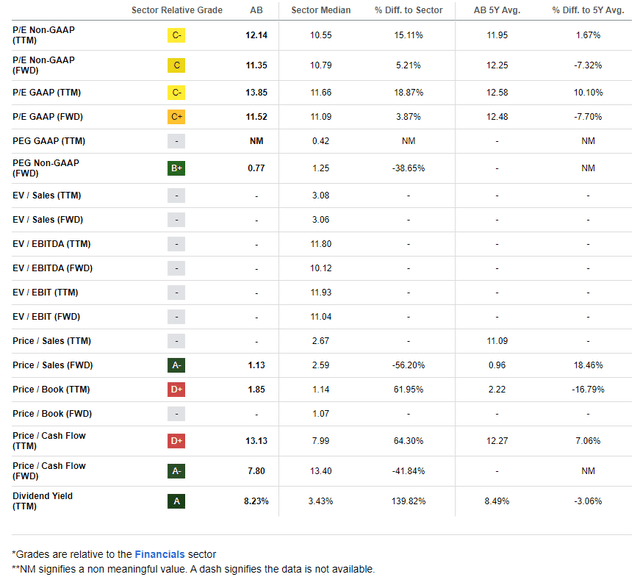

Compared to its peers, AB sports a stellar A valuation rating, while its growth trajectory is almost as strong. With healthy profitability trends, the asset management firm has endured more sellside EPS downgrades lately, compared with just a pair of upgrades. Unit-price momentum has been problematic, but I am encouraged by a few indicators on the chart that I will detail later in the article.

Competitor Analysis

Seeking Alpha

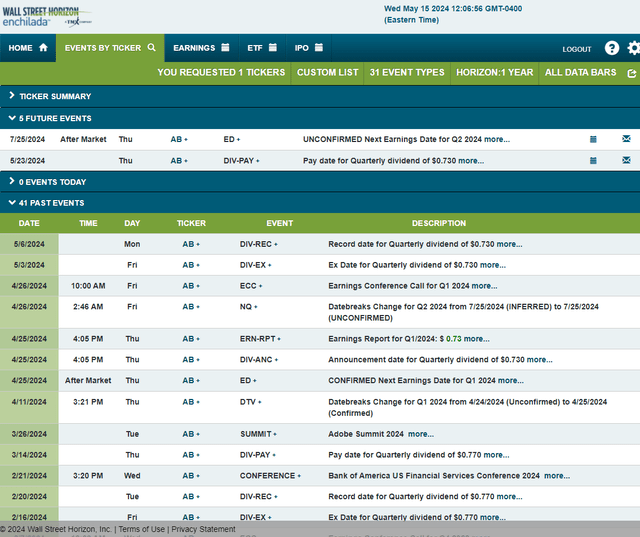

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2024 earnings date of Thursday, July 25 after market close. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

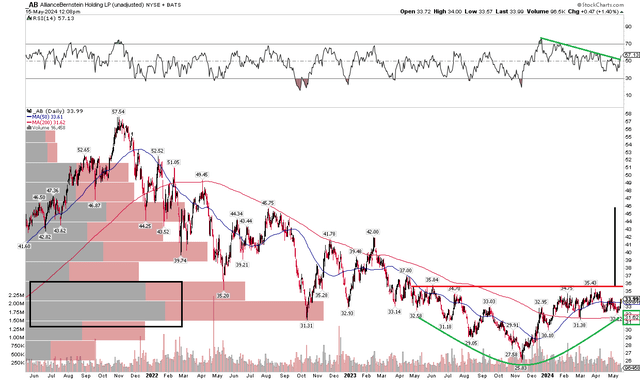

The Technical Take

With a low valuation and favorable market conditions, AB’s technical chart has improved. Notice in the graph below that units dipped to a multi-year low under $26 toward the end of 2023, but then rebounded sharply as the stock market improved and interest rates stabilized. What’s more, AB rose above its long-term 200-day moving average and then held that trend indicator line on a few occasions this year. I see resistance just above the $35 mark. If the stock rallies through that, then a bullish upside measured move price objective to about $46 would be in play based on the height of the consolidation range from mid-2023 through today.

Also take a look at the RSI momentum oscillator at the top of the chart – a downtrend line appears to be giving way to improved momentum. That could be a harbinger of improved price action in the weeks and months ahead. Still, there remains a high amount of volume by price up to the mid-$30s, but a bullish rounded bottom feature is a definite improvement from the late 2021 through late 2023 downtrend.

Overall, the trend appears better today, and a rally through $36 would be a positive development.

AB: Bullish Rounded Bottom Pattern, $36 Resistance

Stockcharts.com

The Bottom Line

I reiterate a buy rating on AB. I see the asset management firm as significantly undervalued if we use out-year EPS estimates. Furthermore, the company’s dividend yield remains high even after the slight decline in the Q1 distribution. Finally, AB’s technical view has improved.

Read the full article here